Treasury yields held on to their modest rebound this week through Thursday’s close, ahead of the Federal Reserve annual conference that begins today in Jackson Hole, Wyoming. No doubt the discussions will center on whether the central bank will begin raising interest rates at its Sept. 16-17 policy meeting. Earlier this week, New York Fed chief Bill Dudley threw cold water on the prospects for tightening next month, explaining that the case for a rate hike looked “less compelling” relative to two weeks earlier. The catalyst for his cautious view, of course, is the recent market turbulence. But in the wake of this week’s US economic reports, it’s not obvious that the macro trend is stumbling for the world’s largest economy, even if Mr. Market’s hysterics of late suggest otherwise.

“The United States relies more than any other developed economy on demand within our own borders,” the chief economist at Northern Trust tells The New York Times. “While the focus in the past three weeks has been on international instability, this should position us to withstand the consequences of recent market volatility,” explains Carl Tannenbaum.

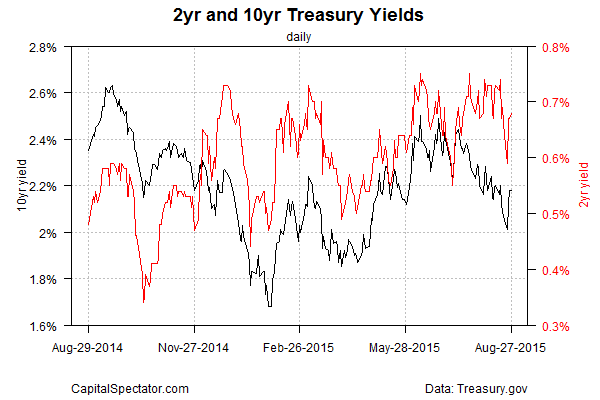

The Treasury market appears to agree–reluctantly, cautiously and ever so gently this week. After the benchmark 10-year yield briefly dipped below 2% on Monday on an intraday basis—the lowest level since late-April—the rate has bounced back, settling at 2.18% yesterday (Aug. 27), according to Treasury.gov data. That’s just below the level that prevailed before the latest selling wave began a week ago. In short, the key Treasury yield has effectively dismissed this week’s market turbulence as noise.

Ditto for the 2-year yield, which is considered the most sensitive spot on the yield curve for rate expectations. The hefty U-turn for this maturity in recent days suggests that the market’s not yet willing to completely dismiss the idea of raising rates at next month’s Fed meeting. It’s still a long shot, or so the Fed futures markets is telling us as of Aug. 27. Yet it’s also clear that the odds for squeezing are a bit higher compared with this past Monday, when markets were in free fall.

Kansas City Fed President Esther George is certainly inclined to pull the trigger sooner rather than later, although she’s a non-voting member of the committee that sets interest rates and so her comments fall into the category of theoretical. In any case, she said on Wednesday that

Policy makers are always trying to divine whether the forecast should adjust because of what they’ve seen. I think you have to be particularly careful when markets move, whether that is a signal of something more fundamental or whether it is a readjustment of some sort.

This week’s events complicate the picture but I think it’s too soon to say it fundamentally changes that picture, so in my own view, the normalization process needs to begin and the economy is performing in a way that I think it’s prepared to take that.

Nonetheless, it’s unlikely that any hard decisions will be made one way or the other before next week’s employment report for August hits the streets on Sep. 4. Yesterday’s encouraging slide on new jobless claims for last week’s tally suggests that the labor market is still poised to grow at a 200,000-plus rate this month. Yet it’s not obvious that this news alone, assuming it’s confirmed, will suffice to convince the Fed to start tightening next month.

Recent updates suggest that the US economy will continue to grow, although the Atlanta Fed’s GDPNow model is currently projecting a sharp slowdown in third-quarter GDP growth to 1.4% vs. 3.7% in Q2. But it’s still early for this quarter’s hard data and so it’s possible we’ll see upward revisions for the near-term outlook. The Atlanta Fed’s incrementally higher revisions of late for Q3 GDP expectations suggest as much.

Meantime, keep your eye on the effective Fed funds rate, which has been creeping higher lately. Economist Bob Dieli at NoSpinForecast.com pointed out this upward trend, wondering if it’s a clue of the Fed’s efforts for laying the groundwork for tightening. That’s a thin reed for seeing a rate hike next month, although if this rate continues to rise it may be a sign that there’s a major attitude adjustment coming for decisions regarding Sep. 16-17.

The bottom line: there’s still enough skepticism about the US macro outlook to argue that it’s premature to raise the Fed’s target rate. The problem, however, is that the economic case for hiking will remain debatable for the foreseeable future—if we’re using historical metrics that were relevant and widely accepted prior to the Great Recession. In the post-crisis world, however, the trend is weaker, which raises the critical question: Are the standards for tightening policy different? Yes, or so it seems… until (or if) Janet Yellen and company tell us otherwise.