The playing field is riddled with imperfect information in real time, long response lags, unclear relationships between economic and financial variables, and a hefty dose of uncertainty linked to behavioral risk. Throw in a high degree of geopolitical risk at the moment vis-a-vis the Ukraine crisis for good measure. Modeling how all this interacts in the months ahead for purposes of setting monetary policy is like trying to grasp all the possible moves in a game of chess.

Enter the Federal Reserve, which is about to embark on its most challenging period for policy adjustment in a generation, if not in all of its history since 1913. But, hey, no pressure.

Let’s begin with what seems highly likely: the first rate hike of the pandemic will start next month. Fed funds futures are pricing in a virtual certainty that the central bank will lift its current 0%-to-0.25% target rate at the March 16 FOMC policy meeting. The outlook is heavily skewed for a 25-basis-point increase (75% probability), but there’s a non-trivial estimate for a 50-basis-point increase (25% probability).

Analysts are also penciling in a string of hikes later in the year. Among the more hawkish outlooks: economists at Bank of America are forecasting seven quarter-point increases this year, with another four in 2023. On that basis, the Fed funds rate would rise to ~3.0% from the current 0%-to-0.25% range. In relative terms, that’s a hefty change.

But a lot can happen between now and 2023. Changes in monetary policy don’t occur in vacuum. Pity the poor central banker who’s charged with giving the impression that all the macro, geopolitical and behavioral factors can be quantified, analyzed and modeled to arrive at an optimal strategy for adjusting policy in real time. Good luck.

So, what to expect? History offers a guide, of sorts. Every US recession since the 1957-58 downturn has been preceded by an increase in the Federal funds rate. You can’t prove that recessions are triggered by rate hikes, but you’d be naïve to ignore the apparent relationship.

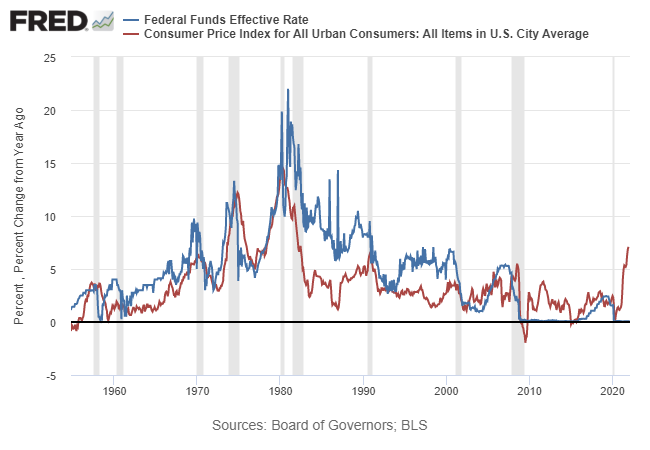

Further complicating the dynamic this time is the widely perceived notion that the Fed is late to the game of containing inflation’s surge. As the next chart reminds, the year-over-year increase in consumer prices has run far ahead of the target rate to a degree that’s unprecedented in modern times, a gap that suggests the Fed’s behind the proverbial eight ball and needs to tighten policy quickly and relatively sharply.

Unless inflation’s recent surge is temporary, triggered by transitory factors such as the global supply-chain disruption, which in turn is a byproduct of the pandemic. No doubt that and other factors are skewing the usual relationship between economic conditions, inflation and monetary policy. But figuring out the degree of the skew, and how long it will last, and how to play it differently this time is devilishly hard, if not impossible, in part because there’s no precedent for what’s been unfolding in the Covid-19 pandemic.

What is clear is that there’s a non-zero risk that if the Fed raises rates too far too fast, the economic expansion could reverse too sharply, perhaps unleashing a new recession. History strongly suggests that this is a distinct possibility. As the MIT economist Rudi Dornbusch famously quipped, “No postwar recovery has died in bed of old age—the Federal Reserve has murdered every one of them.” Will it be different this time?

Maybe, but successfully threading this needle will surely be unusually difficult. The good news, such as it is: Fed Chair Powell seems to understand that environment he’s in. As he explained recently, “We fully appreciate that this is a different situation. If you look back to where we were in 2015 ’16, ’17, ’18 when we were raising rates, inflation was very close to 2 percent, even below 2 percent.”

Today, inflation is currently running at 7%, and tomorrow’s January report on consumer prices is expected to move higher still. Meanwhile, the Fed’s target rate remains pinned at near-zero.

Recessions, it’s worth noting, are effective at reducing inflation. Every economic downturn since the 1950s has been effective at cutting pricing pressure substantially. That history begs the question: Is there really any other way to tame inflation?

As we ponder how to answer, and whether the Fed is up to the job this time, it’s useful to remember that the central bank’s history in tightening policy without creating recessionary conditions is less than encouraging. Even worse, the Fed was operating in “normal” conditions in decades past. This time, conditions are anything but normal.

The wisdom of Solomon would come in handy right about now.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report