Seven trading days don’t tell us much about price trends, but if we plead temporary insanity and restrict our view of performance to the 2019 calendar the numbers look encouraging. What can we do with this information? Not much, but as financial entertainment goes it’s amusing. Let’s throw caution to the wind and consider how some key markets are shaping up so far this year, if only as a brief distraction from the chaos unfolding in Washington and its shutdown soap opera.

Using exchanged-traded funds (ETFs) as our guide, let’s start with the US stock market. As of last night’s close (Jan. 10), the bulls are back in charge after last year’s pain. A broad measure of equities — SPDR S&P 500 ETF (SPY) — is up 3.6% so far in 2019 – the best start for a calendar year in 13 years.

Small-caps are running even hotter: iShares Core S&P Small Cap (IJR) is ahead 6.5% year to date.

In fact, if you slice and dice the US equity market with a factor lens, the rally extends to all the usual suspects. Small-cap value is in the lead via iShares S&P Small-Cap 600 Value ETF (IJS), which is posting a solid 7.4% gain so far this year.

Foreign stocks are running hot, too, so far in 2019. Vanguard FTSE Emerging Markets (VWO) is up 5.1% year to date and Vanguard FTSE Developed Markets (VEA) is in close pursuit with a 4.9% increase in the new year through yesterday’s close.

Real estate is trending higher as well. Vanguard REIT (VNQ) has added 4.1% and its foreign counterpart – Vanguard Global ex-US Real Estate (VNQI) – is up a bit more via a 4.3% advance for 2019.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Even broadly defined commodities, which were hammered in 2018, are enjoying a rebound so far this year: iShares S&P GSCI Commodity-Indexed Trust (GSG) is up a strong 7.7%.

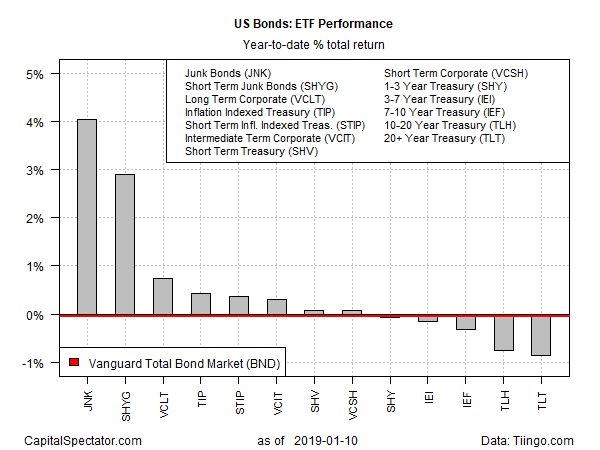

US bonds, by contrast, are a mixed bag. Junk bonds are soaring, led by SPDR Bloomberg Barclays High Yield Bond (JNK), which is up 4.1% year to date. But there’s plenty of red ink on the US fixed-income playing field so far in 2019. The biggest loser: long-term Treasuries via iShares 20+ Year Treasury Bond (TLT), which has lost 0.9%. The investment-grade benchmark — Vanguard Total Bond Market (BND) is fractionally under water for 2019 with a 0.1% loss.

Rounding out our review of 2019’s market results so far: let’s note that there’s an upside bias in foreign government bonds. SPDR Bloomberg Barclays International Treasury Bond (BWX) is up 0.9% while VanEck Vectors JP Morgan Emerging Market Local Bond (EMLC) has added 2.7% since last year’s close.

It’s tempting to see the generally upbeat results as a sign that all’s well. But a quick scan of the headlines reminds that there’s no shortage of risk factors threatening to create trouble for the rest of the year. From the partial US government shutdown to concerns that global growth is slowing to Mideast tensions and Brexit coming to a head, the markets have a deep well of raw material to draw on for climbing a wall of worry in the weeks and months ahead.

So far, however, the crowd is willing to revive animal spirits after a disappointing 2018. Nothing wrong with that. But given that it’s only Jan. 11, it’s premature to read too much into the year-to-date numbers. Meanwhile, one day at a time. It’s been a good year so far!

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Pingback: Based on First Seven Trading Days, 2019 Looks Promising - TradingGods.net