The US recession forecasts persist for some analysts, but the start date keeps moving forward as incoming economic data continues to reflect strength. The trend is reflected in today’s upwardly revised nowcast for the upcoming third-quarter GDP report.

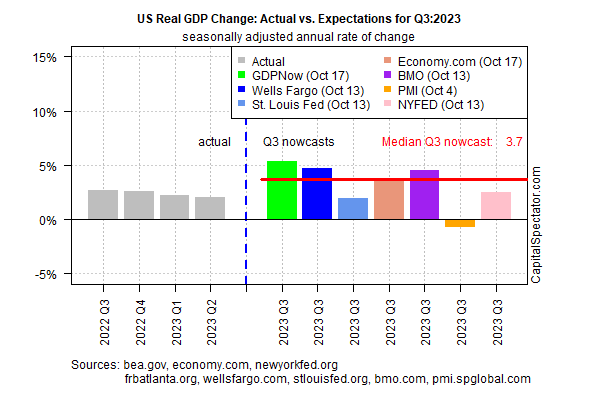

The government is expected to report on Oct. 26 that US output accelerated in Q3 to a 3.7% annualized pace in the July-through-September period, based on the median estimate via several sources compiled by CapitalSpectator.com. The estimate markets a strong improvement over the 2.1% rise for Q2.

Today’s Q3 estimate of 3.7% also reflects an upward revision from the previous update on Oct. 4, when the median nowcast was 3.2%.

The main takeaway: the recent persistence of 3%-plus median nowcasts at this late date suggest that the Q3 data due later this month will almost certainly indicate a pickup in economic activity.

The ongoing economic resilience has defied the warnings in some circles from earlier in the year that a recession was a virtual certainty by this point. As economist Paul Krugman reminds:

Until quite recently there was a near consensus among forecasters that the US economy was headed for a recession. In fact, it’s been exactly one year since Bloomberg declared that, according to its models, the probability of a recession by October 2023 — that is, now — was 100 percent.

Oops.

Most, perhaps, all recession forecasts in recent history have been a form of wishcasting in some degree. Why? A broad measure of data has consistently indicated that recession risk has remained low this year after rebounding from 2022’s short-lived dip. Yes, a different outlook was highlighted if you cherry-picked indicators. You can always see what you want to see if you focus on specific data sets. But that’s a misguided way to analyze recession. A better methodology (or perhaps it’s best to say the least-worst methodology) is to minimize noise and maximize signal by running the analytics over a wide range of indicators that, in the aggregate, present a more reliable profile.

A month ago, for example, a set of proprietary indicators used in The US Business Cycle Risk Report continued to reflect low odds that an NBER-defined recession had started or was about to start. This week’s edition of the newsletter tells a similar story, as shown in the chart below.

Some forecasters insist that a downturn is still approaching. In the grand scheme of business cycle analytics, they’re right. But it’s hardly productive to simply push recession start dates forward while ignoring the signal for a broad, diversified set of economic and financial indicators.

Yes, there’s another recession on the horizon. The key distinction: At the moment, it’s not on the near-term horizon. Some analysts say that looking beyond the next several months tells a different story. Maybe. The problem is that beyond two or three months, analyzing the path for the economy is more or less total guesswork.

To be fair, the possibility of an economic shock could radically change the analysis in a flash. The escalation of the Israel-Hamas conflict is on the short lost of threats at the moment. But evaluating this risk, much less quantifying it, is challenging, to say the least. When/if this, or some other risk, becomes a critical factor for the downside, we’ll see it in the numbers. Meanwhile, recession nowcasting using a broad set of inputs remains the only game in town.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report