This week’s initial peek at the March economic profile for the US via Markit’s survey data for manufacturing delivered upbeat news, which takes some of the edge off for expecting trouble. Later today we’ll see the equivalent for the services sector. Economists via Econoday.com’s consensus forecast are anticipating that the PMI Services Index will hold on to recent gains, in which case we’ll have a new clue for expecting brisk growth for this corner of the economy. But while the tail-end of the first-quarter is showing mild signs of revival, the outlook for Q1 GDP continues to stumble.

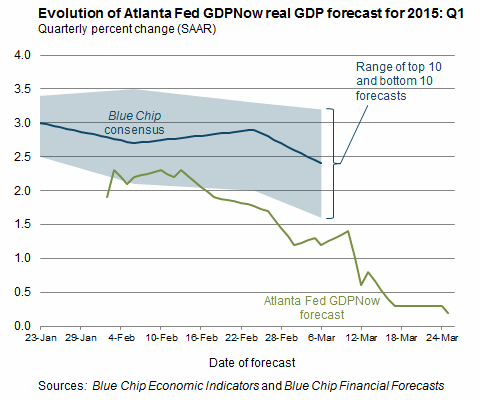

The case for managing expectations down starts with the latest GDPNow estimate from the Atlanta Fed. Yesterday’s update trimmed the outlook for first-quarter GDP growth to a thin 0.2%, down from the previous estimate of 0.3%. The new revision reflects yesterday’s disappointing news on durable goods orders for February.

Wall Street is paring Q1 GDP forecasts as well. CNBC reports that its average of Wall Street tracking estimates for growth in this year’s first quarter fell to 1.8%–the lowest forecast to date for Q1 projections via CNBC’s data set. Compared with the Atlanta Fed model’s outlook for something close to stagnation, however, a 1.8% advance looks relatively encouraging.

In any case, the consensus outlook now expects that first quarter growth will decelerate from the 2.2% rise in last year’s fourth quarter. The only question is by how much? The answer arrives in the “advance” estimate for Q1 GDP, which is scheduled for release on April 29.

One source of the softer estimates is linked to the recent strength in the US dollar. “We’re definitely seeing the impact from the stronger dollar — it’s evident in manufacturing surveys and production data,” Chris Low, chief economist at FTN, tells Bloomberg.

In the wake of the softer numbers, it’s reasonable to wonder: What’s the fallout for the labor market? Growth in payrolls has been robust, at least through the February data. Will the March update that’s due next week tell us otherwise?

It’s prudent to expect that the pace of growth for payrolls will decelerate in March. The recent rise in initial jobless claims hints at the possibility. New filings for unemployment benefits have increased recently, reaching 325,000 (seasonally adjusted) for the final week of February—the highest since last May. Claims have since pulled back, dipping below the 300,000 mark in the first half of March. Nonetheless, this leading indicator seems to be telling us that the rate of growth for job creation has slowed a bit.

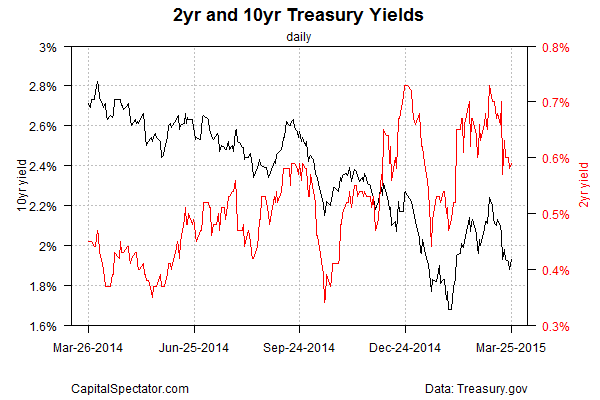

Mr. Market’s on board with lowering expectations, if only slightly. Treasury yields are falling, again. Although the Fed has been signaling that it’s inching closer to raising interest rates later this year, the bond market is increasingly skeptical. The yield on the benchmark 10-year Treasury has been trending lower since last week’s FOMC meeting. Ditto for the 2-year yield, which is considered to be the most sensitive spot on the yield curve for rate expectations.

It comes down to one question: Has the acceleration in growth fizzled? The case for expecting a moderate expansion is still intact, but the odds that we’ll see a stronger run of economic activity is looking shaky… again.