The Federal Reserve raised interest rates again yesterday, but the announcement of tighter policy followed news that the trend in core consumer inflation drifted lower. The combination of higher rates and a softer pricing pressure raise questions about the Fed’s plans for 2018.

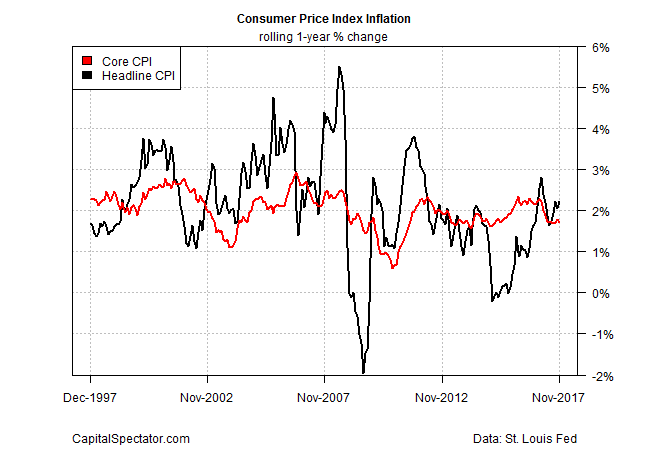

Core consumer price inflation (excluding energy and food) ticked down to a 1.7% year-over-year increase in November, in line with recent data that marks the softest trend in more than two years. The sluggish pace suggests that the Fed will have a hard time reaching its 2% inflation target in the near term.

“The lack of a sustained pickup in core CPI does make the Fed deliberations about the pace of monetary policy tightening next year more complicated,” says Kathy Bostjancic, head of U.S. macro investor services at Oxford Economics.

Nonetheless, the case for firmer inflation next year isn’t dead, explains Leslie Preston, a senior economist at TD Bank Group.

We remain confident that conditions are ripe for inflation to build in the months ahead, although the process is proving lengthy. No doubt November’s inflation data is a setback. But, the sizeable decline in apparel prices is unlikely to be repeated next month, suggesting core inflation will firm once again in December. In an economy with unemployment at a 17-year low, and back-to-back quarters of 3% growth in real terms, conditions are ripe for increased pricing power. Adding to those healthy economic conditions, Congressional Republicans look set to pass a tax cut in the coming days. This will add further to inflationary pressures in 2018.

Perhaps, although it’s interesting to note that while the Fed lifted rates yesterday, the real (inflation-adjusted) trend in M0 money supply continued to rise in November. For the fourth month in a row, this narrow gauge of monetary liquidity increased, which suggests that the Fed’s policy stance may not be as hawkish as yesterday’s rate hike implies.

Note that M0’s real year-over-year trend had been negative for most the two years through this past July, indicating a hawkish bias. But the tide turned in August and the annual pace has been positive for four consecutive months – the longest stretch of gains since the first half of 2015.

Why should we care? For starters, the real M0 trend tends to offer valuable perspective on business-cycle risk. The annual change for this monetary metric tends to go negative ahead of US recessions.

Recent history post-2008 has been an exception, probably because monetary policy has been so extraordinary. In particular, mopping up the excess liquidity in the wake of the Great Recession required several doses of negative year-on-year changes. In any case, it appears that the Fed realized that the negative trend in real M0 had gone too far by mid-2017.

The question is what the return of M0 growth means for monetary policy in 2018? Is this a sign that the Fed is on track to delay its rate-hike plans? At the moment, the central bank seems to be hedging its bets by raising the Fed funds target rate while resuming M0 growth.

An added complication for considering next year’s policy outlook: Jerome Powell, a former investment banker, takes charge of the Fed in February. Exactly what that means for policy changes, if any, is open for debate.

Meantime, the margin for error with policy mistakes may be narrowing. If the Fed continues to raise rates and inflation remains subdued, there could be repercussions.

“If the Fed gets its paradigm wrong and sees inflation that ultimately doesn’t materialize, and they take rates too far, then markets would feel aggrieved,” says Carl Tannenbaum, chief economist at Northern Trust in Chicago and a former senior risk official at the Fed.

Pingback: Core Consumer Inflation Drifts Lower - TradingGods.net

Pingback: Treasury Market Inflation Estimate At 8-Month High