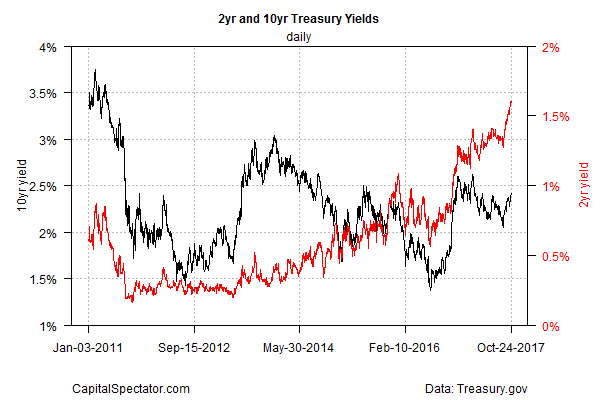

The Treasury market continues to price in firmer odds of another rate hike by the end of the year. Notably, the policy sensitive 2-year yield edged up to 1.60% yesterday (Oct. 24) for the first time since 2008, signaling that a hawkish bias continues to dominate fixed-income trading.

The benchmark 10-year yield advanced too, although this rate’s upward bias remains well below its peak in recent years. The 10-year rate inched up to 2.42% on Tuesday, a five-month high, based on daily data via Treasury.gov.

DoubleLine Capital Chief Investment Officer Jeffrey Gundlach, an influential voice in the bond market, tweeted on Tuesday that “The moment of truth has arrived for secular bond bull market!”

Meanwhile, Fed funds futures are estimating a 97% probability that the Federal Reserve will lift its current 1.0%-to-1.25% target rate at the December FOMC meeting, based on CME data this morning.

Growing speculation that President Trump is considering replacing Fed Chair Janet Yellen with Fed Governor Jerome Powell or Stanford economist John Taylor is also part of the mix for the bond market lately. Taylor’s considered a hawkish choice, based on his work for developing a set of rules for the central bank’s interest-rate decisions. According to CNBC, the so-called Taylor Rule indicates that Fed funds should be significantly higher at roughly 3%, more than double the current 1.0%-to-1.25% target range.

Another factor lifting rates lately: strengthening expectations that Congress will pass tax-reform legislation, including the prospect for a cut in tax rates that’s considered a pro-growth measure by the administration. “It’s going to be all growth,” Trump recently asserted. “That growth can be staggering.” Many analysts are skeptical, but for now the bond market’s inclined to assume that a tax cut will be a positive for the economy.

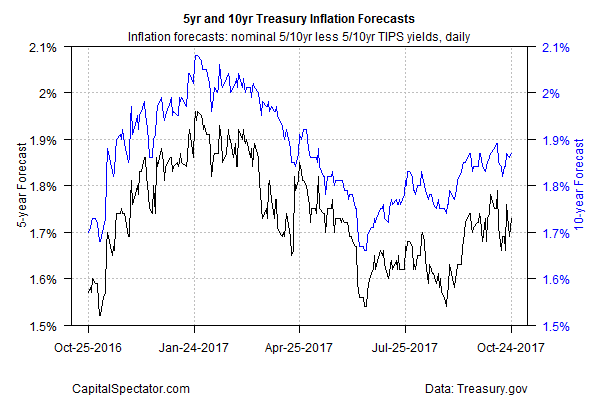

Despite the recent rise in yields, the Treasury market’s implied inflation forecast remains relatively subdued and steady. The yield spread for the nominal 5-year rate less its inflation-indexed counterpart, for instance, is currently 1.73% — roughly the average for the range so far in 2017 and moderately below the Fed’s 2.0% inflation target. The implication: there’s still a case to forgo more rate hikes in the near term.

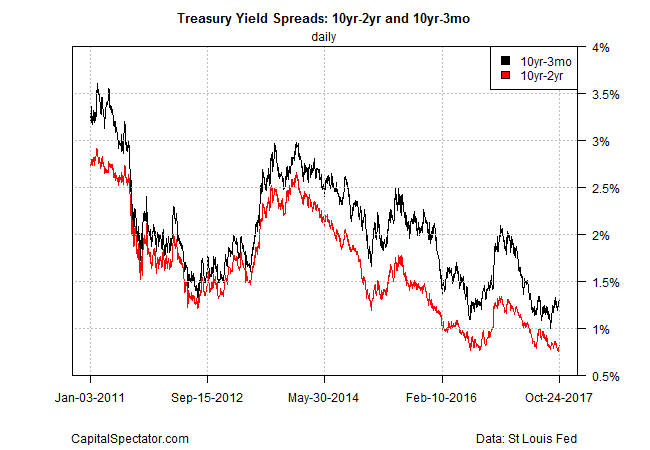

Looking at rates through the prism of key yield curves continues to reflect compressed spreads. For instance, the 10-year/2-year spread edged up to 82 basis points on Tuesday, although that’s still close to a multi-year low.

Note, however, that rates for long maturities have been creeping up lately and so the flattening of the yield curve that’s been in play for much of the year appears to be reversing, albeit on the margins so far.

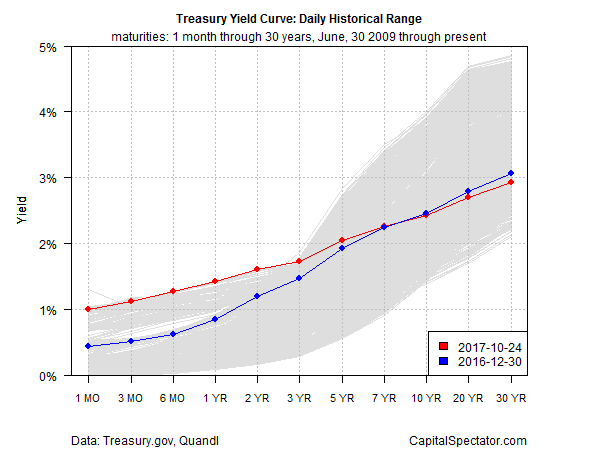

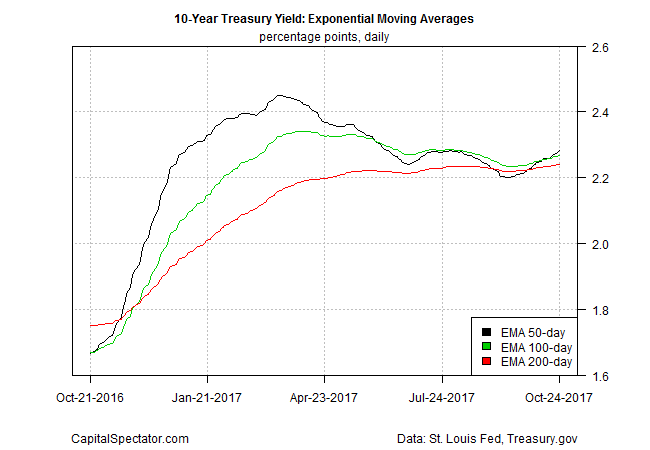

The bottom line: upward momentum for yields is conspicuous. That’s been true for the 2-year rate for some time. The big change of late is the revival of a rising trend for the 10-year yield, based on a set of exponential moving averages. Until or if the economic news delivers an attitude adjustment, it’s reasonable to assume that an upward bias in Treasury rates for the immediate future will prevail.

But as the FT points out, the lack of firmer expectations on inflation leaves room for debate on whether rates can rise for the intermediate term and beyond. “This is not about economic optimism,” notes Guy Lebas, chief fixed-income strategist at Janney Montgomery Scott. Bond-market “sell-offs that don’t have an economic thesis behind them don’t typically sustain.”