A December interest-rate hike is a “live possibility,” Federal Reserve Chair Janet Yellen said in yesterday’s testimony in Congress. The Treasury market took the hint and the 2-year Note—said to be the most sensitive maturity for rate expectations—jumped to 0.84% yesterday (Nov. 3), edging up to the highest level in nearly six years, based on daily data from Treasury.gov. Since last month’s low on Oct. 14, the 2-year yield has climbed sharply, rising 27 basis points.

Interest rates have been on a rollercoaster in recent months as incoming economic reports have delivered mixed messages. But Yellen’s message is that the economy’s still recovering, albeit unevenly lately. Nonetheless, she emphasized that the forward momentum is sufficiently strong to raise the possibility that the central bank will begin tightening monetary policy, if only slightly, at next month’s FOMC meeting. Yes, we’ve heard this before, only to learn later that the expecting a hike was premature, thanks to the news du jour. Is this time different? Maybe, although much depends on how the numbers stack up in the weeks ahead. Meantime, the crowd’s on board with assuming that the first rate hike is near.

Indeed, the 2-year yield has surged in recent days. The benchmark 10-year yield’s climb is less striking but the rebound is still conspicuous on this front too.

There’s also a modest edge in Fed fund futures for pricing in a rate hike for the Dec. 16 FOMC meeting. Based on data for yesterday, 30-day futures estimate a 56% probability that Fed funds will rise to 0.5% from the currently zero-to-0.25% target, according to CME’s numbers.

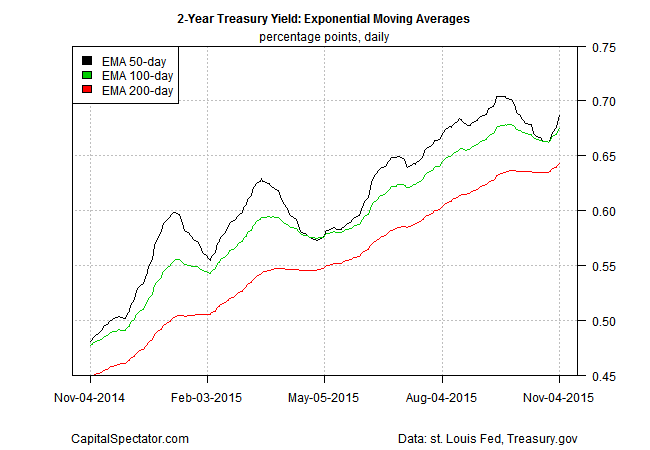

The recent change in expectations pulled the 2-year yield back into a bullish formation via a set of exponential moving averages (EMAs). After slumping in previous weeks, the 50-day EMA for the 2-year yield has rebounded and is again signaling higher rates for the near term.

EMAs for the 10-year yield, however, still look weak. Although there’s been a mild reversal in recent days, the technical profile on this front leaves room for doubt about the prospects for a rate hike next month.

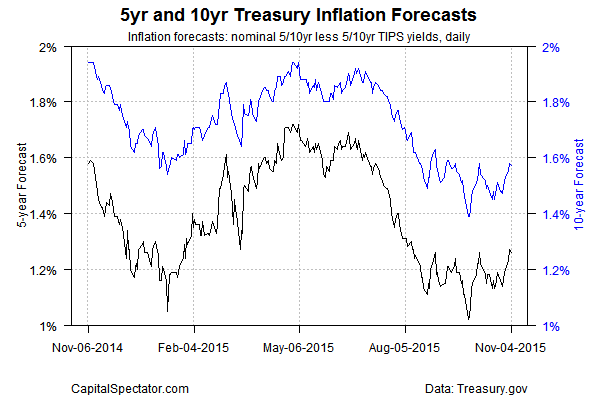

Meanwhile, the Treasury market’s inflation expectations—nominal less inflation-indexed yields–have bounced up lately, but the rebound is mild so far. Will the Fed start raising rates while the inflation outlook remains subdued? On the other hand, if we see inflation expectations rise further in the days and weeks ahead the case for squeezing policy will strengthen.

On balance, there’s a modestly stronger case for expecting a rate hike next month, although there’s still enough doubt to keep reasonable minds on the fence. What could tip the balance one way or the other? Tomorrow’s employment report from the Labor Department is an obvious possibility. But for the moment, the outlook is less than decisive.

Briefing.com’s consensus forecast sees total nonfarm payrolls bouncing back in October after September’s tepid rise. But the crowd’s prediction for a 181,000 gain is moderate at best. Yes, that’s strong enough to argue that the US macro trend remains on a growth track, but it’s hardly a smoking gun that will seal the deal for a rate hike. Then again, perhaps there’s enough juice there to provide cover for raising Fed funds even the full boat of economic numbers don’t look overly convincing. Of course, if there’s a substantial upside surprise in tomorrow’s jobs report, the crowd’s going to make the obvious connection and send yields sharply higher.

“There are pretty good odds that the Fed will hike rates in December as long as employment perks back up and the unemployment rate slips further, which is what we are looking for,” Mark Vitner, a senior economist at Wells Fargo Securities, tells Bloomberg.