Consumer inflation in the US remained surprisingly hot in June, the Labor Department reported yesterday. Taken at face value, the numbers raise more doubts about the Federal Reserve’s assumption that the recent inflation surge is temporary. But a closer look at the numbers paints a more complicated profile.

It’s still too early to dismiss inflation risk, but the same is true for putting a fork in transitory assumption. In other words, despite the ongoing acceleration in the consumer price index (CPI) in yesterday’s report, nothing much has changed. Pandemic-related blowback is still creating noise and so the search for signal on the inflation front remains challenging and ongoing. The truth will out eventually, perhaps by the fourth quarter. Meantime, the debate rages and genuine clarity remains elusive.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

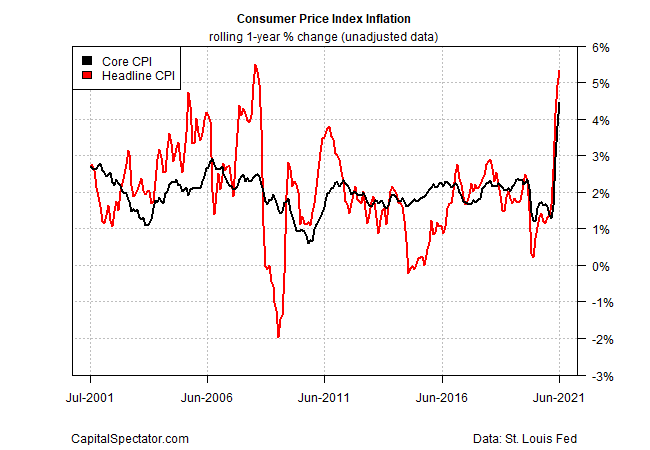

Let’s start with the main results in the June update. Headline CPI jumped to a 5.4% year-over-year increase, the highest since 2008. Core inflation (a more reliable measure of the trend) popped to a 4.5% annual pace last month – a 30-year high!

So-called base effects are still partly driving the annual changes. Unusually low prices during the depths of the pandemic a year ago continue to pair with this year’s rebounding prices to produce dramatic year-over-year increases. But the base effects are fading and with each passing month this factor explains less of the inflation trend.

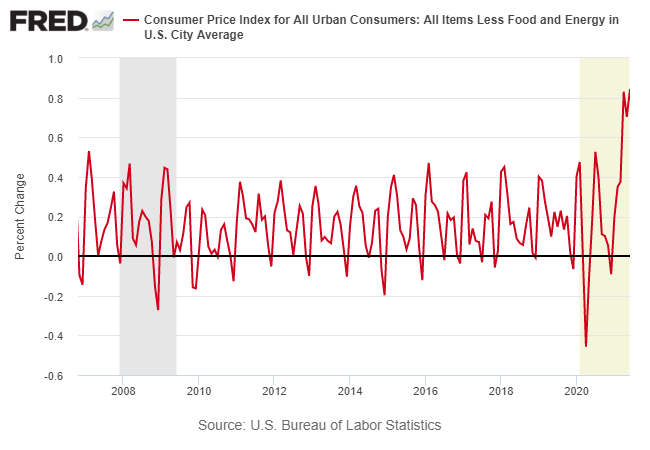

On that note, looking at inflation in monthly terms highlights that last month’s acceleration in pricing pressure transcends base effects. For example, core CPI’s monthly change (seasonally adjusted) remained elevated, rising to a 0.8% gain – far above the increases seen in recent decades. The longer this monthly change stays elevated, the weaker the transitory-inflation narrative becomes.

Monthly CPI numbers are noisy, however, and we should view these results cautiously. Nonetheless, the sustained increase clearly points to strong inflationary pressure in recent months.

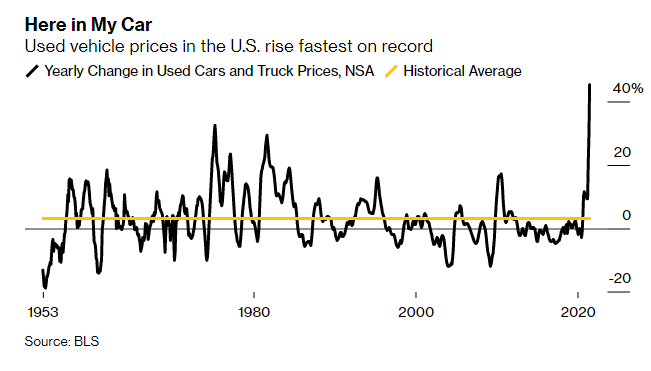

Digging deeper into the data reveals that a key driver of inflation’s acceleration last month is due to a handful of components that are expected to post softer gains, perhaps negative prices changes, in the months ahead. Notably, used vehicle prices continued to surge last month.

“Inflation surprised substantially to the upside in June but, once again, owing to outsized increases in prices in a few categories,” says Michelle Meyer, head of U.S. economics at Bank of America. “This reinforces the idea of transitory inflation.”

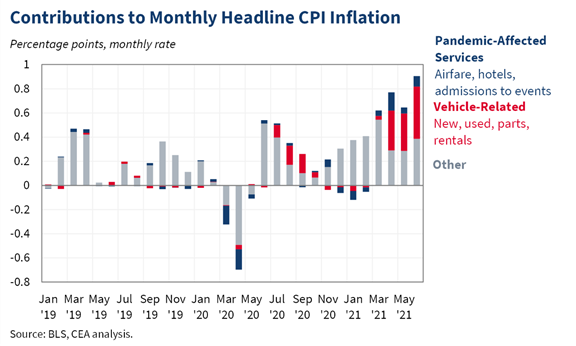

The White House Council of Economic Advisers tweeted a chart yesterday that highlights the outsized influence of vehicle-related prices in last month’s inflation report. Indeed, for the last three months, car prices have been unusually hot. The combination of recovering demand and reopening production bottlenecks has conspired to drive prices sharply higher. But this is likely a temporary change and a reversal of some degree is expected in the second half of the year as production capabilities rebound.

Meanwhile, “Bigger components (like shelter) are still well-behaved,” notes Carl Tannenbaum, chief economist for Northern Trust.

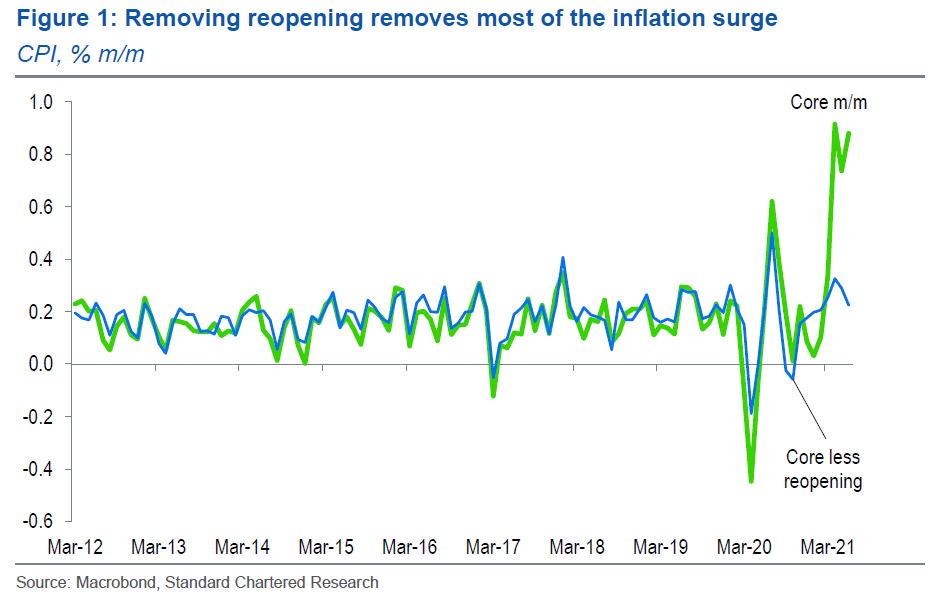

Steve Englander, a foreign exchange strategist at Standard Chartered, attempts to adjust inflation for the reopening shock and finds that monthly pricing pressure is significantly softer after this revision. Some may dismiss this as statistical fudging, but it’s another clue for at least considering the view that the runup inflation lately is less about regime shift vs. base effects.

The case for the transitory narrative may be weakening, but its not dead, at least not yet. But if there’s any validity to this forecast, the evidence will start to emerge soon… or not.

On that front, The Capital Spectator’s Inflation Trend Index (ITI) suggests that pricing pressure will peak this summer. ITI, an eight-factor modeling effort, attempts to provide a degree of forward guidance on the directional bias of pricing activity in real time, although it should not be used as a proxy for estimating the government’s inflation measures. Recent ITI updates suggested that reflation would peak in May or June. New data reveals those estimates were premature and the revised outlook points to July at the earliest. This could change, of course, as incoming numbers are published. Whatever comes, ITI will likely provide an early estimate for managing expectations, one way or the other.

Stepping back and considering the broad macro profile still leaves plenty of room for thinking that the disinflationary trend of recent decades remains intact, despite the pandemic-related interruption. Focusing on the last several months of inflation data suggests otherwise, but as Hoisington Investment Management reminds in its second quarter review, the “massive debt overhang” in the US continues to mount, creating an “obstacle” for the Federal Reserve’s efforts in reaching its goals for economic and inflation targets.

“The current economic growth and inflation rates of 2021 will be the highest for a very long time to come,” Hoisington predicts.

The main obstacle to a return to sustained growth in the standard of living, extreme over-indebtedness, was dramatically worsened by the multiple rounds of fiscal stimulus which has caused the temporary improvement in economic growth and inflation in the second quarter. No pathway out of this trap exists as long as the overreliance on debt remains the only tool of monetary and fiscal policy. The situation is no different in Japan and Europe. Thus, while long Treasury yields can increase over the short run, the fundamentals are too weak for yields to stay elevated. More debt does not cure a subpar economy mired in a debt trap. Given the above, our view is that the trend in long-term Treasury yields remains downward.

By this reasoning, the rise in inflation is noise and will soon give way to moderation. No one knows for sure if this will prove correct, but for now the Treasury market appears to be on board with this outlook. Although the 10-year yield rose yesterday to 1.42%, a six-day high, the trend for this benchmark rate still posting a downward bias after the recent bounce that started reversing in April .

If and when the 10-year yield starts to break to the upside, that may be an early clue that market sentiment is beginning to dismiss the transitory inflation narrative.

Perhaps an even bigger clue for embracing the higher inflation narrative would be if the Fed shifts its tone on the transitory narrative. For now, however, expect the central bank to maintain its current stance, advises Tim Duy at SGH Macro Advisors. “The Fed will continue to emphasize the ‘inflation is transitory’ story as it delays tapering until either the labor market recovers more fully or it is evident that labor supply is not bouncing back,” he writes in a note to clients. “That likely won’t happen until later this year.”

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Pingback: Consumer Inflation Hot in July - TradingGods.net