Today’s second-quarter GDP report is expected to deliver upbeat news about the US economy. Wobbly housing data may be telling a different story. It’s premature to assume the worst, but the weak year-over-year trends in several housing indicators suggest that today’s Q2 snapshot should be used cautiously as a guide to managing expectations for the near-term future.

Econoday.com’s consensus forecast calls for a 4.2% increase in real GDP for Q2 (seasonally adjusted annual rate). If the estimate is correct, output will expand at the strongest pace in three-and-a-half years and more than double the rate over this year’s Q1.

But if the economy is so strong, why is the housing trend so weak? Let’s consider some key indicators, starting with existing home sales.

Despite expectations for a strong Q2 for the US economy overall in today’s release, the appetite for purchases of existing homes faded in each of the past three months. The weakness has been spilling over to the year-over-year change: in every month so far this year, except for February, the annual pace has been negative. The red ink in the last four months marks the longest continuous run of year-over-year declines in four years.

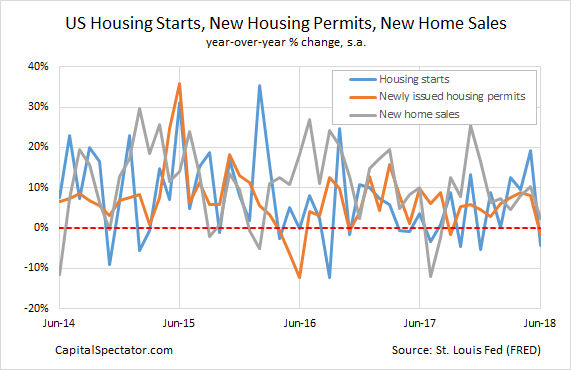

The data for new residential housing construction, newly issued building permits, and purchases of newly built homes look wobbly too. Housing starts and permits contracted on a year-over-year basis last month – the first simultaneous set of annual declines for these two key housing indicators in almost two years.

New home sales are still trending positive, but the annual pace in June decelerated sharply to 2.4% and so it wouldn’t be surprising to see negative comparisons in the months ahead.

Some analysts interpret the recent housing numbers as a warning sign for what lies ahead. “The housing market led the general economy out of the recovery and now it’s leading” it toward a slowdown, says Aaron Terrassa, senior economist at Zillow, a real estate data firm.

Is A New Recession Lurking? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

But by some accounts the housing weakness is less about economic conditions in general vs. issues tied to real estate. The slowdown in housing appears to be a reaction to rising prices, says Adam Contos, CEO at RE/MAX, a real estate firm. “Year-over-year prices have been climbing for more than two years now, which is great news for homeowners and sellers,” he observes. “The slower sales figures we’re seeing are tied to inventory more than anything else.”

Nonetheless, Robert Shiller, a Nobel Prize-winning economist, warns that the housing weakness “could be the very beginning of a turning point,” although he’s not prepared to officially declare that a peak has arrived.

If the soft housing data persists, the weakness will be increasingly worrisome if, as Edward Leamer advised in a 2007 research paper, “Housing IS the Business Cycle.”

Of the components of GDP, residential investment offers by far the best early warning sign of an oncoming recession. Since World War II we have had eight recessions preceded by substantial problems in housing and consumer durables.

It’s debatable if housing will remain an early warning sign for the next recession, although watching this corner of the economy surely deserves close attention in the months ahead.

Meantime, let’s note that the housing indicators above have shown periodic weakness in recent years without triggering a new recession and so caution is recommended in reading too much into the current numbers. Housing could be signaling trouble, but it could turn out to be noise. Since the end of the last recession in mid-2009, housing has suffered several mild downturns that gave way to renewed strength. With the broad macro trend still solidly positive, it’s too early to rule out another housing rebound.

Keep in mind, too, that this week’s review of a broad set of economic indicators reflects virtually zero recession risk. Perhaps housing is telling us that the tide is turning. Even if it is, slower growth overall doesn’t mean that a new NBER-defined downturn is near.

In the quest to develop a timely and reliable profile of real-time recession risk it’s clear that housing data should be closely monitored, but in context with a diversified set of indicators. Every downturn is different and so the mix of factors that lead to the next economic contraction aren’t likely to match the profile in previous slumps.

Whenever the next recession strikes, and for whatever reason, history reminds that a clear, dependable signal on this front will only be available after the fact. That leads to the only game in town: monitoring a broad set of indicators – frequently – along with several business-cycle benchmarks that reflect different methodologies (see The US Business Cycle Risk Report for an example).

By that standard, there’s still no sign of recession in the latest figures. Tomorrow, of course, is another day and so the shelf life for even the best business-cycle analysis is only 24 hours.