The Fed punted on raising rates yesterday, but that didn’t stop it from raising its estimate of GDP growth for 2015… slightly. The median projection for this year has been tweaked up to +2.1% from +1.9% in the June outlook. The modest increase in projected growth looks a bit odd in the context of leaving the target rate for Fed funds unchanged at zero-to-0.25%. But all becomes clear when we review the Fed’s assumptions for 2016.

The central bank sees slower growth next year in comparison with its June forecast: +2.3% vs. +2.5% in the previous estimate. Inflation is expected to be higher next year and move closer to the Fed’s 2% target, although the new estimates for headline and core PCE price changes in 2016 were trimmed relative to June’s outlook. The one set of uniformly upbeat revisions: the unemployment rate, which is on track to dip to 4.8% next year from 2015’s expected 5.0% rate, based on the median projection. In short, moderate growth is still the likely scenario, but at a slightly lesser pace relative to recent history. That’s not terrible, but it’s not particularly encouraging either.

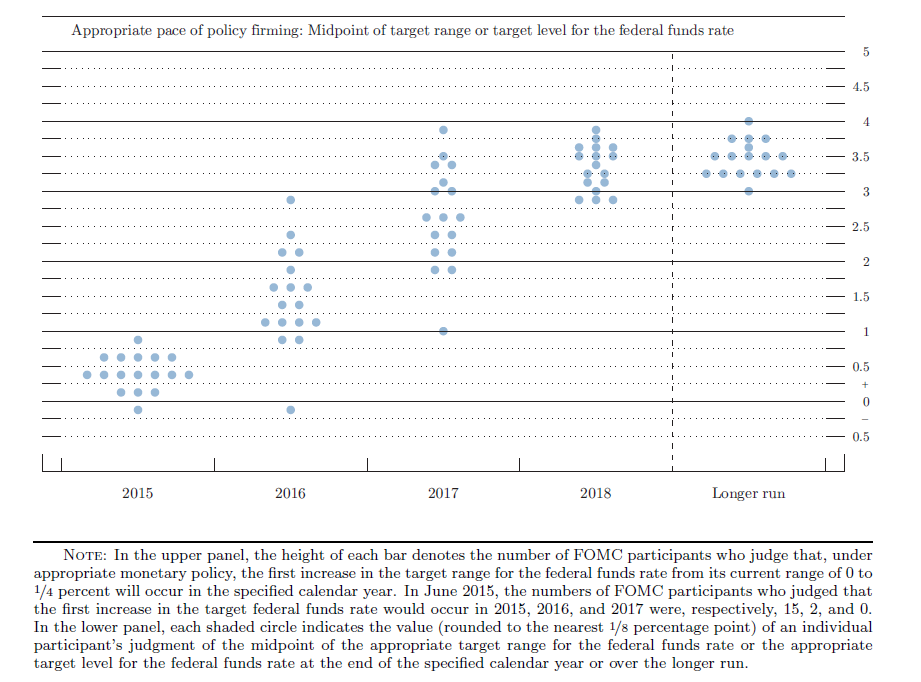

Perhaps the most surprising data point in yesterday’s Fed fest: the appearance of negative interest rate recommendations from one of the FOMC members. Although unnamed, someone at the monetary helm thinks an “appropriate” level for the Fed funds target rate is below zero. Is that a prelude to QE4? The alternative theory is that it’s not a serious hint of things to come. Instead, it was a message from the departing Minneapolis Federal Reserve Bank President Narayana Kocherlakota. According to Neil Dutta at Renaissance Macro, “Kocherlakota had a nice parting shot …[he] wanted an ease to negative rates in 2015.”

The main takeaway from yesterday is that the Fed’s still looking for a moderate pace of growth, but with the caveat that lowflation will remain a threat. The prospect still looks dim for reaching the Fed’s 2% inflation target in the foreseeable future. That’s a risk factor, and one that will become a much bigger problem if growth stumbles.

The Fed’s GDP outlook offers a mild degree of optimism for thinking that the worst-case scenario–a recession that starts with inflation close to zero–is still a low-probability threat. But the Atlanta Fed’s current forecast for growth in the current quarter leaves room for doubt. GDP is projected to rise a tepid 1.5% in Q3, based on the Sep. 17 update of the GDPNow model—less than half the rate posted in Q2.

Using the Atlanta Fed’s forecast as a guide makes one thing clear: delaying the rate hike was the right thing to do. Leaving monetary policy unchanged isn’t likely to offer much additional help for the economy at this late date, but pushing rates higher in the current climate doesn’t look right either.

“If you are incorporating global economic and financial market developments into your calculus then it will be very difficult for this Fed to get off of zero,” says Tom Porcelli, chief U.S. economist for RBC Capital Markets.