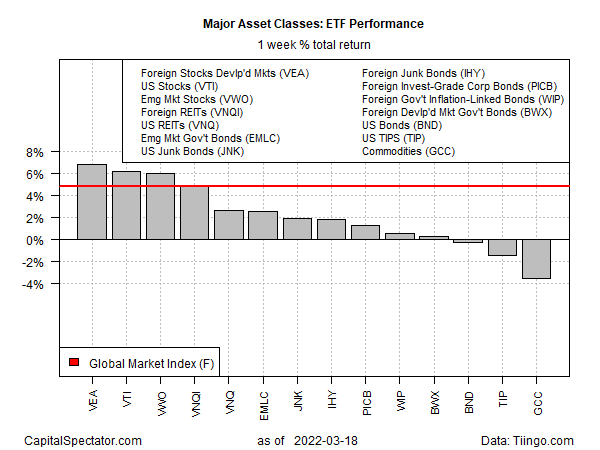

Most markets around the world staged a strong rebound last week, led by stocks in foreign developed markets ex-US, as of Friday’s close (Mar.18). The main exceptions: US bonds and commodities, which posted the only setbacks for the major asset classes last week, based on a set of ETFs.

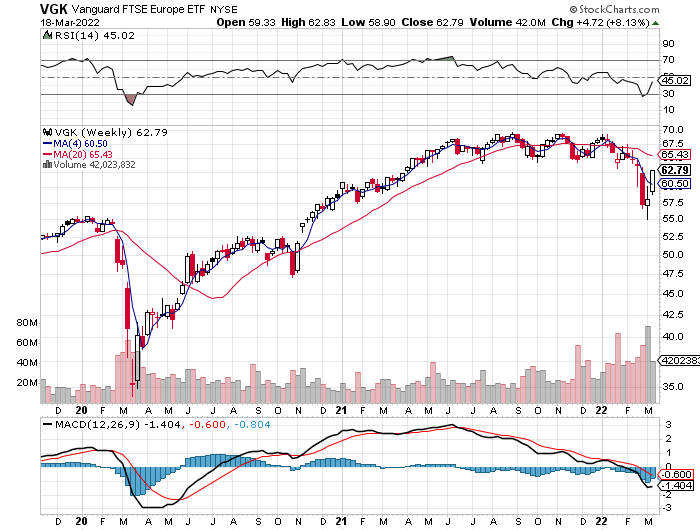

Vanguard FTSE Developed Markets (VEA) surged 6.8%, the ETF’s. A key driver of VEA’s strong rally last week: a sharp gain for shares in Europe.

The return of strength to European shares strikes some observers as odd and perhaps misguided. The Continent’s economy, after all, is still vulnerable to the war in Ukraine that’s still raging on Europe’s eastern border. By some accounts, the opportunity for buying shares at relatively inexpensive multiples and the possibility that the war’s end-game may be near has inspired a recovery in risk-on sentiment, at least for now.

“We were seeing panic outflows but now investors are having second thoughts,” says Bastien Drut, chief thematic macro strategist at CPR Asset Management in Paris. “The markets are starting to trade on fundamentals again.”

Unfortunately, the best-case outlook at the moment is stalemate. “But we should note it’s a bloody stalemate,” says ex-CIA Director David Petraeus, a retired general who served in Iraq and Afghanistan. “Also, arguably, it’s a battle of attrition.”

It’s unclear if that scenario will continue to foster a tailwind for European shares (or stocks elsewhere in the world), but for now it’s arguably the only realistic assessment of what lies ahead for the immediate future.

Stocks generally posted gains last week, including solid advances in the US and emerging markets. The main losers: US investment-grade bonds and commodities. WisdomTree Commodity (GCC) tumbled for a second straight week, losing 3.5%. Despite the setback, GCC remains sharply higher so far in 2022 with a 20.5% year-to-date gain.

The Global Market Index (GMI.F) rebounded 4.8% last week, posting its first weekly gain in the past three. This unmanaged benchmark, maintained by CapitalSpectator.com, holds all the major asset classes (except cash) in market-value weights via ETF proxies.

For the one-year-return profile, a broad measure of commodities continue to lead the major asset classes by a wide margin. WisdomTree Commodity (GCC) is up 37.3% over the 12-month window through Friday’s close.

The weakest one-year performers are essentially tied with losses of nearly 11% via foreign corporate bonds (PICB) and foreign high-yield bonds (IHY).

GMI.F is posting a moderate 4.0% gain over the trailing one-year window.

Profiling the major asset classes through a drawdown lens continues to show that most markets are posting deeper peak-to-trough declines than the current 7.0% decline for GMI.F.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report