Fed Chairwoman Janet Yellen is scheduled for another chatfest in the Senate later today (starting at 10am EST), and it’s a safe bet that interest rates will be the main event. The big question on everyone’s mind, and the one the head of the central bank is sure to leave unanswered: When? Higher rates are coming, but no one knows the timing. Perhaps Janet is clueless as well. After all, there’s that incoming data issue to contend with and even the head of the world’s most influential central bank isn’t clairvoyant.

Janet may be inclined to forgo specific forecasts, but that doesn’t stop the rest of the world from guessing. Some analysts tell us that the first rate hike will arrive sometime this year, perhaps as early as June. Maybe, although the implied probability of tightening in that month is currently a low 18%, based on Fed funds futures data via the CME Group’s calculations. The odds of a rate hike rise progressively with each month, however, from 38% in July to 83% by December.

In any case, Yellen is expected to talk tough, at least by recent standards of macro commentary from Fed heads. Her commentary will be “reasonably upbeat,” predicts Sean Callow, a currency strategist at Westpac Banking Corp. in Sydney. “That should leave intact a pretty high probability of at least a summer rate hike and maybe as soon as June.”

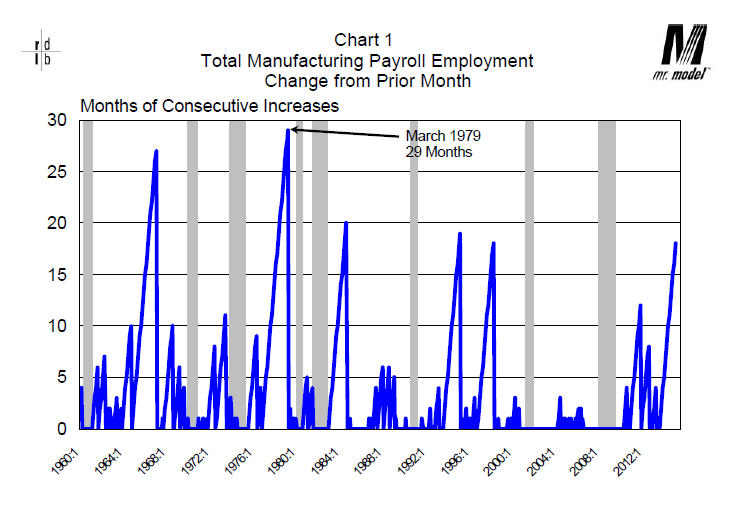

The centerpiece of the rationale for rate hikes is the stronger labor market. The net gain of 1.009 million nonfarm payrolls for the November-through-January period is the strongest three-month run since 1997. Reviewing the cyclically sensitive manufacturing sector draws an even stronger profile, based on some intriguing number crunching by economist Bob Dieli at NoSpinForecast.com. Measuring the consecutive number of monthly net gains in manufacturing suggests that the animal spirits in hiring has picked up sharply in recent months in this corner of the economy.

“This is the first time since 1998 that we have had a run of at least 15 consecutive months of gains in total manufacturing employment,” Dieli says, adding that “this is only the sixth time since 1960 that we have had such a strong run.”

The key question, of course, is whether the acceleration in payrolls is sustainable or just another post-recession head fake that fizzles? No one really knows the answer… yet. Nonetheless, Yellen’s testimony today will be closely analyzed for clues on how the Fed’s monitoring the data in the delicate art of trying to decide when to begin tightening monetary policy, if only on the margins.

The crowd will be listening, but it’s not obvious that today’s discussion will dispense much in the way of news beyond what we already know. “I anticipate that she will stick to an economic outlook very similar to that detailed in the last FOMC statement and related minutes,” writes veteran Fed analyst Tim Duy. “Expect her to indicate that the Fed is closing in on the time of the first rate hike – after all, this was clearly the topic of conversation at the January FOMC meeting.”

One potential wrench in the monetary machine is inflation, or the lack thereof. The Fed’s preferred measure—personal consumption expenditures price index—is still running well below the central bank’s 2% target. Headline PCE inflation was a slim 0.75% on a year-over-year basis in December; core PCE was higher—1.33% vs. the year-earlier level, but in both cases the latest update was below the trend for the previous month. Even weaker numbers may be coming in the January update, or so it appears based on estimates via PriceStats.

How does the soft inflation data factor into the outlook for a rate hike? Or does it? Perhaps Janet will enlighten us in today’s Senate testimony.

Pingback: The Federal Reserve and Interest Rates