Inflation has been trending lower this year, but the Federal Reserve still appears on track to hike rates again before the year is out.

Fed funds futures this morning are pricing in an 82% probability that the central bank will lift its target rate to a 1.25%-to-1.50% range from the current 1.0%-to-1.25%, based on CME data. A quarter-point rise would be a relatively trivial change. But with inflation holding well below the Fed’s 2% target lately, plans for another hike have become a controversial topic.

Yesterday’s release of minutes from the latest policy meeting highlights the Fed’s internal debate on how to interpret the soft inflation numbers.

On balance, participants continued to forecast that PCE price inflation would stabilize around the Committee’s 2 percent objective over the medium term. However, several noted that in preparing their projections for this meeting, they had taken on board the likelihood that convergence to the Committee’s symmetric 2 percent inflation objective might take somewhat longer than they anticipated earlier.

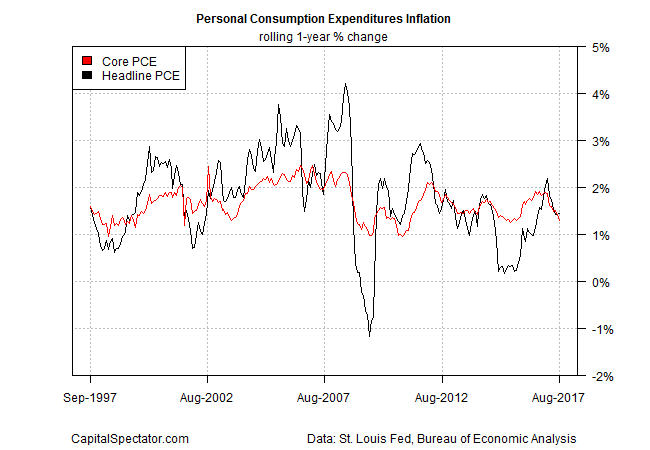

Recent history certainly leaves the doves with ammunition for promoting a go-slow approach to rate hikes. Core inflation based on personal consumption expenditures, which is on the Fed’s short list for key measure of pricing pressure, fell to a 1.3% year-over-year pace in August – the softest gain in a year-and-a-half.

But if the downside bias in core PCE is a reason for delaying rate hikes, at least one Fed official isn’t drinking that Kool-Aid. San Francisco Federal Reserve Bank President John Williams yesterday said he anticipates another round of tighter policy this year and three more hikes in 2018.

For analysts who argue that the economy is strong enough to warrant higher rates and inflation will soon heat up, Exhibit A is the recent increase in wage growth. The annual change for average hourly earnings for workers in the private sector ticked up to 2.9% in September – the highest since 2009. By some accounts, this is a sign that soft inflation is set to rebound in the months ahead.

Skeptics point out, however, that the stronger trend in wage increases may not be the hawkish inflation signal it appears to be. As CNN Money notes:

The jump in wages last month might be due to the fact that there were more than 100,000 jobs lost in low-wage jobs that government economists call the “food services and drinking places” industry and normal people call restaurants and bars.

The fast food sector isn’t known for paying its workers a lot of money — despite some recent minimum wage increases across the nation and moves by individual companies like McDonald’s (MCD) to boost hourly wages.

Nonetheless, the latest Fed minutes suggest that some central bankers are persuaded that firmer wage growth will soon raise inflation.

Many participants continued to believe that the cyclical pressures associated with a tightening labor market or an economy operating above its potential were likely to show through to higher inflation over the medium term. In addition, many judged that at least part of the softening in inflation this year was the result of idiosyncratic or one-time factors, and, thus, their effects were likely to fade over time.

The Treasury market is still taking a wait-and-see view on inflation, although the recent jump in the implied inflation forecast via the 10-year Notes hints that a change in sentiment may be brewing. The yield spread between the nominal 10-year Note and its inflation-indexed counterpart inched up to 1.89% yesterday (Oct. 12), the highest since May, based on daily data via Treasury.gov.

The crowd’s preference to estimate inflation at a sizable premium over the hard data reflected in core PCE could be noise. But a dovish outlook will face more headwinds if the market’s 10-year inflation forecast reaches 2.0%-plus.

Meantime, the Fed appears divided on how to proceed. As the minutes advised, “A few of these participants thought that no further increases in the federal funds rate were called for in the near term or that the upward trajectory of the federal funds rate might appropriately be quite shallow.”

Perhaps Friday’s hard data will help clarify the outlook. Based on Econoday.com’s consensus forecasts, the numbers are set to provide a round of support for the hawks. Headline consumer prices for September are projected to accelerate to a 2.3% year-over-year gain – the first print over 2.0% since April. Meanwhile, retail sales are expected to post a strong rebound, rising 1.8% in September vs. the previous month – the biggest monthly advance in more than a year.

If the predictions are correct, the case for assuming that “lowflation demon” will prevail may be due for an attitude adjustment.

Is not the main job of the Fed to prevent asset bubbles?

Pingback: Despite Low Inflation Fed Still On Track to Raise Rates Again - TradingGods.net