Amid signs that 2019’s slowdown in the US economy may be stabilizing, the US Treasury market appears to be flirting with firmer inflation expectations. It’s too early to know if the latest dance with reflation is noise or a preliminary signal, but the recent U-turns in the market’s implied inflation estimates deserve close monitoring in the weeks ahead.

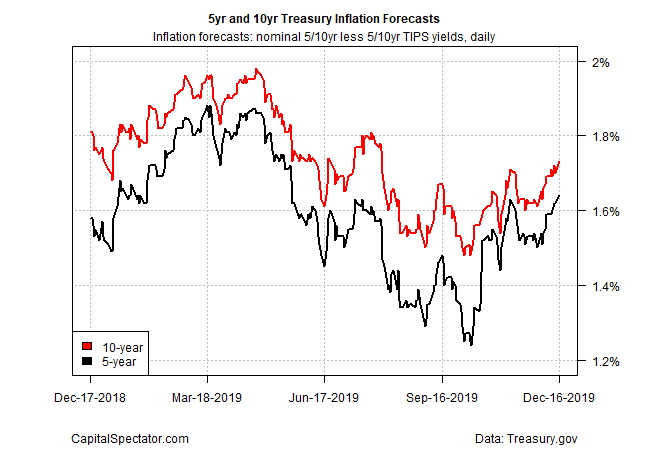

Consider the market’s inflation outlook based on the yield spread for the nominal 5-year Treasury less its inflation-indexed counterpart. This gap rose to 1.64% yesterday (Dec. 16), a seven-month high, based on daily data published by Treasury.gov. A similar reversal in the trend is conspicuous for the 10-year spread.

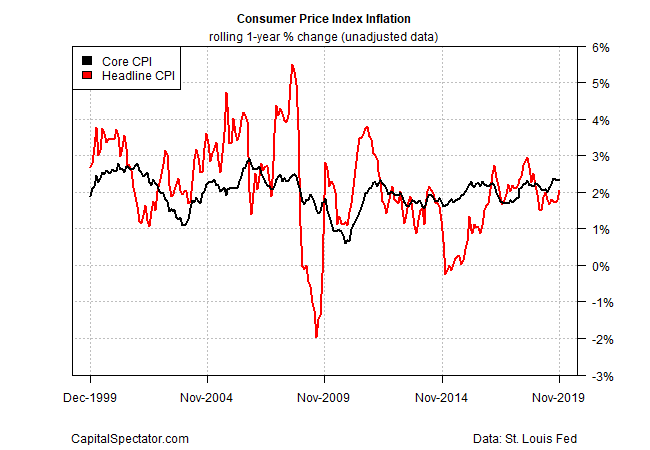

For now, it’s reasonable to see the rise in inflation estimates as mostly corrections from recent lows that arguably went overboard in pricing in high odds of an extended disinflationary run. At one point a few months back, the market’s 5-year inflation forecast looked set to slip to as low as 1.2%. The market is rethinking such a subdued future for the pricing trend, in part because the hard numbers on inflation have firmed up lately. Core consumer inflation is running at roughly 2% on an annual basis through November and headline CPI is even higher.

Despite the latest upgrades in the Treasury’s inflation outlook, there’s a long way to go before monetary policy will tighten. Last week Federal Reserve Chairman Jerome Powell said he wants to see a considerably stronger inflation trend before raising interest rates.

“In order to move rates up, I would want to see inflation that’s persistent and that’s significant,” Powell advised. “A significant move up in inflation that’s also persistent before raising rates to address inflation concerns: That’s my view.”

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

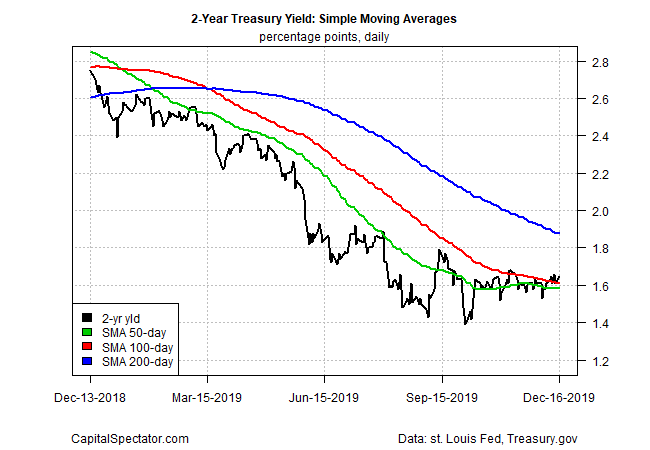

Using the 2-year Treasury yield for guidance (this rate is considered a proxy for policy expectations) suggests that the crowd still assumes that the central bank will keep policy steady for the foreseeable future. Until the 2-year rate shows a clear upside bias, the no-change outlook will likely to prevail.

Fed funds futures echo this peek into the future — this market is pricing in high odds that the Fed will keep its current 1.50%-to-1.75% range target rate steady for the first half of 2020, according to CME data.

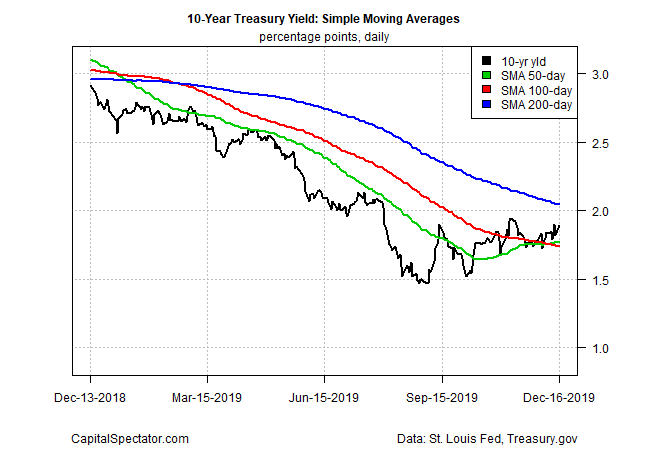

Nonetheless, the benchmark 10-year Treasury yield is hinting that rates may be set to trend higher in the weeks and months ahead. In contrast with the placid 2-year yield of late, the 10-year rate appears to be transitioning to an upside run. In particular, note that the 50-day moving average for the 10-year yield has recently ticked above the 200-day average for the first time since January. It’s premature to read too much into this still-nascent change, but if it continues and strengthens it may presage firmer reflationary signals in other parts of the Treasury curve. A similar shift for the 2-year maturity would be particularly significant.

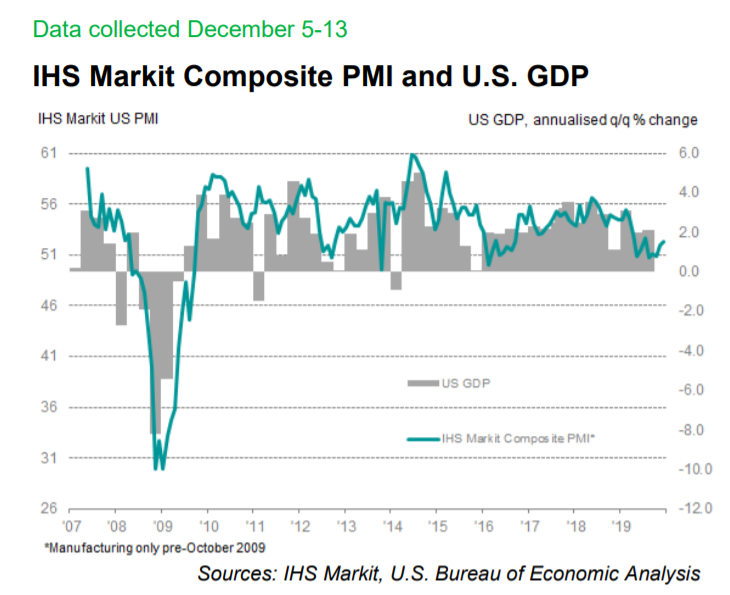

What might trigger a deeper and broader change in the market’s expectations for inflation? Perhaps it starts with recent clues that the US economy may be stabilizing after downshifting earlier in the year. PMI survey data for December shows that business activity growth bounced to a five-month high. “The surveys bring welcome signs of the economy continuing to regain growth momentum as 2019 draws to a close, with the outlook also brightening to fuel hopes of a strong start to 2020,” says Chris Williamson, chief business economist at IHS Markit.

The question is whether the hard data updates in the days and weeks ahead will confirm the apparent strengthening in the PMI survey data? The potential for an attitude adjustment starts with today’s November reports on housing starts and industrial production. Using consensus point forecasts as a guide via Econoday.com hints at the possibility of upbeat numbers on both fronts, based on the monthly comparisons. If correct, the news will give the reflation trade a fresh round of support.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Pingback: Is Treasury Market Flirting with Firmer Inflation Expectations? - TradingGods.net