Nothing lasts forever, as any student of the business cycle knows. But recognizing that the economy is dynamic, and constantly shape shifting, doesn’t make it any easier to spot trend changes in real time.

Most observers were late to the party in late-2022 and early 2023 in recognizing that last year’s slowdown in US economic activity was reversing. The macro trend in America certainly looked worrisome in the final months of 2022. But there were early hints that change was brewing.

In early November, CapitalSpectator.com noted that a pair of propriety US business cycle indicators were showing signs of stabilizing and looked set to “stay moderately positive in the immediate future.” It wasn’t fully clear at the time, and CapitalSpectator.com didn’t fully buy into the idea until late-spring 2023. But history now shows that November ended up as a turning point that would evolve into the “resilience” diagnosis for US economic activity in 2023 – resilience that continues, at least for the moment.

And yet the clues are adding up that the resilience may be peaking. To be clear: the odds that an NBER-defined recession has started or is imminent remains a low-probability risk, based on reviewing a wide number of economic and financial-markets indicators. The median nowcast for US GDP in Q3, for instance, continues to reflect moderate growth. But the tide may be in the early stages of peaking/turning, again, albeit modestly, like a thief in the night.

It’s easy to cherry pick a few indicators to make this point, such as the ongoing slide in job openings, which fell in June to the lowest level since March 2021. A more compelling clue is the ongoing but-still gradual decline in the year-over-year growth of nonfarm payrolls, which eased to a 2.2% through July. That’s still a healthy rise, but as each month posts a softer advance, the tipping point for the labor market at some point in the future draws ever closer and clearer.

The possibility of interest rates staying elevated, or perhaps going higher, isn’t helping. Last week Federal Reserve Chairman Powell said: “Although inflation has moved down from its peak — a welcome development — it remains too high.” He added that “We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.”

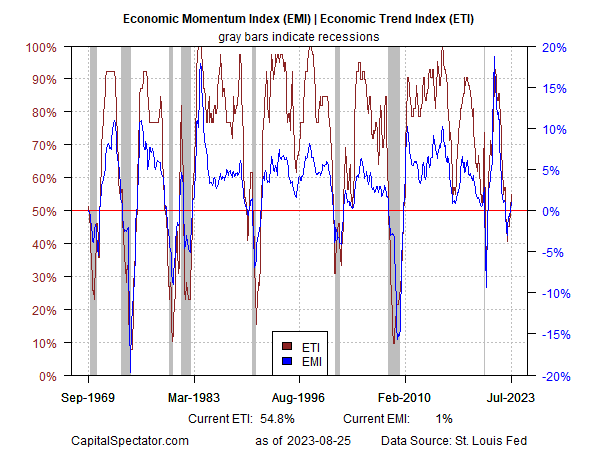

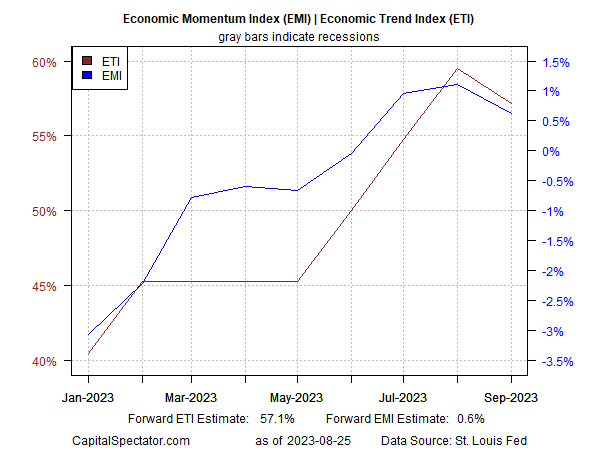

Talk is cheap and your editor prefers to focus on the data, particularly a broad, carefully diversified measure of US economic activity. That includes the Economic Trend Index (ETI) and Economic Momentum Index (EMI) that are part of the core analytics for weekly updates of The US Business Cycle Risk Report. As noted in this week’s edition for subscribers, the forward estimates for ETI and EMI posted modest downturns for September – the first declines vs. the previous month recorded this year.

For context, let’s start with the historical view of ETI and EMI. With the benefit of hindsight, the US economic rebound that started in late-2022 is clear and remains intact through July.

The challenge, as always, is modeling current conditions and the very-near-term future. (As a digression, the popular art of trying to forecast economic conditions more than a month or two ahead becomes increasingly pointless/hopeless the further out one looks, but I digress). A relatively methodology developed for The US Business Cycle Risk Report is using an ARIMA model to project each of the 14 indicators in ETI and EMI into the immediate future. This approach has proven valuable for quantitatively guesstimating the aggregated data points for ETI and EMI over the next 1-2 months. On that basis, it appears that the US economic resilience for 2023 may be peaking.

To be fair, it’s premature to take this apparent shift as definitive. Incoming data over the next several weeks may confirm or reject the preliminary trend change. It’s also possible that the moderate growth for the US economy will continue for some period of time, rather than accelerate or decelerate.

Meantime, I’m on peak watch for the US. It could be a false warning, but it’s too soon to tell. While we’re monitoring the numbers in the days and weeks ahead, it’s useful to remember that it’s all too easy to assume that recent economic activity is the best estimate of near-term future activity. That’s true most of the time… until it isn’t.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report