The US stock market has stabilized in recent weeks, but the downside bias still appears intact. Several risk factors support this outlook, including a weak technical profile; high inflation that will likely convince the Federal Reserve to continue raising interest rates; a rising if not yet decisive threat of a US recession; and the ongoing uncertainty/blowback for the global economy due to war in Ukraine.

It doesn’t help that today’s news from China paints a worrisome picture of the world’s second-largest economy, which contracted in the second-quarter, based on GDP. The decline marks the weakest performance for the economy in two years. “China is no position to be the global engine of growth right now, and the long-term fundamentals point to much slower growth in the next decade,” says Kenneth Rogoff, a professor of economics at Harvard University and a former chief economist for the International Monetary Fund.

As for the current US equities profile, let’s start with a weekly chart of the S&P 500, which shows consolidation over the past month. Perhaps this is a sign that the correction this year has run it’s course (or is close to a trough). Only time will tell. But given the weak macro backdrop, the case for staying defensive/cautious on the near-term outlook still looks reasonable.

The ratio for a pair US equity ETFs that can be used as a proxy for estimating the trend in the market’s risk-on/risk-off sentiment evolution. Comparing the relative performance of the S&P SPDR (SPY) to iShares MSCI Minimum Volatility (USMV) indicates that market sentiment remains defensive (ratio is falling). When this ratio begins to stabilize and turn higher that shift will provide a possible early sign that the tide is starting to turn in favor of the bulls again. For the moment, however, that turning point doesn’t appear to be imminent.

The challenge for market analytics at the moment is deciding if the correction to date has run its course, or is close to a trough. By one measure, that’s a reasonable view, based on CapitalSpectator.com’s S&P 500 Sentiment Momentum Index (for details, see this summary). The index (cited in Z-scores) is posting one of its lowest readings since the pandemic initially triggered a sharp correction in the spring of 2020. That marks a relatively deep slide, although history suggests even deeper declines are possible. Using this metric as a guide suggests that odds look reasonable to play a near-term bounce in the market. Investors with a low risk tolerance, however, may want to stay defensive until there are more convincing signs that a sustained rebound is underway.

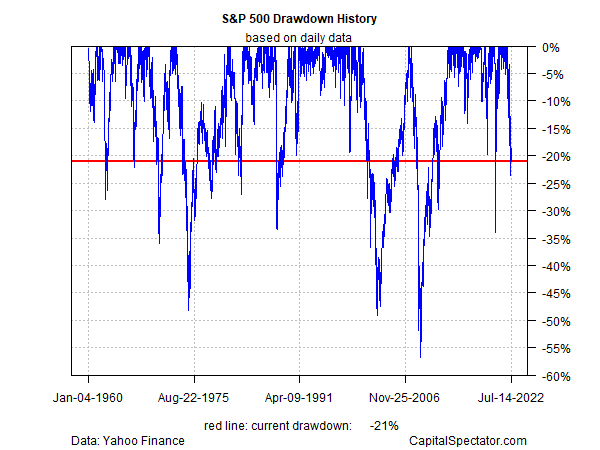

A similar profile turns up via drawdown for the S&P 500. The current peak-to-trough decline for the S&P 500 continues to hold below -20%, a mark widely used as a rule of thumb for defining a bear market. The market’s slide is nearly seven months old, a bit more than half as long as the 12-month average for bear markets since World War II, according to LPL Research. The average decline is -30%, which implies that further weakness from this point on wouldn’t be unusual.

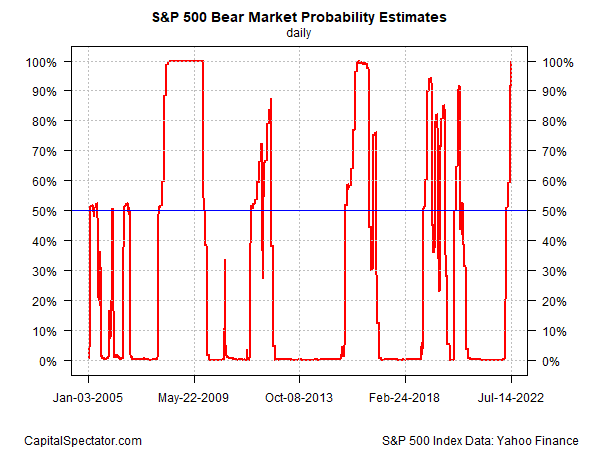

Unsurprisingly, a Hidden Markov model (HMM) continues to indicate that the S&P 500 has entered bear-market terrain. This indicator first hinted at a bear-market signal by rising above the 50% probability mark in early May. The latest reading is 99.9% (July 14). (For some background on how the analytics are calculated in the chart below, see this primer.)

Applying another econometric model to estimate so-called bubble risk shows that this indicator is still indicating that the market appears frothy, and therefore remains vulnerable to the downside. (See this 2014 post for some background on the methodology).

Finally, market valuation has declined recently, although it’s debatable if the S&P has returned to a level that’s considered reasonably valued, based on the CAPE ratio.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report