The US economy remains on track to post a sharp rebound in the fourth-quarter GDP report that’s scheduled for Jan. 27. The momentum, however, is expected to slow in early 2022 amid stronger macro headwinds.

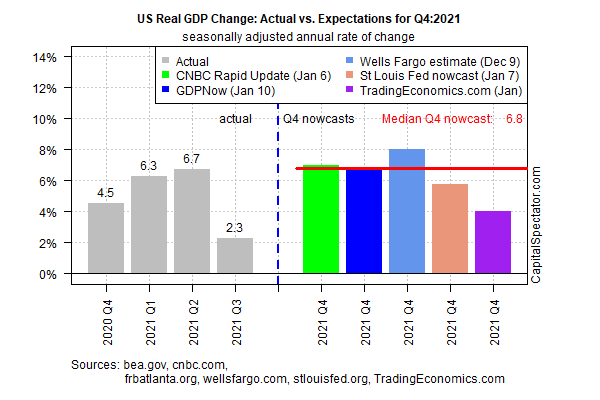

Output in last year’s final quarter is on track to rise at a seasonally adjust annual 6.8% pace, based on the median estimate for a set of nowcasts compiled by CapitalSpectator.com — down slightly from the previous estimate in late-December. The expected gain marks a sharp improvement over Q3’s 2.3% increase.

The surge in growth relative to Q3 isn’t expected to last. Several factors are likely to weigh on the macro trend in this year’s first quarter, including ongoing supply-chain constraints and fallout linked to the recent spread of the Omicron variant of the coronavirus.

“We’re getting a sense that there are a lot of infections, but it’s not going to, in all likelihood, overwhelm us. But how long is it going to be around? Because that is disruptive,” says Mark Zandi, chief economist at Moody’s Analytics.

Tighter monetary policy is also a reason to lower growth forecasts relative to Q4’s rebound. Federal Reserve Chairman Jerome Powell on Tuesday laid out a framework for raising interest rates this year. “As we move through this year … if things develop as expected, we’ll be normalizing policy, meaning we’re going to end our asset purchases in March, meaning we’ll be raising rates over the course of the year,” he told the US Senate Committee on Banking, Housing and Urban Affairs “At some point perhaps later this year we will start to allow the balance sheet to run off, and that’s just the road to normalizing policy.”

A pullback in fiscal stimulus is also a factor for managing expectations down for this year’s economic activity. “Peak fiscal policy support, and therefore peak real GDP growth, was likely realized in 2021, and the global economy now appears to be rapidly progressing toward late-cycle dynamics,” predicts PIMCO, an investment firm.

The main focus at the moment is on expectations for interest rate hikes. There’s a wide variety of outlooks on how far and how fast the Fed will life its target rate, which is currently set at a 0%-to-0.25% range. Fed funds futures are currently pricing in a 79% probability that the central bank will announce its first hike at the March 16 FOMC meeting, based on numbers published by CME Group.

Goldman Sachs sees several more increases later in the year. By some accounts, the Fed will be playing catch-up as it seeks to normalize policy in the wake of a sharp runup in inflation. In turn, the shift in monetary posture is a threat to economic growth, according to some analysts.

“Recessionary pressure is building,” says Jeffrey Gundlach, who oversees DoubleLine, a money manager. The Fed “seems pretty far behind the curve when you consider wage growth,” he advises. “We’re going to be more on recession watch than we have been.”

Perhaps, but recession risk remains low at the moment, based on analysis in this week’s issue of The US Business Cycle Risk Report. Economic momentum looks set to slow in early 2022, based on current estimates of the newsletter’s Economic Trend Index (ETI) and Economic Momentum Index (EMI) through February. But softer growth doesn’t yet translate into elevated recession risk: both indexes are expected to remain well above their tipping points (50% and 0%, respectively) that reflect neutral levels for economic activity.

The wild card is inflation and how the Fed reacts. But for the near term, the US economy remains on track to grow, albeit at a slowing pace. Now-casting.com’s current estimate for Q1 is 3.2% (as of Jan. 7), which is roughly half the expected rise for Q4.

Deciding what happens in the months ahead is still highly uncertain. The one relatively high-confidence view at the moment is that 2022 will unfold with decelerating growth momentum and several risk factors lurking.

“The world economy is simultaneously facing COVID-19, inflation, and policy uncertainty, with government spending and monetary policies in uncharted territory,” observes World Bank President David Malpass.

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno