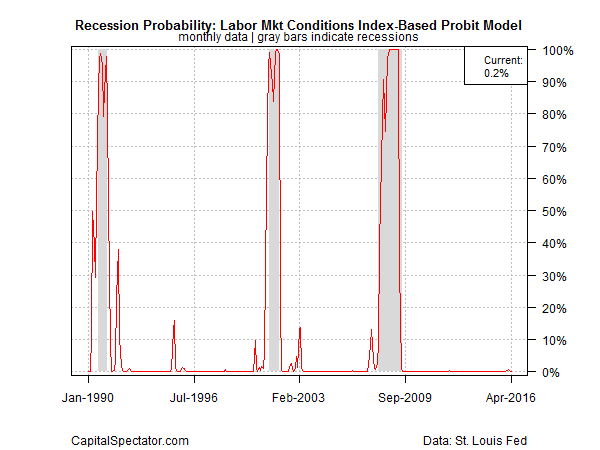

Yesterday’s April update of the Federal Reserve’s Labor Market Conditions Index (LMCI) points to a sluggish rebound for the US economy in the second quarter after flirting with stall-speed GDP growth in Q1. Although LMCI ticked up last month, this multi-factor benchmark posted its fourth consecutive negative reading—the longest stretch of below-zero values since the last recession. That’s not encouraging, but for the moment the main risk is slow growth rather than a new downturn that triggers an NBER-defined slide into recession.

Let’s run LMCI’s history through a probit model that quantifies the index’s relationship with NBER’s business-cycle history for the US. By this standard, LMCI’s implied odds that a new recession started in April remains virtually nil.

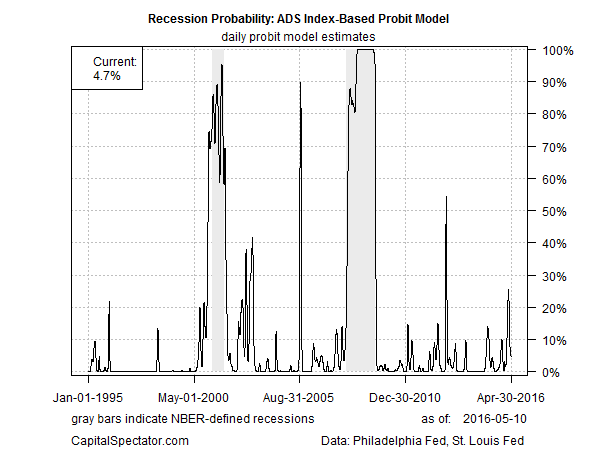

That’s also the message from the vantage of other data sets, including the Philadelphia’s Fed’s ADS Index, which tracks the business cycle via several indicators. Analyzing the ADS data via a probit model also points to a low probability at the moment that April will eventually mark the beginning of an NBER-defined recession.

The caveat is that April’s macro profile is incomplete and subject to revision. But based on the published numbers so far, the odds are low that the US economy was contracting during the first month of the second quarter.

Unfortunately, avoiding a formal recession doesn’t preclude a continuation of slow growth. The Atlanta Fed’s current GDP growth forecast for Q2 (as of May 4) is a weak 1.7% (seasonally adjusted annual rate). That’s an improvement over Q1’s virtually flat 0.5% rise, but both numbers constitute an expansion that’s about as slow as possible without dipping into recession territory.

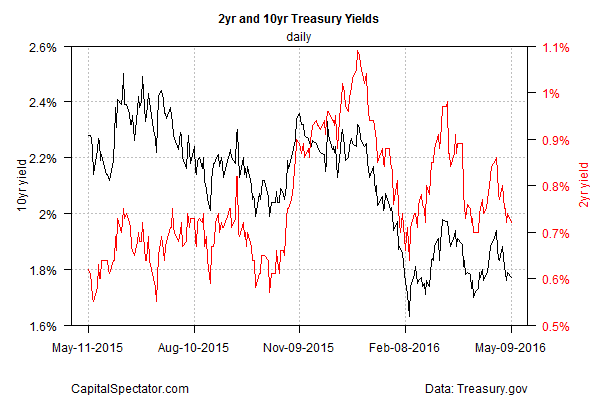

Given the current climate, it’s no surprise to see that Treasury yields are drifting lower… again. The benchmark 10-year Treasury rate, for instance, eased to 1.77% yesterday (May 9), based on daily data via Treasury.gov. Yesterday’s dip leaves the benchmark rate near this year’s low of 1.63% (in early Feb.), when macro expectations were considerably darker.

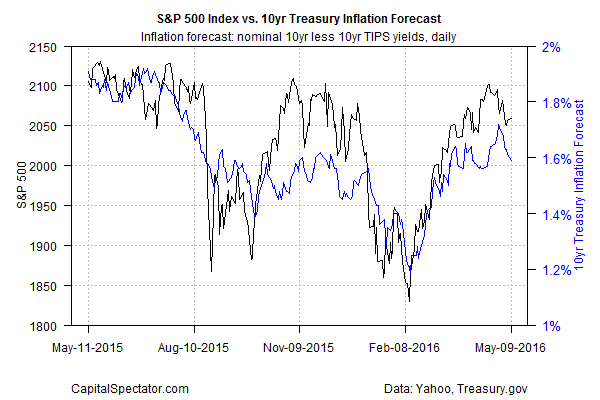

Note, too, that the Treasury market’s implied inflation forecast via 10-year nominal and inflation-indexed maturities is slipping again. The slide, if it continues, suggests that the US stock market (S&P 500) remains vulnerable to further selling. As the next chart below reminds, US equity prices are still tightly correlated with changes in inflation expectations, which makes sense at a time when slow growth and disinflation remain key concerns.

In sum, the available numbers look convincing about two points. One: the US probably didn’t slip into a recession last month. Two, the rebound in Q2 is off to a weak start.

On a brighter note, economists are expecting stronger growth in Friday’s update of retail spending for April. Econoday.com’s consensus forecast sees a 0.9% surge in spending vs. the previous month—the strongest monthly increase in nearly a year and a healthy rebound after March’s modest retreat. If the forecast holds, the news will revive expectations that economic growth may be set to accelerate after all. At the same time, expecting a sustained rebound in consumer spending may be expecting too much if employment growth stays weak.

Pingback: Sluggish Rebound for US Economy - TradingGods.net