* Putin ‘planning for long war’ in Ukraine, predicts NATO chief

* US border cities prepare for expected migrant surge

* Tech firms focus on heading off tougher regulation

* Morgan Stanley analyst: drop in US corporate profits could rival 2008 era

* Goldman Sachs planning deep job cuts as it faces sharp business downturn

* US Senate banking chair considers banning crypto

* Germany business climate sentiment improves for third month in December

* Fed officials reaffirm plan to extend hawkish policy to tame inflation

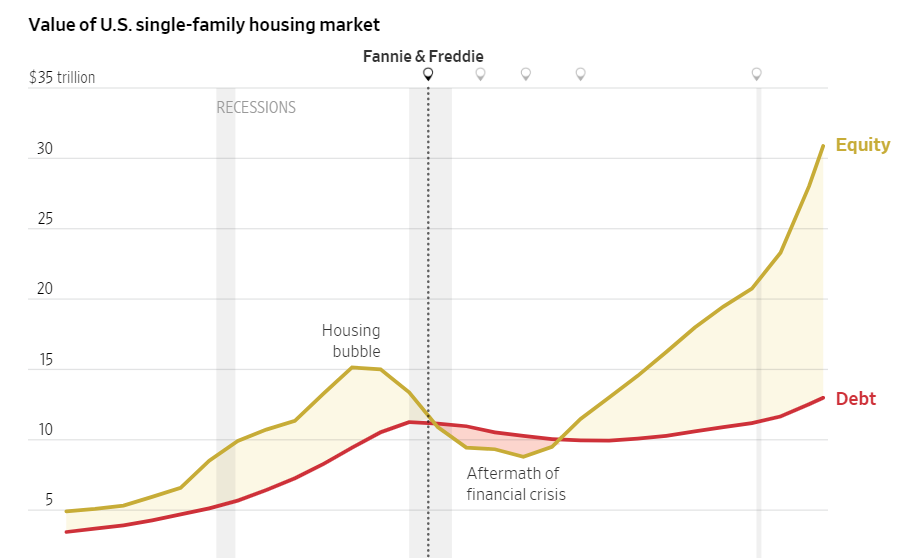

* The housing market appears relatively insulated from the downturn this time:

Central banks may be more comfortable with over-tightening, says Seth Carpenter, global chief economist at Morgan Stanley. “For central bankers, they really do have the responsibility of macroeconomic stability,” he says. “So I think they would rather be wrong by talking tough and saying that they’re ready to keep raising rates more and then happily find out later that they didn’t have to do more, rather than telling the world that they’re done and then go, ‘Oops, we have to do more.’”

Larry Summers thinks the start of recession has been pushed forward. “We are in better shape than I thought we were, and I think those are good numbers,” the former Treasury Secretary tells Bloomberg TV, referring to the softer-than-expected inflation data for November. As a result, the recession forecast “does look like it’s pushed back a bit in time.” He added: “I’ve been gratified to see the ways in which the Fed has caught up” in battling inflation by rapidly, substantially tightening monetary policy.

Will the Fed raise rates more than its expect? Maybe, suggests NY Fed President John Williams. “We’re going to have to do what’s necessary” to lower inflation to the Fed’s 2% target, he says in an interview with Bloomberg on Friday. “We’re absolutely committed to get inflation back to our 2% goal, and we’re acting in that way.” Consumer inflation rose less than forecast in November, offering support for the peak-inflation view. But if the Fed is committed to taming inflation to its target, there’s still a long way to go.

Cam Harvey, the “godfather” of the yield curve signal, says an inverted spread won’t be an accurate predictor of recession this time. “Do I expect a recession? No,” he tells Insider, citing three reasons, including excess demand for labor. The other two: yield curve is inverted on a nominal basis, but not on a real basis. The third: everyone expects recession because yield curve is inverted, which changes people’s behavior. “Given that people are more cautious, they actually provide themselves — and companies also — that when the economy does turn down, they’re somewhat insulated because they’re prepared. They’ve exercised risk management. And that enables the economy to have a so-called soft landing.”