There’s a lot of uncertainty about what a Trump presidency means for the US economy over the medium- and long-term horizons, but for the moment there’s nothing fuzzy about sentiment in the Treasury market. The benchmark 10-year yield jumped to its highest level since January in the two trading days since a billionaire reality TV star won the keys to the White House.

The sharp, sudden increase in yields has reverberated in world markets, particularly for emerging markets. As Reuters reports this morning,

Emerging market shares and currencies slumped on Friday as investors feared higher U.S. interest rates under incoming President Donald Trump will spark capital outflows, while European bond yields were on course for their biggest weekly rise in a year.

The selling was especially pronounced in emerging market bonds. The VanEck Vectors JP Morgan Emerging Market Local Currency Bond ETF (EMLC) has tumbled more than 7% over the past two days as of Thursday’s close (Nov. 10). Equities in emerging markets have also taken a hit, although the damage is lighter, based on Vanguard FTSE Emerging Markets ETF (VWO), which is off roughly 5.5% in the two days through yesterday.

The US stock market, on the other hand, has given President-elect Trump a ringing endorsement. The SPDR S&P 500 ETF (SPY) is up 1.3% since Tuesday’s close. Foreign stock markets in developed countries, by contrast, have held steady over the last two sessions, based on Vanguard FTSE Developed Markets ETF (VEA).

The main focus, however, is on the Treasury market, which is signaling a dramatic shift in expectations.

“We do view the election of Donald Trump as a game changer,” Adam Donaldson, head of debt research at the Commonwealth Bank of Australia, tells Bloomberg. “The strong bias toward fiscal expansion and inflationary policy represents a stark change to the malaise of recent years. This opens the door for the Fed to hike in December, but also more quickly in 2017 and 2018 than previously expected.”

Donaldson’s outlook certainly finds support in the Treasury market. The 10-year yield leaped to 2.15% yesterday, based on daily data from Treasury.gov. The policy sensitive 2-year yield is also on the march, rising to 0.92%–the highest since March.

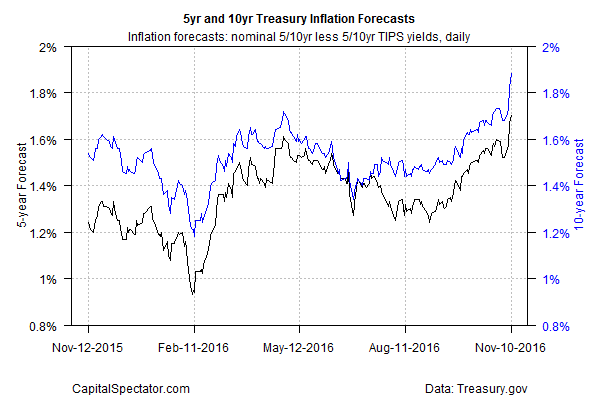

The Treasury market’s inflation forecast has turned conspicuously higher as well in the post-election trading sessions. The yield spread for the nominal 10-year Note less its inflation-indexed counterpart is now 1.88% as of yesterday, the highest since July 2015.

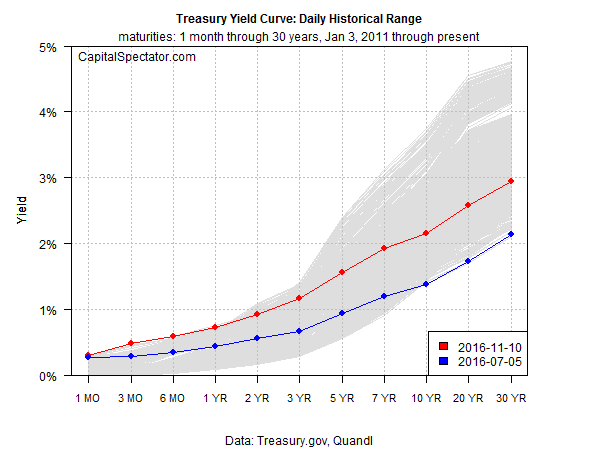

The latest shifts in the bond market are also reflected in the Treasury yield curve, which has steepened sharply over the past two days. Yields at the short end of the curve are now at or near the highest levels since 2013 while longer maturities have popped to a middling range relative to the history for the past three years.

Curiously, Fed funds futures haven’t changed all that much since the election. Although this market is pricing in a roughly 72% probability (as of Nov. 10) that the central bank will squeeze policy at the December FOMC meeting, based on CME data, that’s roughly in line with the numbers from earlier this week and well below the 90%-plus level that would indicate a higher level of confidence.

But Edouard Carmignac, a French investment banker and fund manager, tells the FT today that the fix is in. Trump’s election victory “will surely raise inflation expectations, worsen fiscal balances and put considerable upward pressure on bond yields. Under these circumstances, market permitting, the Fed will clearly be encouraged further to raise rates in December.”