The implied inflation forecast via Treasury yield spreads continues to creep higher, but today’s November report on consumer prices is expected to reaffirm that pricing pressure remains muted. With the US suffering another coronavirus wave, the odds remain low that inflation will accelerate sharply in the near term. But a vaccine rollout is close and the economy will likely strengthen in 2021. Combine that with the incoming Biden administration, which will be incentivized to juice animal spirits, and the groundwork appears to be set for firmer prices generally.

The question is whether the secular forces that have trimmed inflation’s sails over the past several decades will fade? Unlikely. Aging demographics, growing use of technology and other factors will probably keep any reflationary rebound subdued. But in the near term, an upside bias may be brewing. Even a modest bounce in the inflation trend could appear potent in comparison with disinflationary shock in the months following the initial bite of the coronavirus crisis during the spring.

The Treasury market’s certainly pricing in a firmer run of inflation expectations lately. At yesterday’s close (Dec. 9), the implied forecast via the yield spread on the nominal less inflation-indexed 10-year maturities rose to 1.91% — the highest since early 2019.

Relative to the March low, when this 10-year spread collapsed to 0.5%, virtually overnight, the recent rise appears to suggest that a robust reflation trend is unfolding. Maybe, but for now a more compelling interpretation is that the market is revising an extreme disinflation outlook – an outlook that no longer applies, given the prospect that rollouts of effective vaccines are near and the economy has stabilized/rebounded from the coronavirus shock.

Some corners of the economy suggest that pricing pressure is bouncing back stronger than expected – housing, in particular. By one analyst’s reckoning, the housing sector’s inflation momentum is heating up.

Pricing in the housing sector is rising at the fastest rate since 2004, says Lakshman Achuthan, co-founder of the Economic Cycle Research Institute. “This economy that has been really driven by stuff at home.”

Reflationistas also note that the Treasury yield curve has been steepening in recent months, presumably in anticipation that the a stronger inflationary bias is unfolding. The 10-year/2-year spread, for instance, has rebounded to 79 basis points (Dec. 9), the highest in nearly three years.

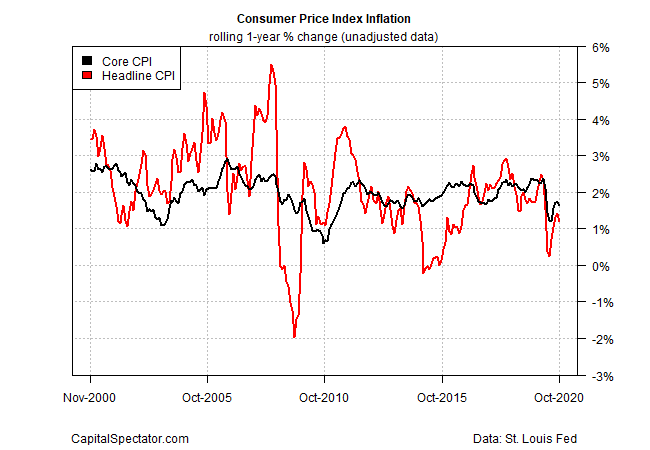

Today’s November data on consumer prices, however, is expected to show minimal if any change in the recent “lowflation” trend. The one-year change in core CPI is expected to hold steady at 1.6%, according to Econoday.com’s consensus forecast. If correct, the news will provide more evidence that inflation’s upside momentum remains hushed.

The new year could change the calculus. But with a long winter ahead of battling the coronavirus, inflation is still a low-risk threat for the near term. The Treasury market’s bounce reflects the adjusting process from the extreme disinflation pricing in previous months. Inflation will likely hold steady or edge higher in the months ahead, but it’s still hasty to assume that a hot run of reflation has started.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Pingback: Higher Inflation Expected by Treasury Market - TradingGods.net

The entire world, now awash in untethered debt and a wobbling fiat currency is expecting inflation next year.

But, like Beckett’s Godoy, what if consensus inflation never comes? Or at least, what if the long expected global inflation surge is still ten years away? What then?

Pingback: Weekend reading: Stocking up on investing wisdom

Pingback: Stocking up on investing wisdom