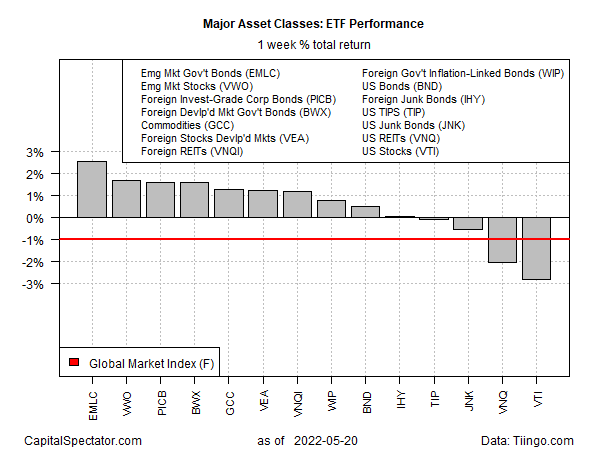

After weeks of widespread losses, markets around the world were mostly higher for the trading week through Friday, May 20, based on a set of ETFs. The main exceptions: stocks and real estate investment trusts in the US, which posted substantial weekly declines.

The strongest gain for the major asset classes last week: government bonds in emerging markets. After six straight weeks of loss, VanEck JP Morgan EM Local Currency Bond (EMLC) rose sharply, gaining 2.6%. Despite the upside reversal, it’s not obvious that the fund’s bearish trend has run its course, based on a price trend that still looks set for more downside risk.

Stocks in emerging markets were last week’s second-strongest gainer. Here, too, after six weeks of loss, Vanguard Emerging Markets Stock Index Fund (VWO) revived. But the 1.7% rise still looks like noise in an ongoing correction.

Emerging economies are headed for “tough terrain” in the near term because of blowback from the Russia-Ukraine war, predicts Atsi Sheth, global head of strategy and research for Moody’s Investors Service via Reuters, which reports: the Moody’s ratings agency “forecasts in a report that nearly 30% of rated non-financial companies in emerging markets would face ‘heightened credit risks’ in a worst-case scenario in which Russia’s invasion of Ukraine triggers a global recession and liquidity squeeze, including a suspension of energy trade between Europe and Russia.”

US stocks certainly endured rough terrain last week – again. Vanguard Total US Stock Market (VTI) shed 2.8% last week despite a heroic rally late in Friday’s session. The decline marks the seventh consecutive week of red ink for VTI.

US real estate fell nearly as much: Vanguard US Real Estate (VNQ) tumbled 2.0%, the fourth straight weekly slide.

The Global Market Index (GMI.F) fell for a seventh week, shedding 1.0%. This unmanaged benchmark, maintained by CapitalSpectator.com, holds all the major asset classes (except cash) in market-value weights via ETFs and represents a useful benchmark for portfolio strategies overall.

For the one-year return, broadly defined commodities (GCC) are the only slice of the major asset classes with a positive change – by a huge margin: GCC is up nearly 30% over the past 12 months.

The biggest one-year loss for the major asset classes: foreign corporate bonds (PICB), which are down roughly 20%.

GMI.F’s one-year loss: -10.2%.

Drawdowns for the major asset classes range from moderate – roughly -7% for inflation-indexed Treasuries (TIP) – to steep: nearly -26% for emerging markets government bonds (EMLC).

GMI.F’s current drawdown: -16.6%.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report