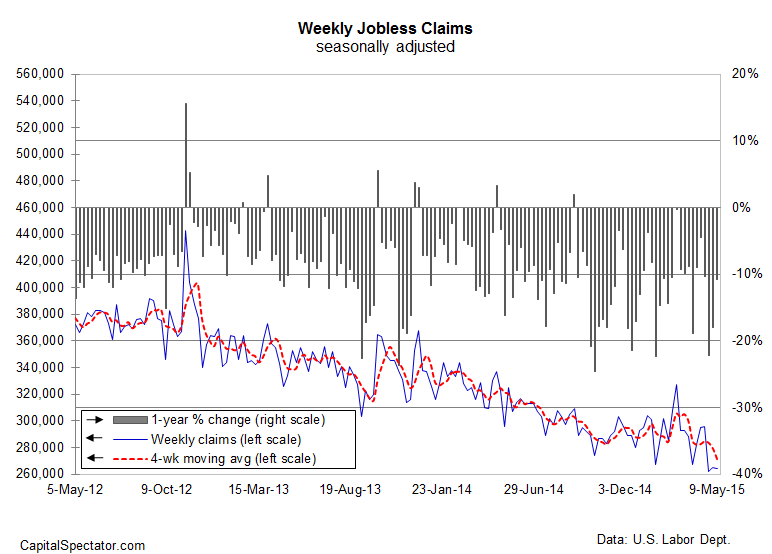

US growth ground to nearly a halt in the first quarter, but jobless claims continue to anticipate a solid pace of growth going forward. New filings for unemployment ticked lower by 1,000 last week to a seasonally adjusted 264,000, which is close to a 15-year low. The four-week average for claims, which is considered a more reliable measure of this volatile leading indicator, actually touched a new 15-year low last week. The downward bias suggests that the economy’s recent sluggish behavior will soon give way to a stronger run of growth.

“The signs are widespread and clear that labor markets are tightening noticeably,” Stephen Stanley, chief economist for Amherst Pierpont Securities, advised in a research note. Exhibit A for such thinking is the sliding trend in jobless claims.

Yet several other macro indicators suggest otherwise, including this week’s April report on retail sales. Consumer spending was flat last month as the year-over-year gain decelerated to a weak 0.9%–the slowest in nearly six years. Nonfarm payrolls in April bounced back after a disappointing gain in March, although the Federal Reserve’s Labor Market Conditions Index hasn’t joined the party and instead dipped in April, moving closer to a 3-Year low.

The outlook would darken considerably if jobless claims were persistently rising, but that’s not happening and yesterday’s release implies that the bullish momentum will persist. But if there’s a case for a second-quarter snapback in the US economy, it’s not showing up in the Atlanta Fed’s Q2 estimate for GDP. The bank this week pared its GDPNow forecast for the current quarter to a weak 0.7% gain. That’s fractionally up from Q1’s stall-speed increase of 0.2%. But if the Q2 prediction is accurate, the US economy is on track for its weakest stretch of back-to-back GDP reports in nearly six years.

Macroeconomic Advisers yesterday added to the recent batch of gloomy numbers by advising that its monthly estimate of GDP for March retreated by 1%, the most since Dec. 2008, when the Great Recession was raging. But don’t read too much into the stumble. “Because the decline in monthly GDP was driven by a surge in imports that was probably unrelated to current production, we are suspicious of it and believe it overstates the underlying weakness in the economy,” the firm explained via The Wall Street Journal.

The upbeat trend in jobless claims certainly leads the charge for optimism. The question is whether the incoming data will play along with the case for managing expectations higher after a dismal Q1?

The process of revising one’s outlook continues with today’s update on industrial production for April, due later this morning. The crowd, however, is anticipating that output was flat last month, based on Econoday.com’s consensus forecast. That’s an improvement over March’s steep 0.6% slide, but no change is hardly the foundation on which sentiment revivals are built.

That leaves the encouraging numbers on jobless claims and payrolls in April as the primary sources for thinking positively. The question is whether we’ll soon see a convincing degree of corroboration from other corners of the economy?