Last week I briefly reviewed the case for casting a wary eye on expecting the standard stock-bond asset allocation to fulfill its historical role as a risk-management tool. Let’s extend this thought experiment by comparing results for possible bond replacements in the classic 60/40 stock/bond portfolio.

As a quick refresher, a recent GMO research note argued rather persuasively that low yields on bonds create headwinds for fixed income as a strategy for smoothing out market volatility in portfolios when stocks take a beating.

“The recent fall in cash and bond yields for those developed countries that still had positive yields has left government bonds in a position where they cannot provide two of the basic investment services they have traditionally provided in portfolios – meaningful income and a hedge against an economic disaster,” writes Ben Inker, head of asset allocation at GMO.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Recent history offers support for his warning. During the coronavirus market crash in March, bond returns were negative in countries where yields were effectively at zero or lower.

A sign of things to come in US if yields continue to move closer to zero or below? Although no one can be sure if US bonds will lose their ability to offset equity market losses in portfolio in the years ahead, we can test how fixed-income alternatives perform in a traditional 60/40 portfolio. As an initial step, let’s review four bond replacements based on numbers since 2008.

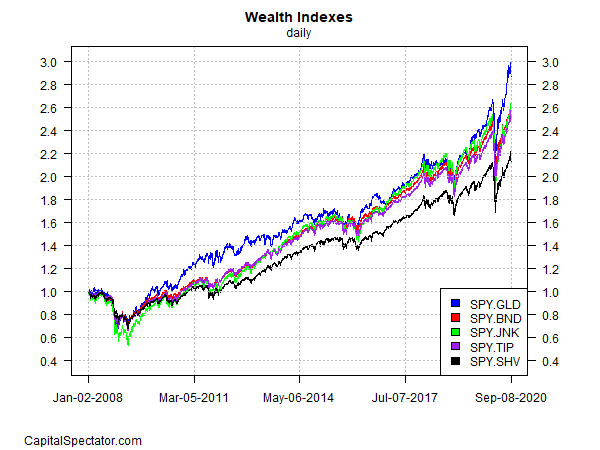

The baseline portfolio holds a 60% weight in SPDR S&P 500 (SPY) and 40% in Vanguard Total US Bond Market (BND). This portfolio is rebalanced to the target weights every Dec. 31. The alternative strategies are managed identically — except that the bond slice is replaced with one of four ETF substitutes representing gold (GLD), cash (SHV), inflation-indexed Treasuries (TIP) and junk bonds (JNK). These are far from the only possibilities, but it’s a useful starting point. Here’s how the numbers stack up:

For a visual summary, here are the results for investing $1 in each strategy on Dec. 31, 2007:

In raw performance terms, the stock/gold mix won the race with an 8.7% annualized total return – comfortably ahead of the baseline strategy’s 7.5%. The other three strategies either matched the baseline return or trailed it.

Looking at the results through a risk prism reminds that there are no perfect substitutes for the standard bond allocation. Using junk bonds, for example, offers the potential for significantly higher yields, but at a price of substantially higher risk for the portfolio. The maximum drawdown for the stocks/junk mix during 2008-2020 was a steep 46.9% decline—considerably deeper than the 32.2% peak-to-trough decline for the baseline portfolio.

The other three alternative strategies offer a comparable maximum drawdown to the baseline strategy but each comes with its own set of pros and cons.

“Investors will need to think more creatively than they have had to historically in order to get the services they used to get from bonds or to build a portfolio that doesn’t require those services in the first place,” Inker prdictes. “That task is by no means impossible, but in a world where historical performance is much less relevant for forward-looking expectations, it will require more thought and creativity than it once did.”

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report

Pingback: Comparing Results for Bond Replacements in 60/40 Stock/Bond Portfolio - TradingGods.net

Interesting idea, and well motivated; I do appreciate the general thrust of the article. However, if the issue truly follows from the GMO report that “low yields on bonds create headwinds for fixed income as a strategy for smoothing out market volatility”, then what one needs to examine is not sharpe ratio, vol and max drawdown, but _correlation coeficients_ . It is the asset class correlations that matter for overall portfolio volatility, if that is truly the issue. Looking at the past 10 years as a model for a “lower for longer” environment, correlations to the SPY are as follows: BND=-0.60; GLD=0.05; SHV=-0.40; TIP=-0.23; JNK=0.67. So, BND still provides the best diversification at a negative 0.60 correlation to SPY. JNK is the worst substitute from a correlation perspective.

But Ben inker and this article’s author also are concerned about providing “meaningful income” in a low rate world. This is a different issue but one critical for income-dependent investors. In this light, Inker and the author are right, replacing some portion of the bond portion of a 60/40 makes sense to seek higher returns/income, but it will be at the _expense_ of worse diversification than standard bonds can provide. Finding the trade-off will be the challenge.

Personally, I have allocated more of my “bond” portion to munis, preferreds and convertibles. Preferreds and convertibles have a correlation to stocks around 0,60, so a modest correlation, but far less of a diversifier than gov bonds; but the excess return over the past 10 years over gov bonds have, for me, justified the tradeoff.

My thanks to the author for highlighting the issue investors face in their portfolio allocation.

Miguel,

Yes, correlations are important, but keep in mind if the low/zero-yield thesis is correct, and bonds lose their diversification power, looking at historical correlations will be misleading.

–JP