Morningstar recently tested the niche world of publicly traded tactical-allocation funds and found mediocre results at best. The Capital Spectator came to a similar conclusion a couple of months back in a mini-study of a handful of tactically minded ETFs. Let’s update the numbers and see if anything’s changed.

But first, a quick recap of Morningstar’s analysis, which reviews a broader sample of funds, including open-end products. For a benchmark, the study used Vanguard Balanced (VBINX), a simple non-tactical 60%/40% mix of stocks and bonds. The main takeaway: the tactical strategies fared poorly. Morningstar’s summary:

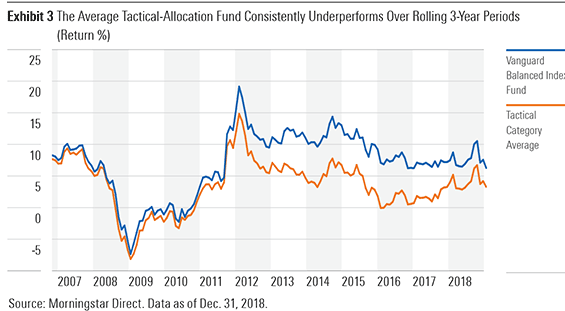

Over the past 15 years through December 2018, the average tactical-allocation fund returned 3.4 percentage points annually, lagging Vanguard Balanced Index by 3.2 percentage points per year with similar risk. This underperformance has been consistent, too. Vanguard Balance Index beat the tactical-allocation category average in every rolling three-year period during the trailing 12 years through December 2018.

Underperforming the benchmark might be tolerable if risk control was impressive, but that wasn’t the case either. According to the Morningstar report, “During the 15 years through December 2018, the average fund in the tactical-allocation category tended to lose 5% more than Vanguard Balanced Index in months that the Vanguard fund posted negative returns.”

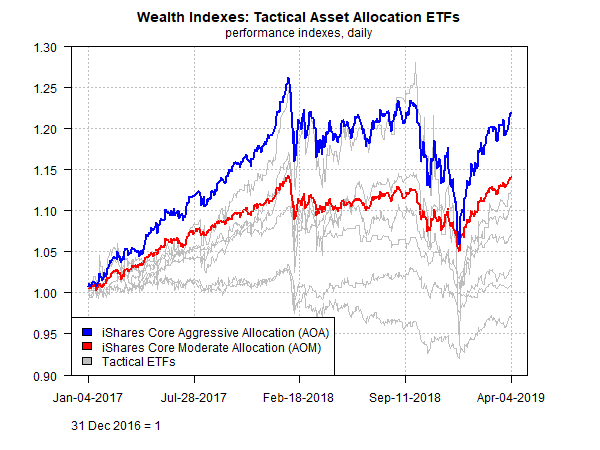

In February, The Capital Spectator came to a similar conclusion, based on crunching the numbers on six tactical asset allocation ETFs. Two months on, has anything changed? No. Comparing the half-dozen funds to a pair of plain-vanilla asset allocation ETFs — iShares Core Moderate Allocation (AOM) and iShares Core Aggressive Allocation (AOA) – reaffirms that the six strategies continue to fall short. Notably, the late-2018 correction and subsequent year-to-date 2019 rebound in markets has been especially rough on the tactical strategies practiced by the six ETFs.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

The chart below compares the six tactical funds with the two benchmark portfolios (red and blue lines), using a Dec. 31, 2016 start date. Why that date? Two of the funds were launched in 2016, which defines how far back we can analyze the group as a whole. The short sample should be taken with a grain of salt, but when viewed in context with the Morningstar results it’s clear that publicly traded tactical funds have faced headwinds, to put it mildly. (The six tactical ETFs remain anonymous for this analysis; interested readers can contact The Capital Spectator for funds’ identities.)

It’s striking that AOM and AOA outperformed all six tactical funds for the sample period. Ditto for reviewing the numbers through a risk-adjusted prism. Using Sharpe and Sortino ratios reveals that AOM and AOA generated stronger risk-adjusted performances. To be fair, two of the tactical funds posted lower maximum drawdowns, but compared with AOM the modestly lower peak-to-trough declines aren’t terribly impressive.

The lesson here is that designing and managing a tactical strategy that delivers encouraging results is challenging. That doesn’t mean it’s pointless to try. But the numbers above demonstrate that trying to beat a simple asset allocation strategy — either with higher return, lower risk or both – tends to be the exception rather than the rule.

As Morningstar concludes, “tactical investing is hard and most who try it fail. For most investors, the best bet is to stick to a suitable long-term asset allocation.”

To the extent you disagree, it’s a safe assumption that you won’t be using data for publicly traded funds to make your case.

Is Recession Risk Rising? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Thanks, James, for the interesting article and link to the Morningstar piece. The Morningstar author mentioned good results testing a strategy which varies stock allocation based on volatility, and I have seen interesting results testing similar strategies on PortfolioVisualizer.com with leveraged ETFs, like SSO. You could use a mix of leveraged and unleveraged funds based on your target exposure each period.

I think I own a couple of those underperforming tactical asset allocation ETFs. We haven’t had a good long bear market since the inception of GMOM and QMOM and the like, so maybe we need more patience to see if they lower drawdowns in the types of markets they were designed to excel in.

It’s probably a good idea to vary tactical strategies — by signal type (momentum, relative strength, valuation, volatility, etc.), by lookback period, trading frequency, etc. If beating the market was as easy as picking tactical ETF and seeing results in a couple of years, more of us would be doing it!

Also, check out the CAPE ETN — it’s a tactical sector allocation strategy rather than asset class allocation, but it does show that tactical strategies can work.