Fixed-income investors looking for interest-rate cuts from the Federal Reserve are still waiting, but that hasn’t stopped low-rated bonds from posting strong gains in 2023.

The upside performance leader for US bonds year to date is Invesco Senior Loan ETF (BKLN), a “low” grade portfolio, according to Morningstar. But there’s nothing low grade about its return this year, which leads the field for a set of bond ETFs that track the major slices of US fixed income markets.

BKLN closed on Wednesday (Sep. 20) with a 9.7% total return so far in 2023. That’s head and shoulders over the near-flat performance for the US bond market overall, based on Vanguard Total Bond Market Index Fund (BND).

In distant second- and third-place performances for 2023 are a pair of US junk bond funds in short- and medium-term varieties (SJNK and JNK, respectively). Meanwhile, US Treasury securities with medium- and long-term maturities (IEF, TLH, and TLT, respectively) comprise the red-ink brigade at the moment for year-to-date results.

Bond investors hoping for encouraging signals from the Federal Reserve that its policy of raising interest rates was ending received mixed news yesterday. The central bank announced that it left its target rate range unchanged at 5.25%-5.50%, but suggested that another hike was possible and rate cuts weren’t on the near-term horizon.

“Chair Powell and the Fed sent an unambiguously hawkish higher-for-longer message at today’s FOMC meeting,” advises Citigroup economist Andrew Hollenhorst in a research note. “The Fed is projecting inflation to steadily cool, while the labor market remains historically tight. But, in our view, a sustained imbalance in the labor market is more likely to keep inflation ‘stuck’ above target.”

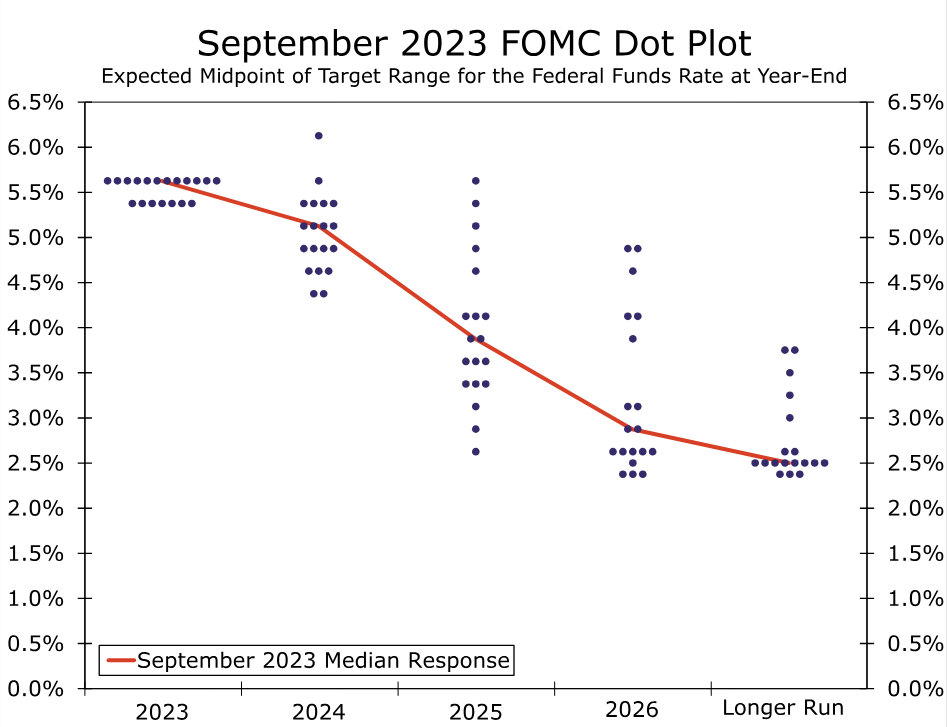

As for the Federal Reserve’s collective outlook for its policy rate, the new dot plot of expectations released yesterday was unchanged from the June estimates.

The median dot for the end of 2023 held steady at 5.625%. Economists at Wells Fargo note: “12 of the 19 members of the FOMC think it would be appropriate to hike rates by 25 bps at either the November 1 meeting or at the final meeting of the year on December 13.”

The median dot today stands at 5.125%. If the FOMC does indeed raise rates by 25 bps by the end of this year, then the Committee would cut rates by only 50 bps in 2024. Although the median dot for 2025 currently stands at 3.875%, there is a wide dispersion in the forecasts, which should be expected of a forecasted variable more than two years from now. In sum, the message from the FOMC today is higher for longer, in terms of interest rates.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report