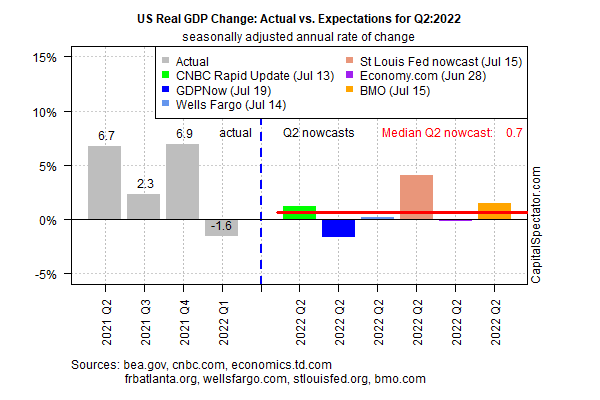

Expectations continue to slide for next week’s release of GDP data for the second quarter (scheduled for July 28). The median estimate is still positive, just barely, but has fallen recently, based a set of nowcasts compiled by CapitaSpectator.com.

The current median nowcast is just 0.7% (seasonally adjusted annual rate). The estimate reflects a sizable decline from our previous update on June 24.

One of the estimates in the table above is pointing to a steep decline in US economic activity for Q2. The widely followed GDPNow model, published by the Atlanta Fed, is projecting that next week’s Q2 will show a -1.6% drop in output.

Our median estimate is more optimistic, although one thing is clear: the US economy’s rebound in Q2, if any, will probably be weak at best.

Many analysts are warning that recession risk is elevated, although the main pushback is that the labor market’s expansion is still solid. “It would be tough to say we have a recession with 3.6% unemployment,” says Fed. Gov. Chris Waller.

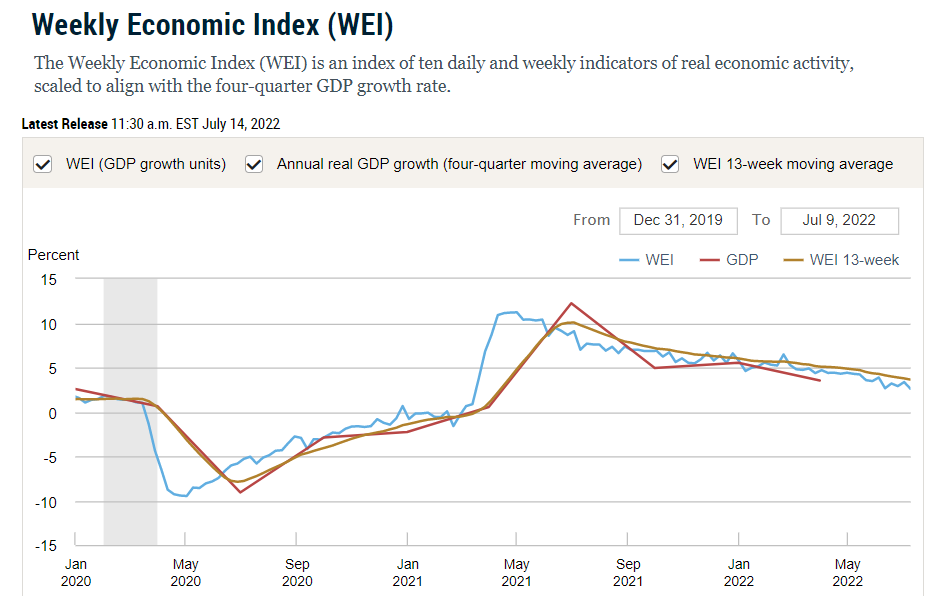

Although many key indicators are signaling slowing growth, some business-cycle indicators paint a brighter profile for current conditions relative to Q2 GDP estimates. The New York Fed’s Weekly Economic Index, for example, reflects slowing but still moderately positive growth through July 9.

Even if the US manages to sidestep a formal recession through Q2, the second half of 2022 looks set to unleash stronger headwinds. A key threat: ongoing rate hikes by the Federal Reserve as it battles persistently high inflation.

Fed funds futures are currently pricing in another hefty rate hike for the July 27 FOMC meeting, with the potential for additional hikes later in the year. Estimating recession risk, in short, is increasingly linked to uncertainty surrounding the question: How long will Fed rate hikes extend?

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report