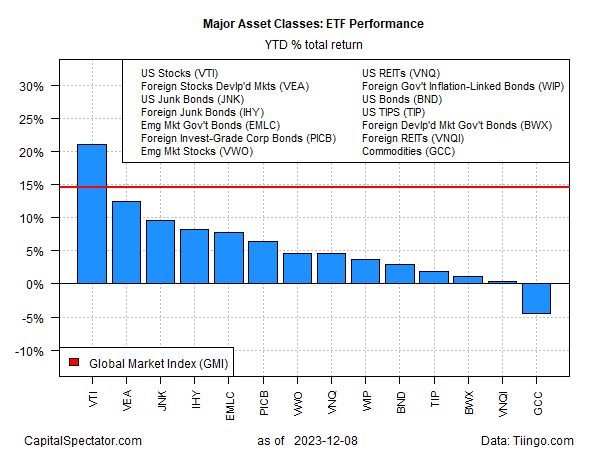

With just three weeks left to the year, nearly all corners of global markets are on track to post gains for 2023, based on a set of index ETFs. The US stock market is still leading the field by a wide margin. Meanwhile, commodities are the downside outlier.

Vanguard Total US Stock Market (VTI) close on Friday (Dec. 8) with a 21.1% year-to-date gain. That’s far ahead of other markets. The second-best performer this year – developed-markets stocks ex-US (VEA) – is up 12.5%.

Commodities overall are struggling this year, in no small part due to sliding energy prices. The US crude oil benchmark (West Texas Intermediate) is down more than 11% year to date. A broad measure of commodities is doing better, but the 4.5% loss this year for WisdomTree Enhanced Commodity Strategy Fund (GCC) is a reminder that beta for the asset class remains on the defensive.

The general upswing in most markets has lifted the Global Market Index (GMI) this year. GMI holds all the major asset classes (except cash) in market-value weights and represents a competitive benchmark for multi-asset-class portfolios. GMI’s 14.5% year to date gain not only marks a strong rally for the benchmark, it’s also a reminder that beating a passive, multi-asset-class strategy has been tough in 2023.

The question is whether this year’s widespread gains in nearly everything are a sign of things to come in the new year? As The Wall Street Journal observes today:

“The simultaneous surge across assets has sparked debate about whether the ‘everything rally’ marks the arrival of a lasting bull market—or just a fleeting sugar high at the end of the Federal Reserve’s tightening cycle.”

The answer is almost certainly linked with upcoming decisions by central banks, including this week’s policy meeting (Wed., Dec. 13) at the Federal Reserve. Expectations that rate hikes are history and rate cuts are likely in 2024 has been a critical factor for recent market gains.

“Investors have been betting that policymakers in the US, the eurozone and the UK will start loosening monetary policy early in the new year, fueling an easing in financial conditions for businesses, as they focus on falling headline inflation readings,” notes Financial Times. “But those expectations will be tested in coming days at meetings of the US Federal Reserve, the European Central Bank and the Bank of England, all three of which have signaled they want clearer evidence of weakening labor markets before cutting rates.”

The crowd expects that the Fed will keep its target rate unchanged at the next two meetings, but the possibility of a rate cut is in play for March, based on Fed funds futures.

“We maintain our call for the Fed to start cutting rates by mid-year, but it is contingent on inflation continuing to trend lower and further weakening in economic activity,” writes Nationwide economist Kathy Bostjancic.

Ongoing disinflation and softer economic growth will likely favor rate cuts at some point in 2024. The bigger question: Would risk markets continue to rally with those conditions? For bonds, yes. The outlook for stocks, by contrast, is more complicated. If economic output slides too far too fast, equities would probably face stronger headwinds.

On the other hand, forecasts for the so-called soft-landing scenario favor higher equity prices in the new year, according to some analysts. If inflation continues to slow and economic growth moderates and a recession is avoided, that could be the sweet spot for stocks.

Comerica’s Chief Investment Officer John Lynch sees that path playing out, in part due to upbeat estimates for earnings. “Fortunately, corporate profits are set to gain traction as we expect market growth to reflect earnings gains. Our base case scenario has the S&P Index fairly valued in the 4,750 range by year-end 2024,” he writes.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Pingback: Monday links: unprecedented employment - QuantInfo - Empowering Algorithmic Trading Insights