Federal Reserve Chairwoman Janet Yellen told the crowd last week that rate hikes are coming. The rise will be gradual, she said, but there’s an upward bias for the road ahead. “With continued improvement in economic conditions, an increase in the target range for [the federal funds rate] may well be warranted later this year,” Yellen advised. But getting from here to there faces a rough road, including what’s shaping up to be a disappointing start for growth in this year’s first quarter. Meantime, the Treasury market is nonplussed by Janet’s latest comments. Yields on government bonds remain well below recent highs, effectively telling the Fed that the future looks somewhat different relative to the narrative that the Fed chair is pushing.

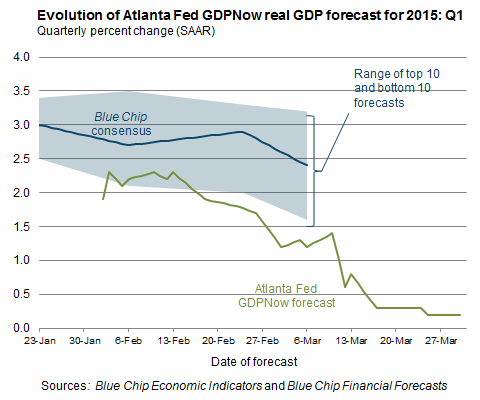

Consider yesterday’s update of the Atlanta Fed’s estimate for first-quarter GDP. The bank’s currently projecting that growth came to a virtual standstill in the first three months of 2015, rising just 0.2% — well below the 2.2% pace in last year’s fourth-quarter and a world below Q3’s 5.0% surge.

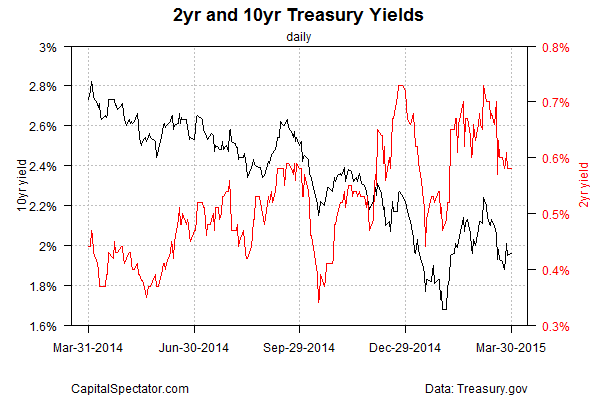

The optimistic view is that this year’s sluggish trend is a temporary setback due to a harsh winter. Some of the recent economic reports offer support for that view, although you could just as easily point to the disappointing updates in recent weeks to argue the opposite. Not surprisingly, the crowd doesn’t appear to be impressed one way or the other. The benchmark 10-year yield, currently at just below 2.0%, hasn’t moved much in recent days and is is well below the recent high of 2.24% that was touched in early March. A similar story applies to the 2-year yield, which is widely considered to be the most-sensitive maturity for rate expectations.

Economist Tim Duy, a veteran Fed watcher, reasons that “Yellen intends to look through any first quarter weakness in GDP data, seeing it as largely an aberration (like arguably the first quarter of last year), as long as the employment data continues to hold up.” He adds that “I doubt any one weak report would do much to undermine her confidence in the recovery; we should be focusing on the story told by the next three employment reports in aggregate.”

Maybe so, but those reports will still arrive one at a time, starting with this Friday’s update on payrolls for March. What should we expect? Yellen seemed to offer some guidance last week, explaining:

I am cautiously optimistic that, in the context of moderate growth in aggregate output and spending, labor market conditions are likely to improve further in coming months. In particular, and despite the somewhat disappointing tone of the recent retail sales data, I think consumer spending is likely to expand at a good clip this year given such robust fundamentals as strong employment gains, boosts to real incomes from lower energy prices, continued increases in household wealth, and a relatively high level of consumer confidence.

Economists anticipate that this Friday’s data on March payrolls will continue to post a solid rise, although a whiff of deceleration is expected to hover over the numbers. Econoday.com’s consensus forecast calls for an increase of 247,000 in total payrolls for this month. That’s a decent advance, although it’s also a conspicuous downgrade from February’s 295,000 increase.

Nonetheless, if the consensus view is right, the gain is strong enough to keep Yellen from changing her outlook, although a downside surprise of any magnitude would inspire a new round of revised forecasts for what lies ahead. But if analysts are right and we see another rise that’s well above the 200,000 mark, the case for a Yellen-based view of the near-term future will remain intact. A bit bruised, perhaps, but intact. In that case, the only question is whether Mr. Market’s willing to play along with the Fed chair’s forecast?

Pingback: Tuesday Morning Links | timiacono.com