Knowing why an investment strategy has stumbled is just as important as recognizing why it succeeded. This obvious-but-often-unheeded bit of wisdom comes to mind after reading yesterday’s Bloomberg story that seven large, public US university endowments posted disappointing results for the year through the end of June 2016. “It was a bit of a bloodbath,” said Jagdeep Bachher, chief investment officer at the University of California system. The weakness is surprising because the year through the end of this year’s first half generated a modest upside bias for the Global Market Index (GMI), an unmanaged benchmark that holds all the major asset classes in market-value weights.

But that upside bias was nowhere in sight for the endowment funds, as a chart in the Bloomberg article reminds.

You can’t tell much from one-year returns, of course—especially for portfolio strategies run by endowments. These tend to be complicated beasts, which is probably the source of the trouble. In any case, crunching the numbers across various time windows and focusing on multiple risk dimensions is essential for understanding what’s going on. That said, there are legitimate issues of concern when a strategy falls well short of a simple benchmark that, in theory, is a reasonable yardstick for an investment mandate.

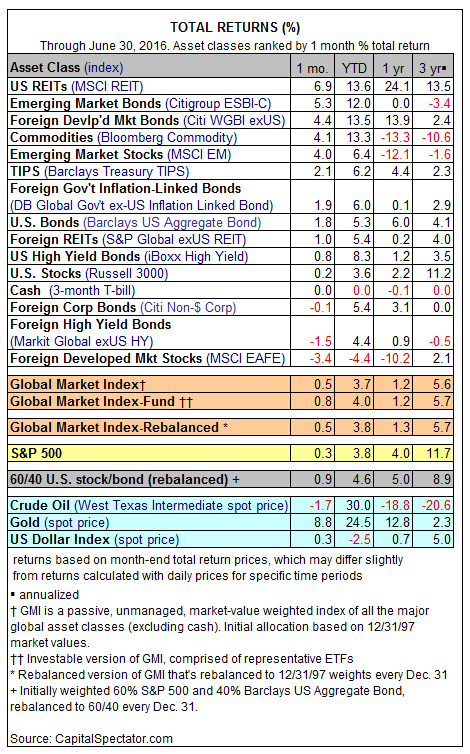

With that in mind, GMI posted a 1.2% total return for the 12 months through June 30, 2016, as originally reported here. That’s a weak result, but the source of GMI’s weakness for that period is clear: low and negative returns in the passive benchmark’s major allocations, particularly for foreign stocks. For perspective, let’s review the table of performance data for GMI’s components at that point in time.

Note, too, that an ETF-based version of GMI (GMI.F) was also higher by 1.2% for the year through this past June 30. Flat-to-modestly higher results over that span can also be found in publicly traded asset allocation products. The Vanguard Star fund (VGSTX), for example, posted a fractional gain for this 12-month period, although just barely. But if this low-cost, plain vanilla mutual fund with a global asset allocation mandate can keep its head above water, why can’t endowments with sophisticated oversight deliver comparable results?

I don’t have the answer since I’m not privy the full boat of historical results, but I can guess. Having dissected hundreds of strategies through the years, my gut tells that the investment methodologies in the endowment funds under scrutiny are overly complicated and pricey, and perhaps slightly misguided. Exactly how the complication and misguidance affects results is the critical issue. That requires a thorough review of the strategy and so for the moment we’re at a dead end.

But designing robust investment strategies isn’t rocket science, especially for endowments, which generally have long time horizons. The problem is often that large institutional strategies tend to get bogged down in complication and committees–two factors that tend to be inversely related with satisfactory investment results.

An obvious example: the recent rush into hedge fund allocations, which for pension and endowment funds often translated into holding dozens of products. If you’ve ever wondered what analytical hell is like, just imagine the thankless task of monitoring and evaluating a spectrum of hedge fund strategies in real time. No wonder that many institutions have soured on hedge fund allocations in recent years. But there are still plenty of believers. A Reuters headline from earlier this year reported: “Public pensions stick with hedge funds despite frustrations.”

It’s not clear that hedge funds are weighing on the endowments cited in the Bloomberg article. On the other hand, it appears that something’s amiss. The story suggests that offshore equities are to blame. That’s a reasonable guess. As the table above shows, there was a lot of red ink in the tailing one-year return column for foreign stock markets as of this past June.

But keep in mind that GMI has a relatively heavy weighting in foreign equities too—roughly 23% of assets as of June 30. Did the endowments hold even more? If so, why? What methodology led to a comparatively big bet?

Actually, asking these type of questions after the fact is misguided. Rather, the focus should be on reviewing a strategy from the bottom up (and the top down) when the best-laid plans go off the rails.

Granted, it’s unclear what exactly is wrong with these endowment strategies, at least from the perspective of one news story. Perhaps it was only a temporary bout of volatility and all is well once more. But when a strategy has trouble matching a passively run portfolio with a similar mandate—maximize returns over the long term by holding a broad set of asset classes—it’s usually a wake-up call.

Pingback: Knowing Why an Investment Strategy Has Stumbled - TradingGods.net

Pingback: News Worth Reading: September 16, 2016 | Eqira