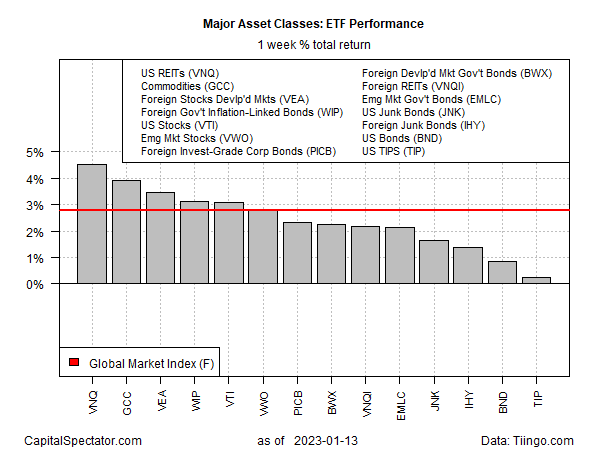

All the major asset classes scored gains last week, delivering more relief from widespread losses in 2022, based on a set of ETF proxies through Friday’s close (Jan. 13).

US real estate investment trusts led with a strong 4.5% increase. Last week’s rally in Vanguard US Real Estate (VNQ) left the fund near its highest close since September.

The rest of the field also posted gains, leaving no major slice of global markets untouched from the buying wave. But a new potential headwind for markets came into focus on Friday, when Treasury Secretary Janet Yellen advised that the US will reach its debt limit within days.

“Failure to meet the government’s obligations would cause irreparable harm to the US economy, the livelihoods of all Americans, and global financial stability,” she wrote. “I respectfully urge Congress to act promptly to protect the full faith and credit of the United States.”

Partisan politics in Washington raise doubts about how quickly a solution can be crafted. Until there’s a resolution, a new macro risk hangs over markets and the economy. “The Treasury debt limit is suddenly a serious threat to optimism we can avoid recession this year,” warns Mark Zandi, chief economist at Moody’s. “Unless lawmakers increase, suspend, or eliminate the limit, Treasury won’t have the cash to pay all its bills on time later this year. Financial markets and the economy will crater.”

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Meanwhile, the Global Market Index (GMI.F), an unmanaged benchmark maintained by CapitalSpectator.com, continued to recover last week, gaining 2.8%. This index holds all the major asset classes (except cash) in market-value weights via ETFs and represents a competitive measure for multi-asset-class-portfolio strategies.

Despite year-to-date rallies, most of the major asset classes continue to suffer losses for the trailing one-year window. Commodities (GCC) are the outlier, posting a modest 4.7% gain at Friday’s close vs. its year-ago price.

GMI.F’s one-year performance remains negative at -13. 3%.

Comparing the major asset classes through a drawdown lens continues to show relatively steep declines from previous peaks for most markets around the world. The softest drawdown at the end of last week: US junk bonds (JNK) with an 8.6% slide from its last peak.

GMI.F’s drawdown: -14.4% (green line in chart below).

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno