The Federal Reserve is widely expected to lift its target interest rate by 75 basis points tomorrow (Wed., Sep. 21). The question is whether the bond market has priced in the change? That’s a tough call until there’s deeper clarity on where inflation is headed.

There are hints that inflation has peaked, but the evidence is still thin. Even thinner is support for expecting high inflation to ease quickly and substantially in the immediate future.

Meanwhile, the benchmark 10-year US Treasury yield edged higher yesterday (Sep. 19), reaching 3.49% — matching the previous high set in June. For the moment, one can argue the market is on the fence, weighing two competing outlooks. If the crowd senses that the Fed’s policy tightening are still not sufficient to tame inflation, we’ll see the 10-year yield push decisively higher. Investors are also asking: Will tomorrow’s expected rate hike fully convince the market that the central bank is committed to breaking the back of the recent inflation surge?

If the Fed hikes rate by 75 basis points, that will lift the target rate to a 3.0-to-3.25% range. A market-based estimate of where the terminal rate will be in the near future currently projects a roughly 4.25% objective at some point in early 2023. In turn, that implies there’s another 75-basis-points hike in the cards beyond tomorrow’s increase.

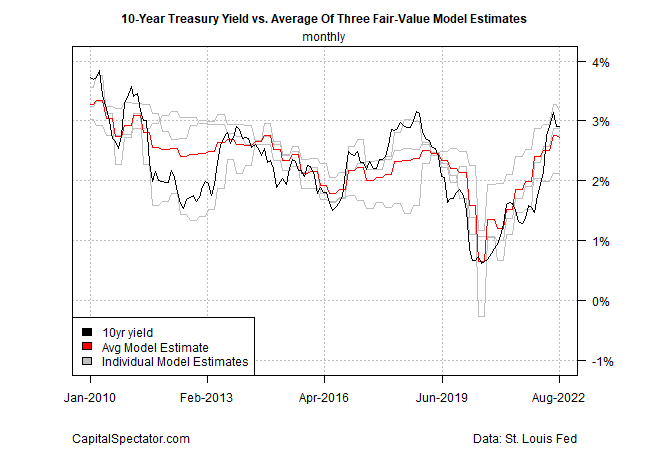

CapitalSpectator.com’s fair-value model currently shows the 10-year yield at 2.90% as of August, based on the average of three models (see details here). That compares with the market’s 10-year rate moderately above that average estimate. On this basis, the model’s implicit forecast is that the 10-year rate’s upside bias is relatively constrained compared with recent history, when the 10-year yield was below the average fair-value estimate.

In the short run, changes in the 10-year rate are mostly noise and so our model is of limited use for deciding what’s coming in the days and weeks ahead. Looking further ahead, a key question is how the models’ inputs – economic growth, inflation and other factors – change the fair-value estimate?

Keep in mind that economic growth is slowing and recession risk is rising – trends that imply a lower 10-year yield. To be fair, the outlook for the fourth quarter is unusually cloudy and so it’s hard to get a read on how inflation pressures interact with softer estimates for economic activity. We are, it seems, at a point of maximum uncertainty for modeling such factors.

Bottom line: our fair-value estimate suggests the upside bias for the 10-year rate has moderated lately. That doesn’t mean the 10-year rate can’t rise further from current levels. But without clear signs that inflation will stay elevated, a case is building for expecting that we’re approaching a cyclical top for the 10-year rate before the year is out.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno