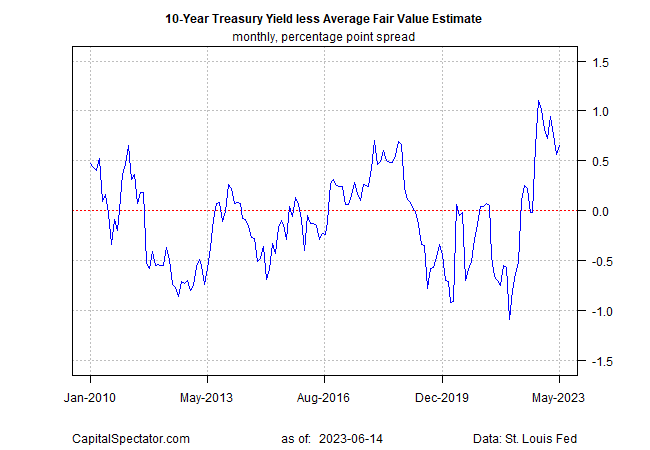

The market continues to price the US 10-year Treasury yield at a relatively wide spread over its “fair value”, based on the average estimate of three models assembled by CapitalSpectator.com for May 2023.

The first question: Will today’s policy announcement from the Federal Reserve change the outlook for interest rates and our fair-value estimate. Fed funds futures this morning are pricing in a 90%-plus probability that the central bank will put its rate hikes on pause in today’s FOMC statement (scheduled for 2:00 pm eastern).

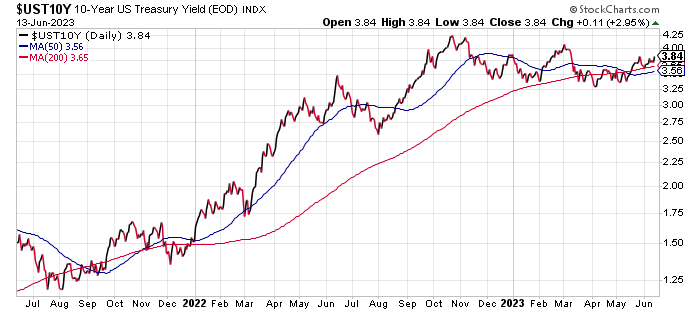

Meanwhile, the 10-year yield on Tuesday (June 13) edged up to 3.84%, a relatively middling level for the range-bound market that’s prevailed so far this year.

Today’s fair-value modeling of the 10-year yield is 2.92%, fractionally above last month’s estimate. That’s nearly 100 basis points below the current market yield. The implication: the market yield will fall, the model estimate will rise, or some combination of the two will unfold in the weeks and months ahead due to changing economic, inflation and markets data.

The relatively wide spread for the market yield exceeding fair value has persisted for the past nine months, fluctuating between roughly 50 and 100 basis points.

Note that the spread has narrowed recently but remains comparatively wide. The gap suggests that the upside bias for the 10-year yield is limited. A more ambitious forecast of the analytics translates to a forecast for a lower 10-year yield in the months ahead.

Today’s Federal Reserve announcement could be a critical variable in changing the calculus. Using a simple model of inflation and unemployment to gauge current Fed policy suggests that monetary policy is moderately tight. In turn, that profile adds to case for expecting the 10-year yield to hold steady or drift lower in the near term. Let’s see if today’s FOMC statement, followed by a press conference with Fed Chairman Powell, revises expectations.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno