The US economy downshifted sharply in the third quarter, based on last week’s initial estimate of gross domestic product (GDP). Is that a warning sign for Q4? No, at least not yet. The early estimates for Q4 suggest a rebound may be brewing.

Let’s start with last week’s numbers. GDP rose 2.0% in Q3 (real annualized rate), well below expectations. The comparison with Q2 is even more stark: output surged 6.7% in the April-through-June period. On its face, the sharp slowdown looks ominous, suggesting that the economy faces heightened recession risk in the near term. But a closer look suggests that output will remain positive and quite possibly rebound in Q4.

One reason for cautious optimism: Q3’s relatively weak print may be due to temporary factors linked to supply chain bottlenecks and softer consumer spending, which is probably due to a resurgence in Delta variant-related coronavirus cases in the late-summer. But both of those factors may be easing, providing a lesser headwind overall in Q4.

It’s still early in the current quarter in terms of published data and so any optimism for 2021’a end run remains uncertain and perhaps even precarious. That said, the current profile looks encouraging.

Consider, for instance, the Atlanta Fed’s latest GDP nowcast for Q4, which is running at a hot 8.5% (as of Nov. 4).

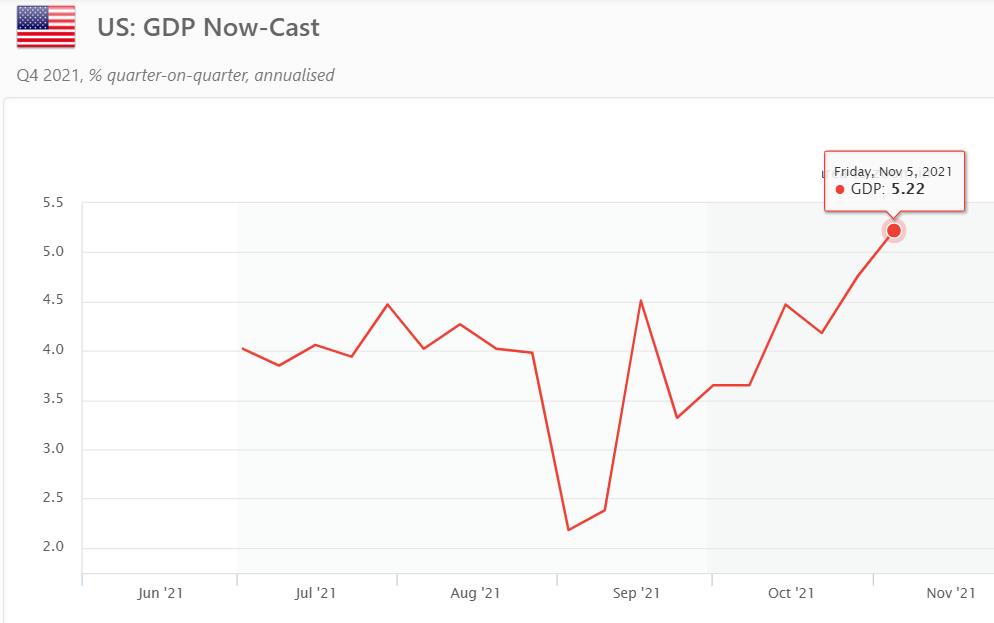

Now-casting.com’s latest estimate for Q4 also points to a recovery via a softer-but-still-strong 5.2% increase.

There’s also a case for expecting a bounce-back in consumer spending. One clue is the Chicago Fed’s weekly estimate of retail trade: data through the first half of October points to an ongoing rise in spending on Main Street.

ADP’s estimate of private sector employment for October is also upbeat. “The job market is revving back up as the Delta-wave of the pandemic winds down,” says Mark Zandi, chief economist of Moody’s Analytics. “Job gains are accelerating across all industries, and especially among large companies. As long as the pandemic remains contained, more big job gains are likely in coming months.”

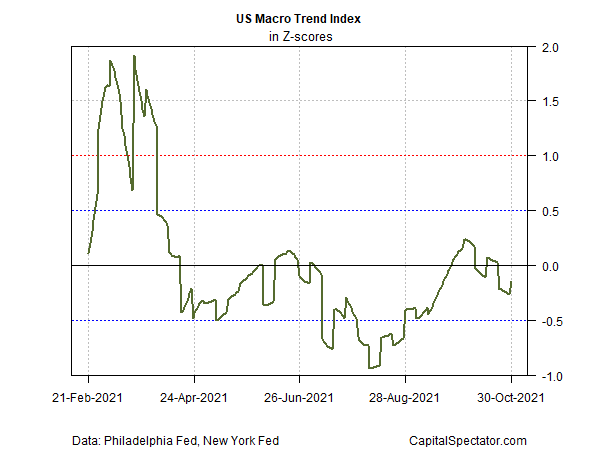

Meanwhile, CapitalSpectator.com’s Macro Trend Index, which tracks the strength of the directional bias for US economic activity in real time, continues to show that the stronger rate of deceleration of growth during the summer has eased. MTI’s current reading, based on data through Oct. 30, reflects a near-state of equilibrium in the macro trend. Given that the economy is still expanding, that’s another clue for thinking that the near-term outlook remains biased toward growth.

Several risk factors that continue to lurk could change the outlook, including a resurgent pandemic and a slower-than-expected easing of the supply bottlenecks. Higher energy prices and elevated inflation are also a threat. But for the moment, the numbers suggest that the sharp growth slowdown in Q3 isn’t a warning sign that recession risk is rising. In fact, there’s a decent case for arguing that growth is on track to strengthen in 2021’s final quarter — until or if the incoming data tell us otherwise.

Exactly how much the economy bounces in the current quarter is highly uncertain, despite what the latest nowcasts suggest. But short of a sharp deterioration of economic activity in the weeks ahead, the data suggests we’re looking at some degree of faster output in Q4 vs. the previous quarter.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report