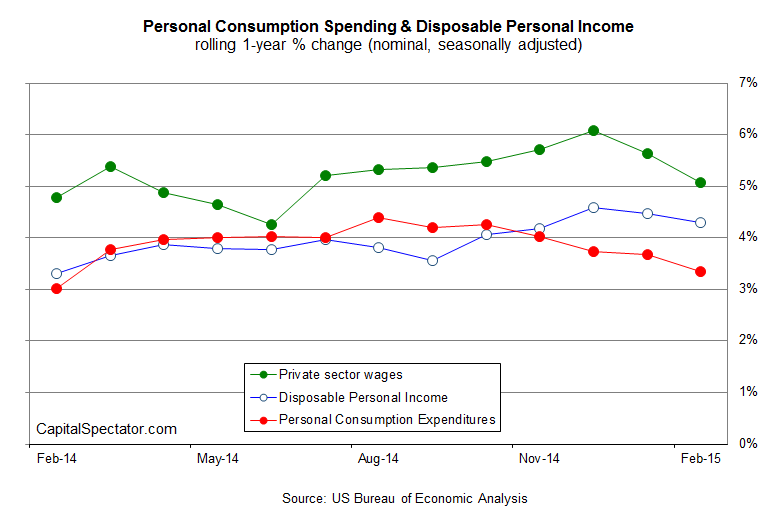

Consumer spending in the US revived last month, rising 0.1% in February vs. January, the Bureau of Economic Analysis reports. The gain is slightly below expectations among economists, although the increase is the first monthly advance since last November. The directional shift back into positive territory is encouraging, but a closer look at the trend suggests that a softer run of growth persists. It’s still reasonable to wonder if the harsh winter is the source of the weaker growth, in which case warmer weather is the antidote. Based on today’s update, however, it’s clear that spending’s rise in the consumer sector continues to decelerate in annual. In fact, the same is true for disposable personal income, which continued to post a lesser rate of growth last month vs. the year-earlier level.

The key weakness in today’s numbers is the ongoing slide in private-sector wages, which slowed to a 5.1% rise through February in annual terms. That’s still a respectable gain, but the question is whether the slowdown will roll on? Indeed, the year-over-year rate of growth in private wages has decelerated at a robust pace for two months in a row. Perhaps that’s simply payback after the improvement in the trend during last year’s second half.

In any case, today’s release certainly provides more support for thinking that first-quarter GDP growth will slip below 2014:Q4’s sluggish 2.2% rise. The case for downgrading Q1 expectations is old news at this point (see last week’s estimate for Q1 GDP and the February update on the Chicago Fed National Activity Index, for instance). Based the Atlanta Fed’s real-time estimates from last month, GDP’s estimated pace for the first quarter is virtually flat.

The good news is that the early signals for March look brighter, including the upbeat survey numbers for the manufacturing and services sectors via this month’s flash estimates from Markit Economics.

As a result, deep trouble in the US economy is still a slim risk. At the same time, the case for arguing that economic growth is accelerating is no longer compelling. Maybe we’ll learn otherwise as the rest of the March reports arrive in the weeks to come. Meantime, it appears that the stronger run of growth that we saw in late-2014 is skidding back into the old habit of modest growth.

Unless, of course, it’s really all about the weather. If it is, we’ll see convincingly stronger numbers in the March comparisons. There’s a mild bit of good news on this front via the weekly updates of the Johnson Redbook Index lately. This measure of national chain-store sales has been inching higher this month, although the high-2% advances on a year-over-year basis are still relatively soft vs. the 3%-4% annual gains posted in January.

The next major economic release for March arrives on Friday (Apr. 4) via the monthly payrolls report from Washington. For the moment, however, analysts are downsizing estimates. Private payrolls are expected to increase by 240,000 in March vs. the previous month, according to Econoday.com’s consensus forecast. A decent advance, but well below February’s 288,000 rise.

Pingback: Consumer Spending Increases Slightly