Shares of small companies and value stocks have had a tough time keeping up with the broad market in recent years, and the headwind for these risk factors is still blowing so far in 2024.

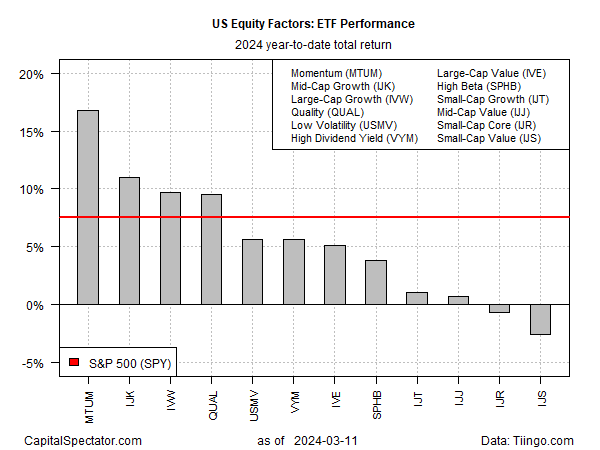

By contrast, the momentum factor (MTUM) has surged nearly 17% so far this year, dramatically outperforming its counterparts, based on a set of US equity factor ETFs through Monday’s close (Mar. 11). At the opposite extreme: the small-cap value factor (IJS), which is underwater by 2.6% year to date.

To be fair, small-cap growth (IJT) is holding on to a modest 1.0% gain in 2024. But this pales next to broad market’s 7.6% rally via SPDR S&P 500 ETF (SPY).

Meanwhile, mid- and large-cap growth, along with quality (IJK, IVW, QUAL, respectively), are neck and neck for second-place this year.

The strength of the broad market’s rally has triggered warnings from some analysts that the market has risen too far, too fast. But by some accounts the upside bias is encouraging. As the Financial Times reports today:

Goldman Sachs and UBS have upgraded their year-end forecasts for the S&P 500 this year, and this month Bank of America raised its year-end prediction to 5,400 — about 5 per cent above the index’s current levels.

“It’s like a reset of the risk cycle,” said Evan Brown, a portfolio manager and head of multi-asset strategy at UBS Asset Management. “Everyone’s been anticipating a recession for a long time and it hasn’t materialized.” He described the growing enthusiasm for stocks as a release of pent-up risk appetite.

But some observers, with an eye on the Federal Reserve, worry that a policy mistake is a growing risk factor. Mohamed El-Erian, an economist and advisor to Allianz advisor, writes in a Bloomberg column that a Fed “held hostage” by so-called data dependency “is asking for trouble.”

Don’t get me wrong; high-frequency inputs are important in any assessment of economic conditions and policy responses.

In today’s economy, an excessive focus on the numbers tips the balance of risks toward keeping interest rates too restrictive for too long, unduly increasing the probability of output loss, higher unemployment and financial instability.

Yet there are signs that the rally is broadening, which inspires some observers to see a bullish future. The Wall Street Journal reports: “Strong US growth is prompting investors to scoop up a broader set of stocks, rather than just the handful of giant technology companies that drove indexes to record heights.”

Joseph Amato, chief investment officer of Neuberger Berman, advises that the macro trend is now your friend. “With inflation coming down and the Fed no longer fighting you, it’s just a better long-term case for risky assets.”

The next stress test of that view arrives later this morning, with the release of consumer inflation data for February.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno