Federal Reserve Vice Chairman Stanley Fischer last week advised that “a large part of the current [low] inflation is temporary.” Speaking to Bloomberg TV, he explained that “these things will stabilize at some point, so we’re not going to be as low as we are forever.” Based on recent action in the Treasury market, however, the crowd’s still expecting low-flation to roll on for the near term.

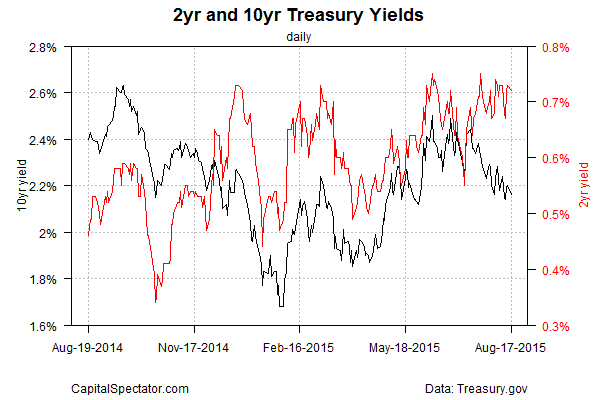

The benchmark 10-year Treasury yield ticked lower yesterday, touching 2.16%–close to a three-month low, based on daily figures from Treasury.gov. As recently as late-June the 10-year had been just a tick under 2.50%.

Is this a sign that the Fed won’t begin raising interest rates next month? That’s still an open question, in part because the 2-year yield—considered the most sensitive spot on the yield curve for rate expectations—continues to hold on to its recent gains. Indeed, the 2-year yield remains in the low 0.7% range, which is near the highest levels in almost five years. For those who think the central bank is set to begin squeezing monetary policy at the September FOMC meeting, the 2-year yield is one of the smoking guns that support such forecasts.

But skeptics wonder if the Fed is likely to begin hiking rates while inflation remains subdued. The labor market continues to rise at a brisk pace through July, but inflation remains well below the bank’s 2% target rate. The headline personal consumption expenditures price index is hovering just above zero on a year-over-year basis. Core PCE is higher, rising at roughly 1.3% a year recently. But the outlook for inflation remains low—and falling, based on the Treasury market’s forecasts.

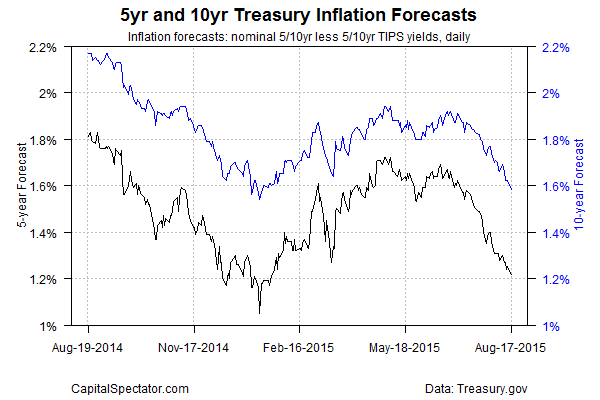

The implied inflation estimate via the yield spread on the nominal 10-year Treasury less its inflation-indexed counterpart slipped below 1.60% yesterday for the first time since January.

This is worrisome when you consider that the current outlook for economic growth in the third quarter is weak—considerably weaker than Q2’s modest 2.3% advance for GDP.

The Atlanta Fed’s Q3 forecast for GDP growth is currently a thin 0.7%, based on the Aug. 13 update. Forecasts from economists are still looking for a stronger Q3, although the impressive record of the GDPNow estimates this year raises questions about the crowd’s higher expectations.

Adding to the perception of weakness: yesterday’s surprising tumble in the New York Fed Index for this month’s reading. “It was not a good start to the August data, and a stronger dollar, weak growth overseas and a still 2 percent U.S. economy doesn’t lend itself to a robust manufacturing outlook,” wrote Peter Boockvar, chief market analyst at The Lindsey Group, in a note to clients.

Falling estimates for inflation and economic growth aren’t the raw material for inspiring rate hikes. Then again, with nonfarm payrolls still rising at a 200,000-plus rate each month lately, there’s room for debate. Meanwhile, recession risk remains low through July, as my proprietary business cycle analysis will likely reveal when I update the numbers tomorrow.

Nonetheless, the case for raising rates is hardly a slam-dunk decision at this stage, which is why the implied probability of a rate hike next month via CME’s Fed fund futures is currently just 41% this morning.

Keep in mind that it’s still early for profiling the macro trend through August. Meanwhile, the weakness in manufacturing doesn’t seem to be infecting the services sector, which continues to post a robust rate of growth. The ISM Non-Manufacturing Index for July jumped to its highest level on record (albeit for a data set that dates to 2008). Considering that services account for the lion’s share of US economic activity and employment, it’s unlikely that the macro trend is about to fall off a cliff. But that doesn’t mean that growth is poised to impress.

The bottom line: modest if not sluggish growth and subdued inflation will likely give the Fed an excuse to delay the first rate hike beyond September. There’s enough forward momentum to keep the US economy expanding for the near term. But interpreting the trend as worthy of tighter monetary policy remains a bit of a stretch until (if) we see stronger numbers on a consistent basis.

Pingback: 08/18/15 – Tuesday Afternoon Interest-ing Reads | Compound Interest-ing!