The recent rise in the 10-year US Treasury yield has stalled. It’s unclear if this is a pause before the upside trend resumes vs. the early stages of new leg down. The sharp rise in inflation this year and the potential for an economic slowdown in the new year are conflicting factors that are muddying the outlook. While this scenario continues, our baseline forecast anticipates that a trading range for the 10-year rate will prevail in the near term, in part based on today’s update of The Capital Spectator’s ensemble model for estimating the benchmark yield’s “fair value.”

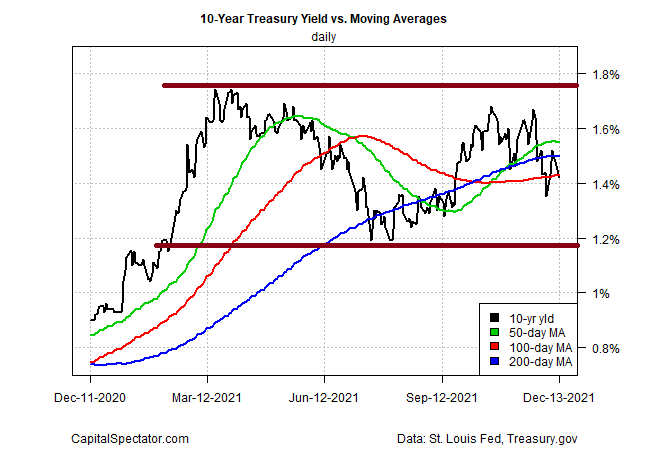

The 10-year yield fell to 1.42% yesterday (Dec. 13), the second-lowest level since late-September. Nonetheless, the yield continues to print at a middling level relative to this year’s range.

The latest slide suggests the market is pricing in higher odds that the upcoming changes in the Federal Reserve’s monetary policy will slow the economy. In line with that profile, the 10-year/2-year yield spread has declined recently, slipping to 76 basis points, close to the lowest level of the year. A narrower yield curve is widely considered a market forecast of softer economic growth. Note however, that the 10-year/3-month spread is relatively stable, leaving room for debate about the significance of the sharper fall in the 10-year/2-year spread. As long as the yield curve is positive (long rates above short rates), the implication is that the market’s assuming some level of growth will endure. When/if the curve inverts (long rates below short rates), that would be a forecast for an economic recession — a forecast that’s nowhere on the immediate horizon at the moment.

A key factor for assessing where rates are headed is the outcome of tomorrow’s Federal Reserve policy announcement and press conference (Wed., Dec. 15). Although forecasters see low odds that the Fed will lift the current 0%-to-0.25% Fed funds target rate (based on Fed funds futures) tomorrow, the central bank is expected to announce a faster round of tapering its bond purchases, which would be seen as laying the groundwork for an earlier-than-expected rate hike in the new year.

“With high inflation readings heading into the new year, we now expect the Federal Reserve to speed up tapering to reach ‘zero’ by March 2022, leaving the year open for at least one rate hike, perhaps even sooner than our forecast of their first hike in September,” says Beth Ann Bovino, US chief economist at S&P Global Ratings.

Meanwhile, the 10-year Treasury yield continued to trade below CapitalSpectator.com’s fair-value estimate. The gap suggests that there’s a floor and perhaps a modest upside bias for the rate’s near-term outlook.

Last month marks the sixth-straight month that the 10-year yield traded below our fair value estimate. The spread for November: -54 basis points, modestly deeper than the -44 basis points spread in October, as shown in the chart below.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Pingback: 10-Year Treasury Yield Has Stalled - TradingGods.net