How quickly and deeply will economic growth slow? That’s the critical question, but the future being the future the answer is unclear. What we do know is that headwinds are building. We also know that growth has probably rebounded from the first quarter’s contraction, based on GDP. Beyond these basic facts, the outlook turns murky.

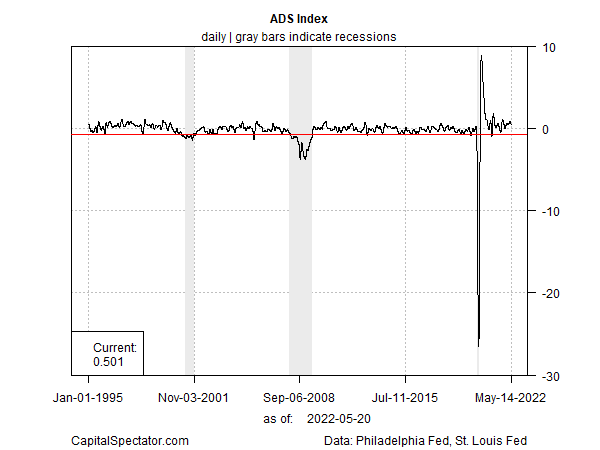

As a quick review of where we stand at the moment, a pair of business cycle indexes updated yesterday by two regional Federal Reserve banks show that growth is slowing but still well above the red zone that indicates recession. Let’s start with the Philly Fed’s ADS Index. This indicator, which tracks several key economic data sets, printed at 0.5 as of May 14. A reading above zero reflects above-average growth. One estimate of a tipping point that highlights a high probability that recession has started is -0.7 (red line in chart below), which is nowhere on the immediate horizon.

The New York Fed’s Weekly Economic Index (WEI) offers a similar profile. Yesterday’s update shows that this business cycle indicator continues to reflect growth at a level that implies the start of an economic downturn is unlikely for the near term, as of May 14. The current 4.14 for WEI is still far above my estimate of a recession signal (red line in chart below).

Encouraging, but both indicators are showing signs of slowing growth. The slowdown could be an early sign of trouble later in the year as several risk factors lurk: high inflation, a Federal Reserve committed to an extended run of tightening monetary policy, and various negative effects triggered by the Ukraine war.

Yet the 10-year/3-month Treasury yield curve (a widely followed market-based business-cycle indicator) continues to show low recession risk. Although this spread has fallen recently, it’s upward trend in positive terrain remains conspicuous and suggests that the economic outlook remains firmly biased toward growth.

Nonetheless, a number of economists have become gloomy lately and are warning that recession risk is rising. Comments in a Bloomberg story today highlight the darkening outlook from some analysts:

“I don’t think you can have a completely benign soft landing of the economy at this point,” says Ethan Harris, head of global economics research at Bank of America Corp. “We’re either going to have a weak economy or a recession.” Meanwhile, Moody’s Analytics chief economist Mark Zandi advises: “We put the odds that the economy will suffer a downturn beginning in the next 12 months at one in three with uncomfortable near-even odds of a recession in the next 24 months.”

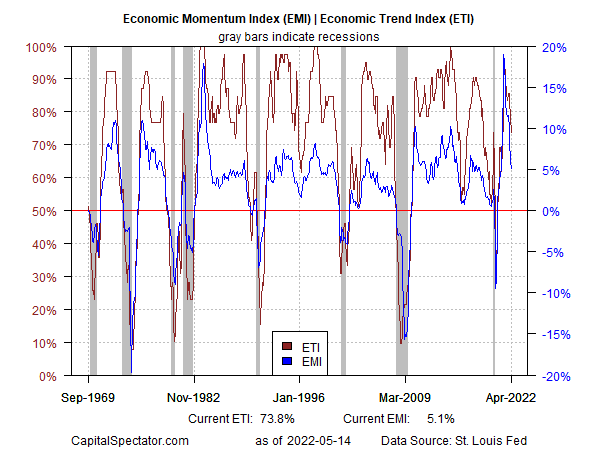

They may be correct, but it’s hard to accurately forecast economic activity beyond a few months and on that score the odds remain low that an NBER-defined recession will soon start, based on the current update of Economic Momentum Index (EMI) and Economic Trend Index (ETI) through April (for details on EMI and ETI, a pair of multi-factor benchmarks, see the sample issue of US Business Cycle RIsk Report). Deceleration in these indicators is ongoing and looks set to continue for the near term, which may signal trouble as early as late-2022. Then again, a lot can happen between now and, say, August and so forecasting that far in advance is little more than guesstimating.

In the realm of high-confidence forecasts, ETI and EMI projections through June, while lower, still indicate a moderate level of growth. ETI and EMI are expected to hold above their tipping points that signal recession: 50% and 0%, respectively.

The economy could suffer deeper trouble beyond June and that risk can’t be dismissed. It’s a potential threat that deserves close monitoring by way of incoming data. But it’s also prudent to recognize that we’re still not at a point of making a high-confidence call that a recession is fate. We may get to that point in the months ahead – or not. Meantime, growth prevails and that’s not about to change over the next month or two.

How is recession risk evolving? Monitor the outlook with a subscription to:

The US Business Cycle Risk Report