It’s no secret that global interest rates have been low in recent years, but a recent study by the Bank of England (BoE) finds that the decline exceeds records going back to the 13th century. Piecing together a new dataset, the research advises that the latest bond bull market that’s driven yields down is even more extraordinary than previously known.

“We establish for the first time a long-term comparative investigation of ‘bond bull markets’,” the BoE reports in Eight centuries of the risk-free rate: bond market reversals from the Venetians to the ‘VaR shock’, published by the bank last month. “It is shown that the global risk-free rate in July 2016 reached its lowest nominal level ever recorded.”

The record, according to BoE’s research, can be traced back to the mid-13th century. With the benefit of a longer dataset to study, the bank writes that “the current global bond market does indeed show strong signs of a historically unusual price expansion since 1981.” The chart below (click for a larger image) tracks the nominal rate since 1273.

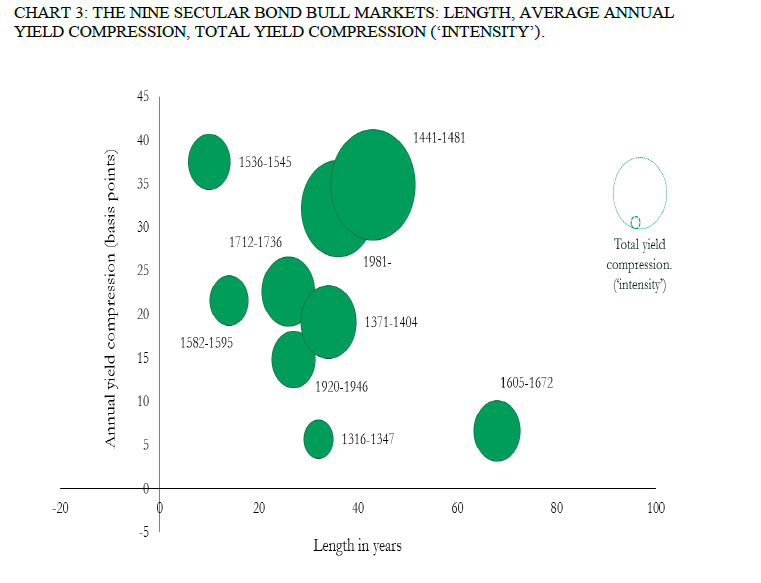

The latest (and still current?) bond bull that’s been on a 36-year run is also unusual for its length and intensity, the BoE reveals. Only two previous bull periods have been longer – one in the mid-15th century and another in the early 1600s. The yield compression of the last 36 years is also extraordinary, with only two previous periods (1441-1481 and 1536-1545) exceeding the trend in recent history.

The question, of course, is whether the current regime is on its last legs. The headwinds of history certainly appear to be blowing. There’s still room for debate, but the odds aren’t particularly favorable at this late date.

The present bond bull market originating in 1981 – despite closing 36 basis points higher at the end of December 2016 over the previous December – still has the potential to surpass the 1441-1482 bull market in intensity (though at the present trajectory this would require another eleven years at continued rate compression trends). It is, however, already the second most intense bull bond market, with a significant margin to the 1371 cycle, and could still become the second longest bond bull market, potentially overtaking – once again – its 1441 predecessor by the year 2019.