There’s precious little hard data at this point for profiling the US economy in July, but the preliminary numbers so far suggest that growth will prevail and the manufacturing sector’s recent weakness will give way to a modestly stronger trend. We’ll know more when we see today’s flash July data for the US manufacturing purchasing managers index (PMI), scheduled for release at 9:45 am eastern–the consensus forecast sees the moderate growth rate in June ticking up slightly, according to Econoday.com. Meanwhile, the available July figures at the moment imply that the stronger pace of growth in June will carry over into this month.

One source of that upbeat outlook is yesterday’s weekly report on initial jobless claims, which fell to a four-decade low for the week through July 18. The unusually low level may be skewed due to seasonal factors bound up with retooling efforts at auto companies. But taking the data at face value continues to paint a bullish profile for the labor market and the economy overall. Consider, for instance, a monthly average of jobless claims that’s filtered through a probit model for estimating business cycle risk. This methodology indicates that the probability is virtually nil that NBER will declare this month as the start of a new recession.

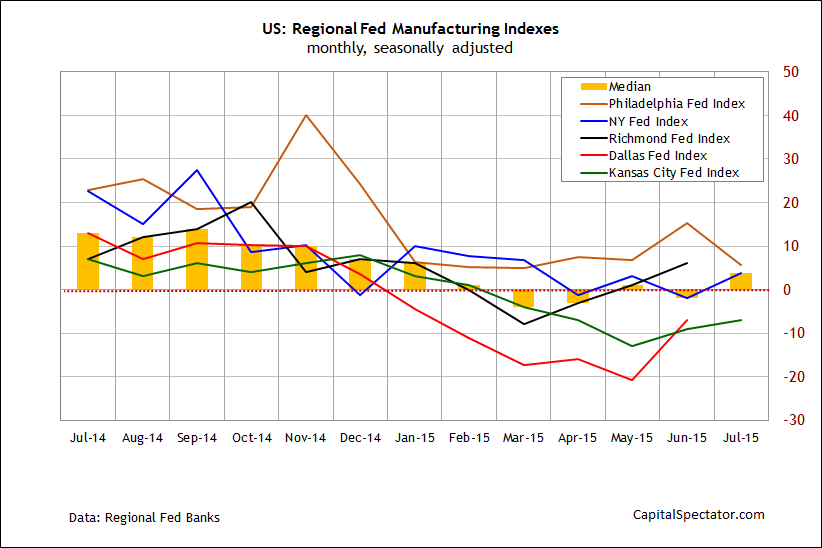

Next, let’s consider US manufacturing activity with July numbers, based on data published to date by the regional Fed banks. Three of the five indexes are currently available—the median value for this month hints at a moderate rebound after several weak months. Is this a sign that manufacturing’s stumble is easing? The numbers from three regional Fed indexes make a case for cautious optimism on this front.

We should, of course, take these early clues with a grain of salt. A complete set of July numbers for the US economy won’t be available until next month. But for the moment it’s fair to say that the leading edge of the monthly economic profile is off to an encouraging start.