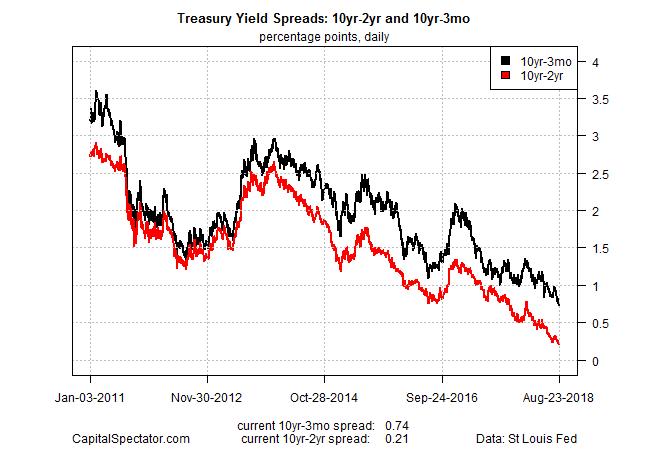

The difference in the widely followed spread in 10- and 2-year Treasuries slipped to 21 basis points on Thursday (August 23), marking yet another 11-year low, based on daily data via Treasury.gov. The narrowing gap is stoking debate about whether a new recession is near and the wisdom of what’s expected to be another rate hike by the Federal Reserve next month. Based on current data, however, the economic data continues to reflect a healthy macro trend for the US. The question is whether various risks on the horizon, including a US trade war with China, will delay or even derail the central bank’s plans for higher rates?

A formal recession warning requires an inverted curve – short rates above long rates. By that measure there’s still a margin of safety, albeit a small and fading one. Another rate hike may tip the 10-year/2-year curve into negative terrain for the first time since 2007, a year or so ahead of the start of the last recession.

Fed funds futures are pricing in a 98% probability that the central bank will lift its target rate by 25 basis points to a 2.0%-to-2.25% range, according to CME. With the 10-year/2-year spread at just 21 basis points, a quarter-point rise leaves room for wondering if the curve will invert in the near-term future.

When You Need Reliable & Timely Intelligence On Recession Risk:

The US Business Cycle Risk Report

Meantime, the effective Fed funds rate (the rate on overnight loans between banks) has recently ticked up to 1.92% and has been trading above its 30-day average for the week through August 22. That’s another sign that the central bank’s upward bias on rates prevails at the moment.

At least one policymaker is looking to keep short rates moving even higher, which suggests an inverted curve is coming. Dallas Fed President Rob Kaplan this week recommended several more rate hikes so that monetary policy is at a so-called neutral level for the economy.

“My own view is we should be raising rates until we get to neutral,” he told CNBC. “We should do it gradually. I’m not prepared to say yet I want to go above neutral.”

Doubts are increasing about whether a hawkish policy path, even a modest and gradual one, remains viable.

“The policy challenges are getting more difficult in the next 12 months,” says James McCann, senior global economist at Aberdeen Standard Investments. “The trade situation has escalated in recent months, we’re carefully watching how the Fed incorporates that into their thinking. If tariff measures push up inflation, and slow growth that’s not a straightforward policy conundrum.”

Indeed, headline consumer inflation ticked up to a 2.95% year-over-year pace in July, the highest since 2011, based on unadjusted numbers for the consumer price index (CPI). Core CPI (less food and energy) is also trending up, reaching 2.35% last month vs. the year-ago level – the biggest advance since 2008.

But in a sign that the crowd’s outlook is mixed, the Treasury market’s implied estimate of inflation has been edging lower in recent months after touching a recent peak in the spring. The spread between the 5-year nominal Treasury less its inflation-indexed counterpart, for instance, was 1.99% yesterday, below this year’s peak of 2.16% reached in May.

If the market forecasts fall further, the case for more rate hikes may be weaker than assumed.

The critical factor, of course, is the broad economic trend and on that score one can argue that another round of policy tightening is reasonable. Uncertainly is inching higher, however, on the question of how the incoming data fares. Yesterday’s survey data via IHS Markit reflected a slight deceleration in US growth, although the expansion is still solid.

“The US economy lost a little pace in August, according to the flash PMI, but continued to grow at a solid rate,” notes Chris Williamson, chief business economist at IHS Markit. “The PMI is indicative of the economy growing at an annualized rate of roughly 2.5%, down from a 3.0% indicated rate in July.

Meantime, today’s revised third-quarter GDP growth estimate for the US ticked down to 3.2% via Now-casting.com. That’s a healthy gain, but it’s clear that the robust 4.1% increase for Q2 appears on track to soften.

Will growth projections continue to decelerate to a degree that convinces the Fed to hold off on another rate hike at its September 26 policy announcement? For now, that looks unlikely. But confidence is a bit weaker about what happens next in the wake of disappointing numbers in key areas such as housing – new residential construction was mildly negative in year-over-year terms for a second month in July.

Accordingly, the next several weeks of economic releases will be closely read for fresh clues.

As for the yield curve, Atlanta Fed President Raphael Bostic is downplaying the narrowing spread. “I believe the yield curve gives us important and useful information about market participants’ forecasts,” he wrote yesterday. “But it is only one signal among many that we use for the complex task of forecasting growth in the U.S. economy.”

In any case, like everyone else, he’ll be keeping a close eye on the incoming numbers. For now, however, Bostic asks and answers the critical question:

When we ask whether a flattening yield curve is a cause for concern, what we are really asking is: does the market expect an economic slowdown that will require the FOMC to reverse course and lower rates in the near future?… The market appears to be forecasting continuing policy rate increases through 2020, and there is no evidence of a market forecast that the FOMC will need to reverse course in the medium term.

Let’s see if the next round of data updates concurs.

Pingback: Weighing the Week Ahead: Should Investors Worry about the Yield Curve? | Dash of Insight

Pingback: Worried About the Yield Curve? - TradingGods.net

Pingback: Landmark Links August 28th – The Heist