The US stock market couldn’t hold on to its snap-back rally in early trading on Tuesday, but Treasury yields posted a sharp U-turn yesterday (Aug. 25). For a day, at least, the notion that the appetite for safety was limitless was turned on its head as the crowd sold bonds.

The benchmark 10-year Treasury yield delivered its biggest one-day rise in two months on Tuesday, increasing 11 basis points to 2.12%, according to Treasury.gov. The 2-year yield, considered the most-sensitive spot on the yield curve for rate expectations, also rebounded sharply, rising 8 basis points to 0.67%.

The Treasury market’s implied inflation forecast popped yesterday, too. The yield spread for the nominal 10-year yield less its inflation-indexed counterpart jumped 4 basis points to 1.53%–the biggest daily increase in two months.

Despite yesterday’s gains, the 2- and 10-year yields remain well below their recent highs. Meanwhile, the market’s 10-year inflation forecast is still close to a four-year low. The downward bias for inflation expectations, in short, remains in force, despite yesterday’s uptick.

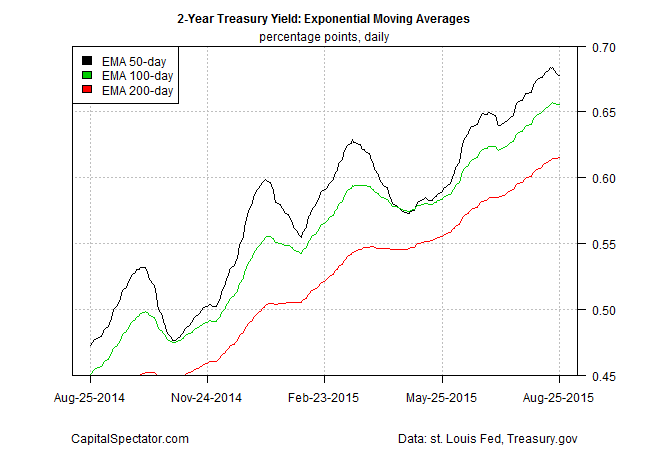

Nonetheless, the upside momentum is still relatively strong for the 2-year yield, based on exponential moving averages (EMAs).

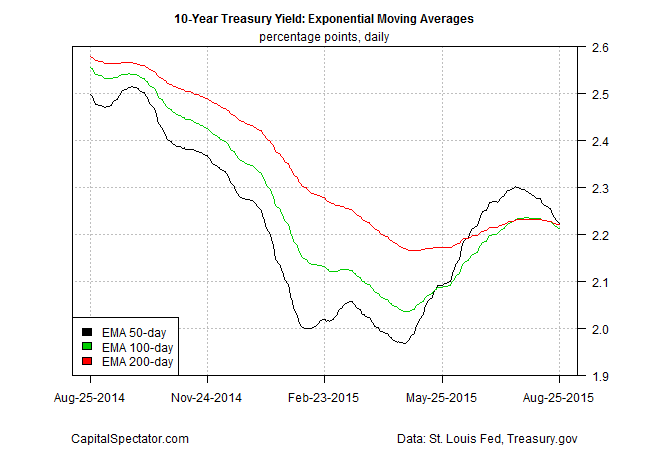

By contrast, the tide appears to be turning for the 10-year yield. EMAs on this front are signaling that the recent upside momentum may be running out of steam.

Given the turmoil in global markets lately, the case for delaying the Fed’s rate hike beyond September would seem to be obvious and compelling. “When our growth has been as volatile as it has been, when the stock market has been as volatile as it has been . . . [raising rates now] would be undertaking undue risk,” economist Joseph Stiglitz observed yesterday.

But Peter Tchir at Brean Capital offers a different spin, reasoning that the case for a rate hike is still persuasive. As reported by Business Insider, Tchir explained in a research note:

Quite frankly, I don’t care if someone wants to panic and sell stocks because the Fed hiked a measly 25 bps. I am quite convinced that this Fed will remain data dependent. If the economy deteriorates after the hike, they will cut. Or they will do QE4. I still bet that we see QE4 before 1.00% of Fed Funds, but I think the right move is to hike in September.

Not hiking sends too many wrong signals to markets. Hiking clears the path for the real take off.

How much more comfortable would I be buying a rallying S&P 500 knowing that the first hike is off the table and been absorbed? The answer is a lot more comfortable. Once we can get past the zero bound we can lose this erroneous fixation on when the first hike is and think properly about the path.

The question is whether the Treasury market agrees that a rate hike is still imminent? Yesterday’s jump in yields was quite striking in the current risk-off climate. Will we see a second day of higher yields? If so, maybe a rate hike by the Fed in September isn’t a dead issue after all.

Keep in mind that while analysts are rushing to downgrade their economic forecasts for China, the US macro trend still looks set for moderate growth in the near term, based on recent data (see here, here, and here, for instance). It could all change quickly, of course, particularly if the blowback from China is bigger than expected. But from the vantage of the latest US indicators at the moment, business cycle risk remains low. As such, pondering the next big move for Treasury yields demands navigating a tricky but familiar path between emotion and the data.

Pingback: Treasury Yields Up On Tuesday