Retail sales unexpectedly fell 0.5% last month, the Census Bureau reports. Economists had generally predicted an increase for the month. In contrast, the revised numbers now show that June’s retreat was the third monthly loss in a row—the first trio of consecutive decreases since 2008. Not an encouraging sign, but not a smoking gun either.

The standard caveat applies, namely, monthly data is volatile and not necessarily indicative of the broader trend. Then again, it’s not often that volatility on the downside persists for three months running if the economy has a head of steam.

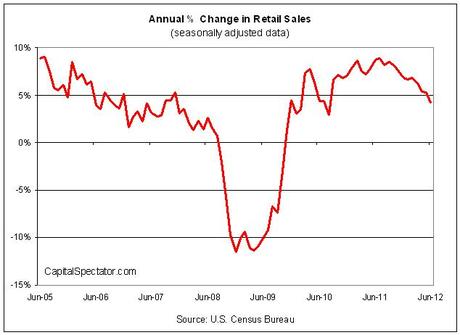

For a clearer look at the trend, let’s consider the year-over-year percentage change. The good news is that retail sales are still growing at a healthy pace on this score. The bad news is that the deceleration in the annual rate of growth rolls on, posting a 4% rise for the year through last month—the slowest increase since August 2010.

Is this a sign that a recession has started? Possibly, but the jury’s still out until we have a broader reading on the June data. There’s still a case for making a distinction between forecasting and diagnosing the trend based on the numbers in hand. We’ll know more in the days and weeks ahead.

What we’ve seen so far, however, has been a mixed bag, at best. The ISM Manufacturing report is warning of economic trouble. So too is the employment report for June, although the annual pace of private-sector job growth continues to hold up in moderately positive territory and initial jobless claims have yet to take a sharp turn upward. Nonetheless, it’s hard to dismiss the possibility that the cycle has turned.

If we have slipped over the edge, we’ll soon see a number of convincing signs of the change. For example, the June update of the Chicago Fed National Activity Index (scheduled for release on July 23) will tell us if the May weakness in this benchmark deteriorated further. Meantime, I’ll be updating my 15-indicator reading on the economy for additional clues on where we stand as of last month as the numbers come in.

For the moment, it’s getting easier to see darkness approaching. It may still be a head fake, but that’s a harder argument to make today. “Evidence is increasingly clear that the U.S. economy is slowing,” says Jim Baird, an investment strategist at Plante Moran Financial Advisors.

“People are just pulling back, and you’re not likely to see a significant pickup from here,” notes Michael Carey, chief economist for North America at Credit Agricole CIB. “This was certainly a slowdown from the first quarter.”

The next big clue: industrial production for June, which will be released tomorrow. The consensus forecast among economists sees a 0.3% rise for last month, according to Briefing.com. Suffice to say, the crowd’s just about out of patience for another round of negative surprises.