It’s been a year of revival so far for the previously trailing small-cap value space in the US stock market. Deciding if the party can last may depend on how stocks overall fare in the months ahead and whether the consensus forecast for a strong economic recovery is accurate.

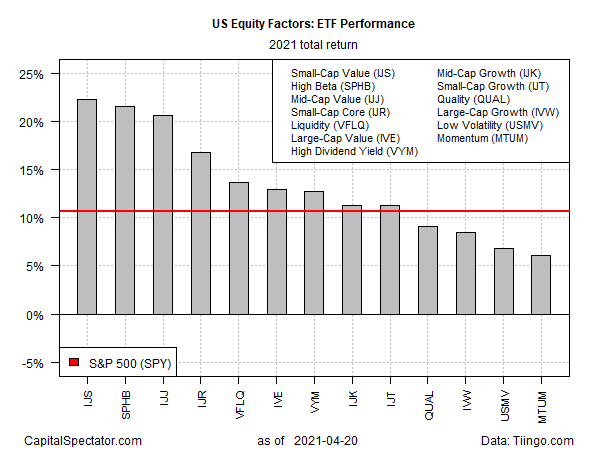

For now, small-cap value is the top-performing equity risk factor year to date, based on a set of exchange traded funds. The iShares S&P Small-Cap 600 Value ETF (IJS) is enjoying a strong 22.3% total return in 2021 through yesterday’s close (Apr. 20). The edge over second- and third-place factors is shrinking, but for now IJS holds the high ground. Meanwhile, measured against the broad market, there’s no comparison: IJS’s year-to-date run is more than double the 10.6% increase for SPDR S&P 500 (SPY) so far in 2021.

Small-cap value (SCV) is widely followed, in part because of influential research in the 1990s that first documented that this slice of equities’ capacity for outperforming the broad stock market through time. But as the SCV stumbled in recent years, investors wondered if the risk premium had faded and the original research was wrong. But as the risk factor’s prospects hit rock bottom, the tide began to turn, or so it seemed.

Last June, The Wall Street Journal wrote that “Small ‘Value’ Stocks Are Down but Not Out.” The article was a timely piece, arriving just ahead of renaissance in SCV leadership. Since November, IJS has pulled far ahead of the broad market (SPY).

In fact, there’s been a strong run for most of the major US equity factors so far this year. More than half of the ETF-based equity factors in the table above are beating the broad market’s performance in 2021. Note, too, that every corner of this factor zoo is posting a gain, ranging from a relatively modest 6.0% rise for momentum (MTUM) up through small-cap value’s performance lead.

Yet the second-place high-beta version of the S&P 500 is nipping at small-cap value’s heels. Invesco S&P 500 High Beta (SPHB) is up 21.6% so far this year, just slightly behind IJS’s lead.

The main challenge for stocks generally at the moment is the risk of a correction for a market that, generally, appears to have run too hot too fast. By some accounts, bubble risk is also brewing.

“The asset bubble keeps on getting bigger and bigger,” advises David Rosenberg, chief economist and strategist at Rosenberg Research, in a research note to clients. “Please understand that this is the second most expensive S&P 500 index of all time.”

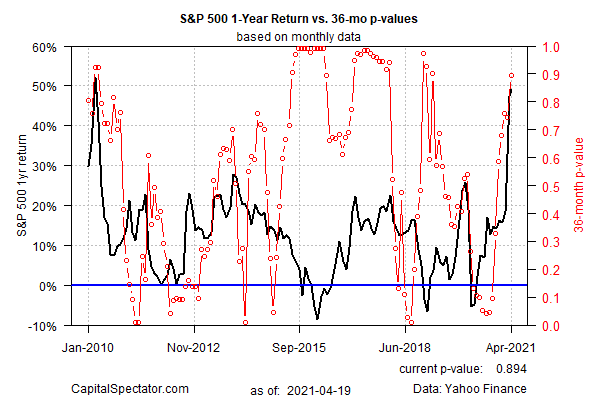

A basic econometric measure of bubble risk maintained by CapitalSpectator.com supports the idea that the S&P 500 is looking a bit frothy these days, as shown in the chart below. (For some background on the metric’s design, see here.)

Given the broad market’s strong run over the past year, with limited downside, it wouldn’t be surprising to see a correction at some point in the near term. A pullback of some magnitude would likely weigh on all the equity factors. In that case, deciding if small-cap value’s mojo was noise or the start of extended recovery after a long period of weakness would emerge on the other side of a correction (or bear market, if it comes that).

In any case, some analysts remain optimistic. AllianceBernstein, writing this week, advises that “we believe several forces will continue to drive the recovery in the months, and possibly years, ahead.” Even higher interest rates don’t threaten SCV, the money management shop explains. Meanwhile, “at current valuations, we believe small-cap value stocks are still undervalued, and the potential narrowing of the discount can drive a lot of outperformance.”

Learn To Use R For Portfolio Analysis

Quantitative Investment Portfolio Analytics In R:

An Introduction To R For Modeling Portfolio Risk and Return

By James Picerno

Pingback: A Year of Revival for the Small-Cap Value Space - TradingGods.net