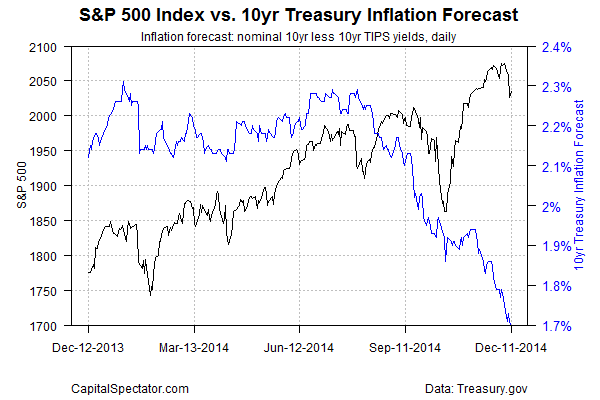

The Treasury market’s implied inflation forecast continues to fade, dipping to 1.70% yesterday (Dec. 11) — close to a four-year low, based on the yield spread for the nominal 10-year Note less its inflation-indexed counterpart. The slide looks worrisome, but appearances can be deceptive at a time when US economic growth is holding steady if not accelerating. Indeed, while economic activity decelerates/stagnates elsewhere, the US trend is gaining momentum, or so yesterday’s retail sales data (and last week’s bullish payrolls update) suggest. Meantime, the bear market in energy may end up boosting US growth on the margins in the months ahead while putting pressure on inflation.

“Oil prices are continuing to decline and inflation expectations tend to be correlated quite highly with that,” says Allan von Mehren, chief analyst at Danske Bank A/S. “At the same time there is a correction in risk sentiment and there is greater expectation of QE from the [European Central Bank]. These are all pushing down yields.”

Europe’s woes may create headwinds for the US eventually, but at the moment America’s macro resilience endures. Reuters reports that the latest round of upbeat data inspired Macroeconomic Advisers to raise its estimate of fourth-quarter GDP growth for the US by three-tenths of a percentage point to 2.4% (seasonally adjusted annual rate). A key catalyst: “unexpected strength” in consumer spending.

Falling inflation expectations and an improving economic outlook make for strange bedfellows, but the rosy glow appears genuine. Looking to 2015, the economics group at Wells Fargo, for instance, likes what it sees:

In the year ahead, we expect real consumer spending growth to maintain its current course, averaging 2.5 percent for the year. Employment gains and modest real disposable income growth will help to provide support to overall consumer spending. In addition, lower gasoline prices should also bolster more discretionary consumer spending activity.

The current state of macro adds up to a positive bias for the US, but it’s also leaving the Treasury market with a touch of bi-polar disorder these days. On the one hand, downward momentum is conspicuous for the 10-year yield while the 2-year yield – the most sensitive part of the curve when it comes to rate expectations – is trending up.

Economists are still anticipating that the Fed will start raising interest rates in the middle of 2015, according to a new survey of economists via The Wall Street Journal. By some accounts, the central bank would be justified in raising rates today, based on Blackrock’s “Yellen Index,” CNBC reports:

The proprietary index is made up of a series of labor and growth metrics that the Fed would be watching as it contemplates interest rates, and the index is showing improvement all fronts.

“It’s pretty clear today that we hit virtually every metric,” said Rick Rieder, BlackRock CIO of Fundamental Fixed Income. “We’re at a place today where the Fed would move. Quite literally, we believe they could move today based on what the data shows.”

Higher rates and falling inflation expectations? Welcome to the new new normal.

Pingback: Friday links: margin debt don’ts | Abnormal Returns

Pingback: Monday Morning Links | timiacono.com