Consumer spending perked up last month while disposable personal income (DPI) stagnated in March, according to today’s monthly update from the US Bureau of Economic Analysis. Meanwhile, the Labor Department reports that initial jobless claims fell significantly more than expected last week, touching a 15-year low and thereby providing a bullish signal for next week’s monthly update on payrolls for April. From the vantage of today’s spending and income numbers, however, the first quarter ended with mixed results.

Consumption advanced 0.4% vs. the previous month, ramping up from February’s 0.2% rise. But the improvement was marred by the news that DPI was flat last month. Overall, it’s a mixed batch of numbers. Today’s update also shows that the annual trends for both income and spending continue to decelerate.

The softer year-over-year gain in private-sector wages—the foundation for consumer spending—dipped last month to 4.3%. That’s still a decent increase, if it holds. Unfortunately, recently history leaves room for doubt. Indeed, the current 4.3% annual pace is down sharply from the 6% year-over-year rise posted in December.

There’s also a conspicuous downward bias weighing on personal consumption expenditures (PCE) for the annual comparison. Spending through March increased 3.0% vs. the year-earlier level, the slowest pace in nearly five years.

The optimistic view is that the recent weakness is just a temporary setback. “What we went through over the first quarter was simply a soft patch related to the weather and port strikes,” says Tom Porcelli, chief U.S. economist at RBC Capital Markets. “Ending the quarter on a pretty strong note like spending did is indicative of an economy that seems poised to rebound.”

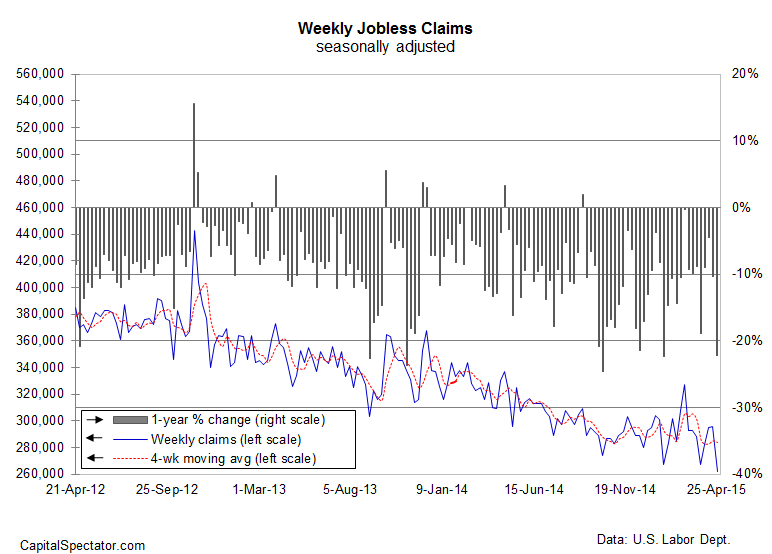

Today’s jobless claims report certainly supports Procelli’s upbeat view. New filings for unemployment benefits fell more than expected, easing to a seasonally adjusted 262,000 for the week through Apr. 25.—the lowest since Apr. 2000. More impressively, claims fell 22% last week vs. the year-earlier level. In short, jobless claims represent Exhibit A in the case for expecting a stronger second quarter.

Stress testing the case for optimism continues with tomorrow’s monthly report on April’s business sentiment in the manufacturing sector via the ISM data. The main focus, however, is next week’s payrolls data, starting with the ADP Employment Report for April (due on May 6), followed by this month’s official jobs report from Washington on Friday (May 8).