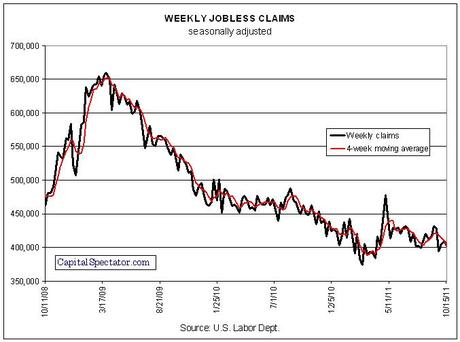

Today’s update on new jobless claims is encouraging because of what didn’t’ happen. New filings for unemployment benefits didn’t rise last week, which keeps hope alive that a new recession can be avoided for the foreseeable future. But while new claims dropped by 6,000 last week to a seasonally adjusted 403,000, this mild decline isn’t all that convincing. The ranks of the newly unemployed continue to swell each week by roughly 400,000, a stark reminder that the labor market is still struggling. As a result, the economy remains vulnerable, even if it’s not at the tipping point.

If jobless claims surge higher at some point, so will the odds that another recession is upon us. By that standard, today’s numbers suggest that the sluggish growth will prevail. But how much confidence do you have that next week (or the week after) will dodge a bullet as well?

No one can ignore the rising pressure on the economy. As one example, consider how the St. Louis Financial Stress Index compares with the broad economic trend (Chicago Fed National Activity Index) these days. As the chart below shows, the pressure is rising at a time when growth momentum has been decelerating. That’ a toxic mix, and if it continues, well, the outcome is all but assured.

There are plenty of other warning signs as well, such as the rolling 12-month percentage change in real consumer spending and real average hourly earnings. Joseph Ellis, author of Ahead of the Curve: A Commonsense Guide to Forecasting Business And Market Cycle, cites these metrics as among the more valuable indicators for evaluating the outlook for the macro cycle. Unfortunately, the recent numbers don’t look encouraging, as the chart below shows.

Persistently declining real wages and earnings on a year-over-year basis are hardly the raw material for producing robust periods of economic growth. But as long as the labor market doesn’t succumb, the forces of darkness can be held off. Still, the defenses are weak, and perhaps weakening.

“We’re running in place,” says Scott Brown, chief economist at Raymond James. The latest jobless claims numbers are “consistent with lackluster to moderate growth in the job market and the economy.”

Michael Woolfolk, senior currency strategist at BNY Mellon, advises that the latest updates on payrolls and retail sales have “effectively removed the double-dip scenario for the U.S.” Today’s drop in jobless claims is another piece of supporting evidence for this view, he notes. “But we are still a long distance from the 200,000 new jobs a month we need for a sustainable improvement in the unemployment rate.”

Meantime, the un-recession rolls on.