The value and momentum factors have earned high praise in recent years as complementary sources of risk premia for designing and managing equity portfolios. AQR’s widely cited paper “Value and Momentum Everywhere” a few years back helped popularize the idea, pointing to applications in equities and beyond. There’s no shortage of support from the wider world of investment management. Earlier this week, for instance, Jack Vogel at Alpha Architect outlined “Why Investors Should Combine Value and Momentum.” Not surprisingly, there are several investment funds focused on the strategy, including the recently launched Cambria Value and Momentum ETF (VAMO).

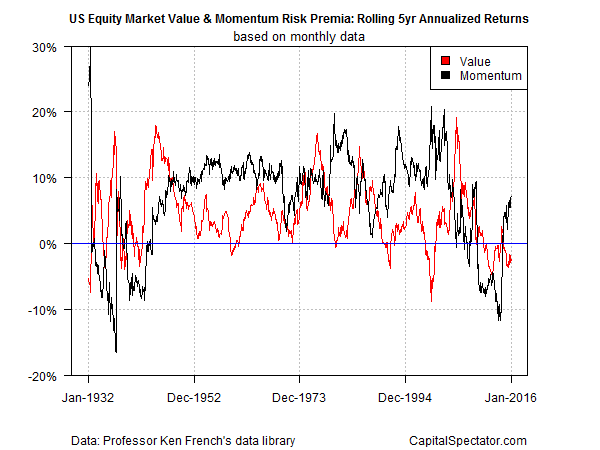

The rationale for a value-momentum mix can be summarized by reviewing the historical results. Consider rolling five-year annualized returns (a time window used in AQR’s paper), which captures a fair amount of mean reversion. The chart below hints at the possibilities from a portfolio-design perspective. Using the risk premia numbers via Professor Ken French’s data library suggests that value and momentum do in fact exhibit a fair amount zigging when the other factor’s zagging.

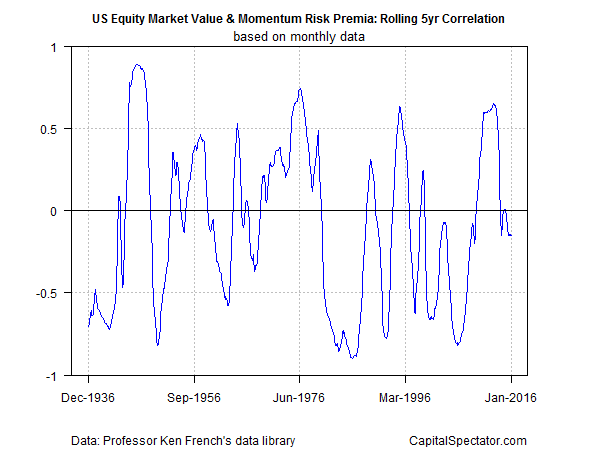

The correlation for the two sets of rolling 5-year returns since the early 1930s is moderately negative—roughly -0.24 (based on monthly returns). That tells us that no one will confuse one risk premium for the other. But how does correlation stack up over shorter periods? From a practical perspective, the results over, say, five years offer more insight into the potential for tapping into the value-momentum dynamic. As the next chart shows, the relationship is far from static. Indeed, the rolling five-year correlations ebb and flow through time by more than a trivial degree. The implication: a dynamic system for managing risk with these factors may be superior to buying and holding.

Sometimes, and perhaps for several years at a stretch, these two risk factors generate similar returns. During those times you’ll probably read stories proclaiming the “Death of Diversification For Value and Momentum Strategies.” But if history’s a guide, the tight correlation will only be temporary.

There’s nothing magical about rolling five-year windows, of course. A serious research project would review multiple rolling periods by running the numbers through a battery of risk analytics. But the preliminary if inconclusive profile above implies that looking at the equity market (and other asset classes) through a value-momentum prism has intriguing possibilities.

One question that comes to mind: How does a value-momentum strategy fare as a buy-and-hold proposition (with naïve year-end rebalancing) vs. a tactical asset allocation application? How much improvement, if any, should we expect with a dynamic system? In an upcoming post, I’ll explore this question with a back-test and reviewing the results by adjusting for risk.

Several researchers have already run similar tests and produced encouraging results. Let’s see if we can replicate the data. The literature suggests that’s likely. But the devil’s in the details. There are several ways to define “value” and “momentum” and there’s a rainbow of possibilities for implementing tactical strategies. Therein lies the potential for success… or failure.

But it’s always best to start with a simple model. If there’s truly opportunity for enhancing a buy-and-hold version of a value-momentum strategy, the evidence should be clear in a basic tactical model.

Pingback: Value and Momentum Factors

Pingback: 03/24/16 – Thursday’s Interest-ing Reads | Compound Interest-ing!

In Dr. Vogel’s post he concludes that “a static value and momentum portfolio has known diversification benefits” but the stats that he includes in his post are not encouraging. The ‘Momentum’ only portfolio has far better stats than the ‘Value’ only portfolio with the exception of ‘Best Month Return’ (98%; yikes, don’t want to miss that month!!) On a risk adjusted basis adding ‘Value’ doesn’t improve on the ‘Momentum’ portfolio. In fact the 50/50 portfolio is still poorer than the stand alone ‘Momentum’ portfolio. One would assume when one asset ‘zigs’ while the other ‘zags’ the net effect of owning both would be better risk adjusted returns.

I had the same results as Doug. Using relative strength momentum with indices gives better results and is less expensive than combining stock value and momentum. See Antonacci’s: http://goo.gl/z0RAS6

Pingback: US Equity Value and Momentum Risk Premia - TradingGods.net

Pingback: Quantocracy's Daily Wrap for 03/24/2016 | Quantocracy